Alnylam Pharmaceuticals (NASDAQ:ALNY) presented its second quarter 2025 financial results on July 31, showcasing substantial growth driven primarily by its successful ATTR-CM launch in the United States. The company’s stock responded positively, trading up 4.47% to $355 in premarket activity following the presentation.

The biotechnology company, which specializes in RNA interference (RNAi) therapeutics, reported a significant acceleration in revenue growth compared to previous quarters, achieving non-GAAP profitability and prompting management to raise full-year guidance.

Quarterly Performance Highlights

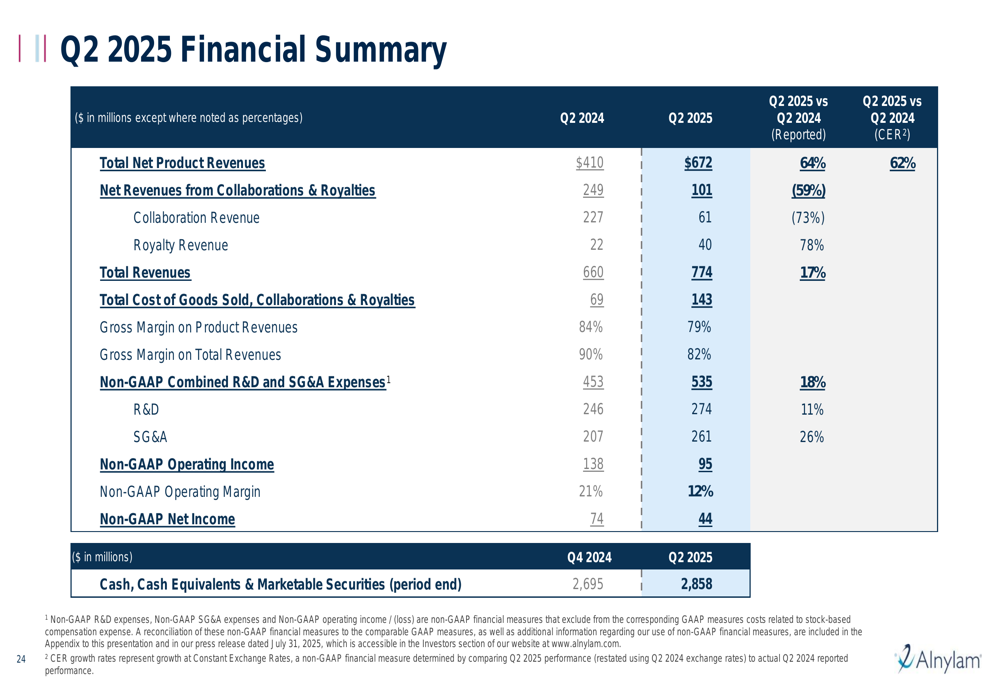

Alnylam reported total revenues of $774 million for Q2 2025, including $672 million in net product revenues, representing 64% year-over-year growth. This substantial increase was primarily driven by the company’s TTR franchise, which generated $544 million in revenue, up 77% compared to Q2 2024.

As shown in the following comprehensive financial summary:

The company achieved non-GAAP net income of $44 million, marking an important milestone in Alnylam’s financial trajectory. Net revenues from collaborations and royalties contributed an additional $101 million to the quarter’s results.

The rare disease franchise, comprising GIVLAARI and OXLUMO, delivered $128 million in Q2 2025 net product revenues, representing 24% year-over-year growth. GIVLAARI specifically showed strong performance with 30% year-over-year growth, while OXLUMO grew by 15%.

