FULL HEARING VIDEO: Fighting Obamacare Subsidy Fraud: Is the Administrative Procedure Act Working as Intended?

Oral Testimony Transcript

Chairman Van Drew, Chairman Fitzgerald, Ranking Member Crockett, Ranking Member Nadler, and Members of the Committee:

Thank you for the opportunity to testify.

The failures of the Affordable Care Act are well known.

Cancelled health plans.

Soaring premiums and deductibles.

Lost doctors and narrower networks.

The law entrenched an inefficient, insurance-dominated health sector by sending massive subsidies straight to insurance companies.

A new Joint Economic Committee report found that the main winners of the ACA subsidies are health insurers, whose stock prices have soared.

My testimony today will focus on one profound and expanding failure: massive fraud and abuse in the exchanges.

GAO’s work shows how vulnerable the program is to fraud with 96 percent of fake applications enrolling in subsidized coverage.

Paragon’s work shows the staggering cost.

Our research grew out of a single conversation. In May 2024, I testified in Texas. A state senator asked me about techniques being used to inappropriately enroll people in fully subsidized ACA plans. I responded that there were large incentives for abuse, but that I did not know the scale.

Upon returning, I asked my team to do a simple analysis—compare the number of people enrolled claiming income between 100 and 150 percent of the federal poverty level to the number who would be eligible for a plan with that income. Under COVID-era subsidy boosts—the ones set to expire after 2025—coverage was made fully subsidized for people who claimed income in that category.

Using conservative assumptions, we found 5 million more people enrolled in that income category than were eligible in 2024.

Nearly half of all enrollees claimed income in this narrow band—yet more than half of them were not eligible.

In 2024, federal spending on ineligible enrollees likely exceeded $20 billion. We published our findings in a paper entitled, The Great Obamacare Enrollment Fraud.

Others replicated Paragon’s work. They got the same result.

Exchange enrollment had surged, in large part because eligibility rules were ignored. Improper and phantom enrollment took off.

After ignoring the problem for two years, the Biden administration’s actions to penalize some brokers were too little, too late.

As proof of their failure, improper enrollment surged in the last open enrollment period on President Biden’s watch. After open enrollment in 2025, there were 6.4 million people enrolled in fully subsidized plans who were not eligible, at a cost of $27 billion.

Many enrollees were victims, signed up without their knowledge. Some lost plans they liked, and others now face tax penalties.

One customer service agent said that half of the people signed up had no idea they were enrolling in health insurance.

A new study from the Competitive Enterprise Institute shows two times more people enrolled in exchange plans than who report being enrolled.

Automatic re-enrollment has simply shuffled improper eligibility determinations from one year to the next. In 2025, 45 percent of all exchange enrollees took no action and were automatically re-enrolled.

Given widespread improper enrollment and many enrollees unaware of their coverage, we would expect many to never use their plan. The Biden administration refused to release information on zero-claim enrollees. But fortunately, in August, the Trump administration did.

What did we find? A surge in enrollees who never used their plan—no doctor visits, no prescriptions, no lab work. In 2024, nearly 12 million enrollees did not use their plan a single time—up from fewer than 4 million in 2021.

Overall, 35 percent of all exchange enrollees never used their plan, and 40 percent of fully subsidized enrollees did not have a single claim.

Zero-claim exchange enrollees are more than double what occurs in a normal health insurance market and are double the rates before the COVID-era subsidy expansion.

There are unquestionably millions of phantom enrollees in the exchanges. Federal taxpayers sent more than $35 billion to insurers in 2024 for people who never used their plan.

The One Big Beautiful Bill took some important steps to improve exchange program integrity. But the best way to reduce the fraud and waste is for the COVID-era subsidy boosts to expire as scheduled.

That would still leave in place extremely generous subsidies that cover the vast majority of premiums and that grow more generous over time on autopilot.

Thank you. And I look forward to your questions.

Written Testimony

My name is Brian Blase, and I am the founder and president of Paragon Health Institute. From 2017 through 2019, I served as a special assistant to the president for economic policy at the White House’s National Economic Council. From 2011 through 2014, I worked for the House Committee on Oversight and Government Reform under then-Chairman Darrell Issa. I appreciate the opportunity to testify on this important topic. This written testimony was greatly assisted by the work of my colleague, Gabrielle Minarik.

Last month, I testified before the Senate Finance Committee on how government policies drive health insurance and health care costs higher and how we can make health coverage and care more affordable. In today’s testimony, I focus on specific problems with the Affordable Care Act (ACA) exchanges that have led to significant improper enrollment and spending and created a climate that invites, and even rewards, fraud. I first outline general problems with the ACA that have driven premiums higher.

The Affordable Care Act’s Escalating Premiums

The ACA promised affordable, high-quality insurance for individuals and lower health care spending for the nation. It failed to deliver. Premiums and deductibles escalated—often for coverage that excludes the best hospitals and doctors. The law entrenched an inefficient, insurance-dominated health sector with massive subsidies flowing straight from the U.S. Treasury to insurance companies—adding hundreds of billions to the debt since its enactment.

Here are the economic realities of the ACA:

- Its regulations increased premiums for the vast majority of people.

- Subsidies were then needed so people could afford the coverage made more expensive by these regulations.

- The underlying regulatory and subsidy structure leads to ever-escalating premiums and prices.

- Higher premiums create pressure for still more subsidies.

- And those additional subsidies only worsen the underlying problems—fueling the very premium and price escalation they are meant to offset.

The ACA’s regulations drive higher costs. For example, the ACA’s essential health benefit mandates require all plans to cover the same set of services regardless of what consumers want or need for their health. In addition, these rules increase wasteful spending and drive premiums higher.