ATTR-CM Launch Success

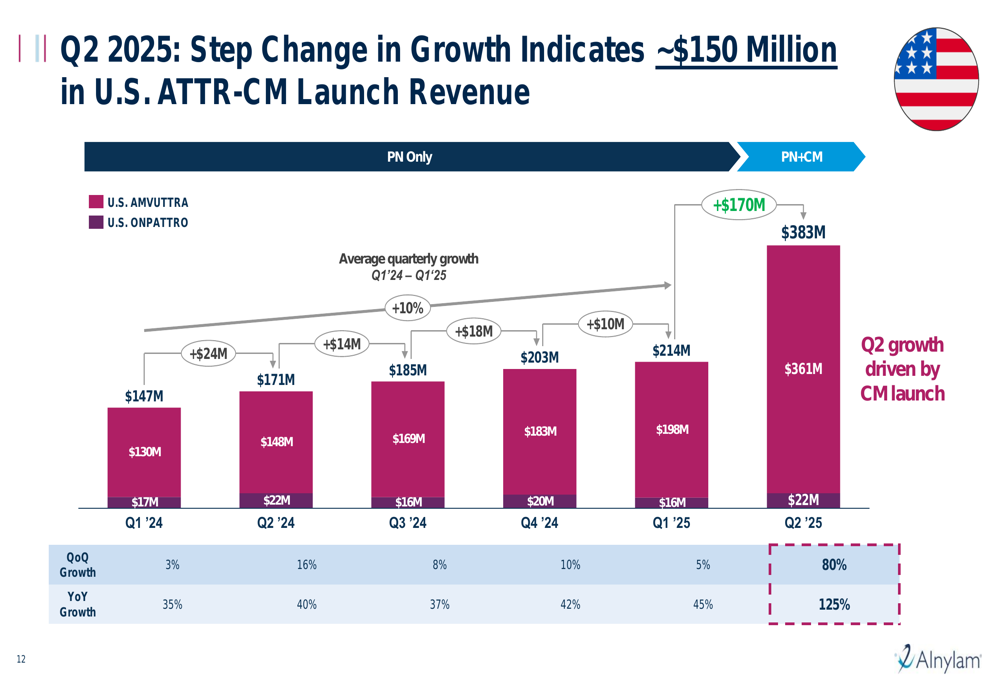

The most significant driver of Alnylam’s growth in Q2 was the successful U.S. launch of AMVUTTRA for ATTR cardiomyopathy (ATTR-CM). The company reported approximately 1,400 CM patients receiving AMVUTTRA by the end of Q2, generating approximately $150 million in ATTR-CM revenue for the quarter.

This launch has created a clear inflection point in the company’s growth trajectory, as illustrated in the following chart showing the step change in U.S. TTR franchise revenue:

The U.S. TTR franchise demonstrated exceptional growth, with 125% year-over-year and 80% quarter-over-quarter increases. This performance reflects substantial demand growth driven primarily by the ATTR-CM launch, with U.S. demand growing 115% year-over-year.

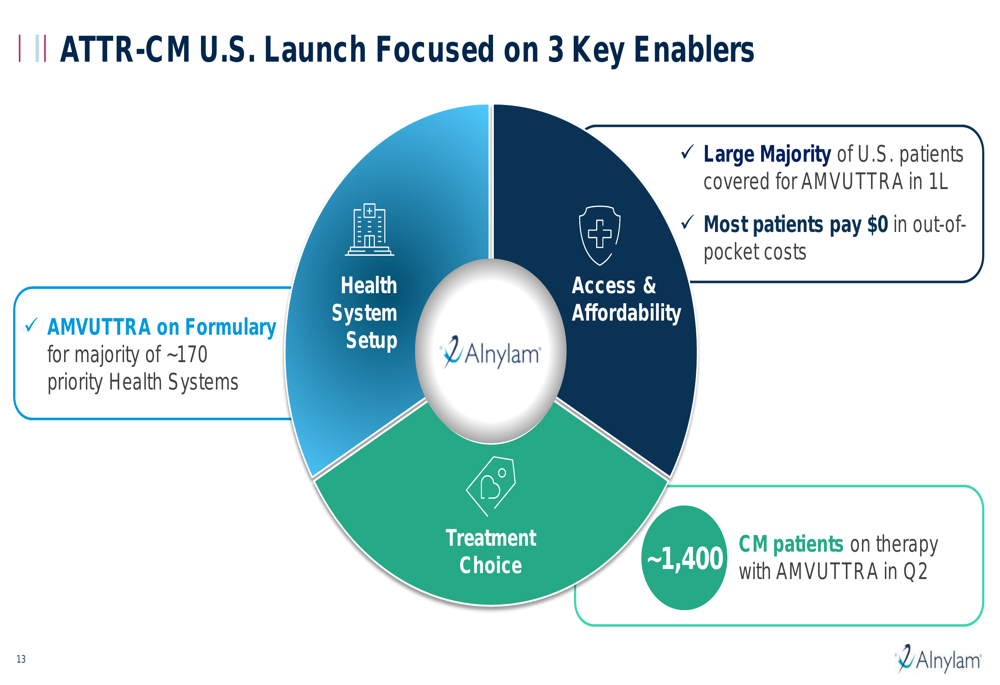

Alnylam’s launch strategy focused on three key enablers: health system setup, access and affordability, and treatment choice. The company reported that AMVUTTRA is now on formulary for the majority of approximately 170 priority health systems, with a large majority of U.S. patients having first-line payer coverage without step-through requirements.

As shown in the following slide detailing the company’s launch enablers:

The company has also made significant progress in expanding access points, with over 2,000 alternate sites of care enabled and approximately 90% of U.S. patients able to receive AMVUTTRA within about 10 miles of home. Most patients are paying $0 in out-of-pocket costs, further supporting adoption.

Pipeline Progress

Beyond its commercial success, Alnylam continues to advance its pipeline of RNAi therapeutics. The company presented additional data from the HELIOS-B study of AMVUTTRA in ATTR-CM, showing a 36% all-cause mortality risk reduction and 33% cardiovascular mortality risk reduction through 42 months, reinforcing the product’s differentiated clinical profile.

The company is also advancing nucresiran, a next-generation TTR silencer with potential for greater TTR knockdown, improved efficacy, and biannual dosing. The TRITON Phase 3 program includes TRITON-CM with a cardiovascular outcomes primary endpoint (targeting launch around 2030) and TRITON-PN (targeting launch several years earlier).

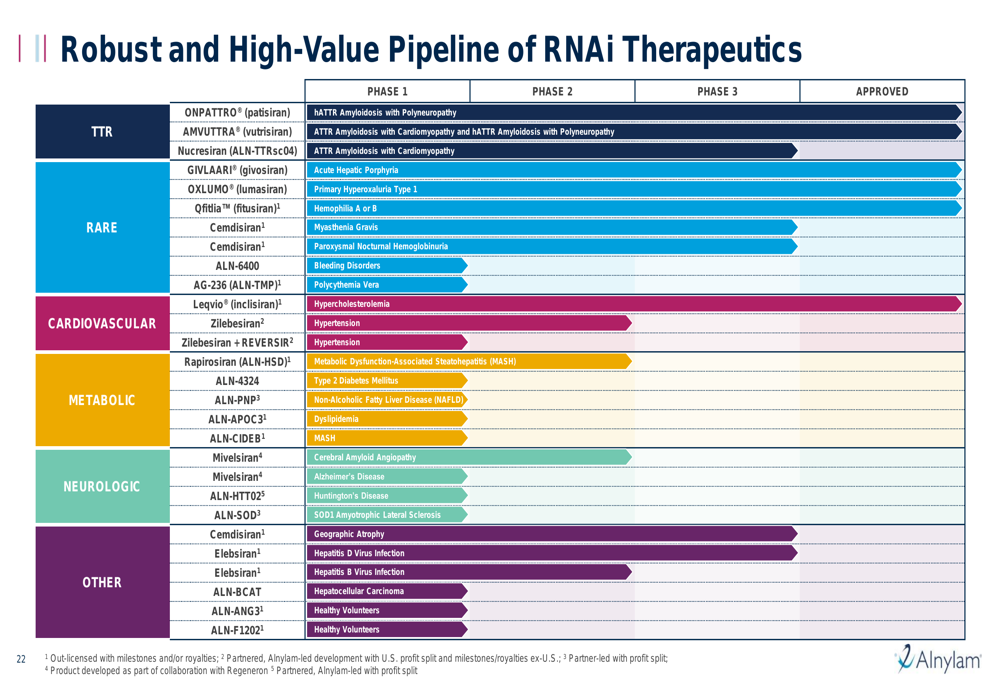

As illustrated in the following overview of Alnylam’s robust pipeline:

Additionally, the company reported encouraging data for mivelsiran in Alzheimer’s disease, showing durable knockdown and tolerability observed for more than one year, with multiple doses providing additional reductions in CSF Aβ42 and Aβ40 levels.

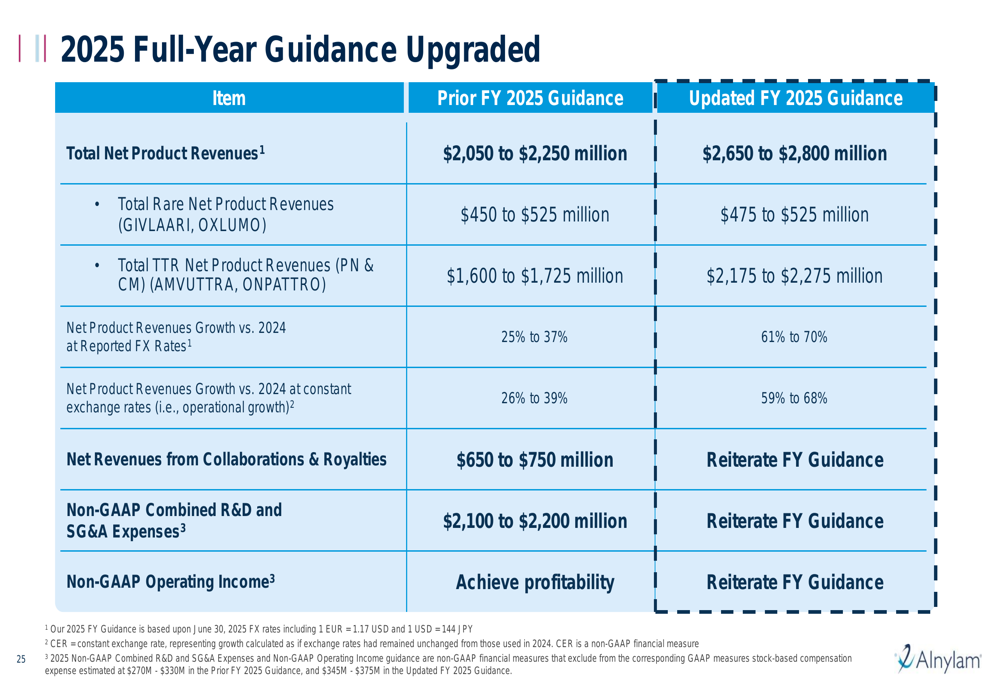

Financial Outlook

Based on the strong Q2 performance, Alnylam has upgraded its full-year 2025 guidance. The company now expects total net product revenues of $2,650 to $2,800 million, representing an increase of $575 million at the midpoint (27% higher than previous guidance).

The updated guidance is broken down as follows:

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.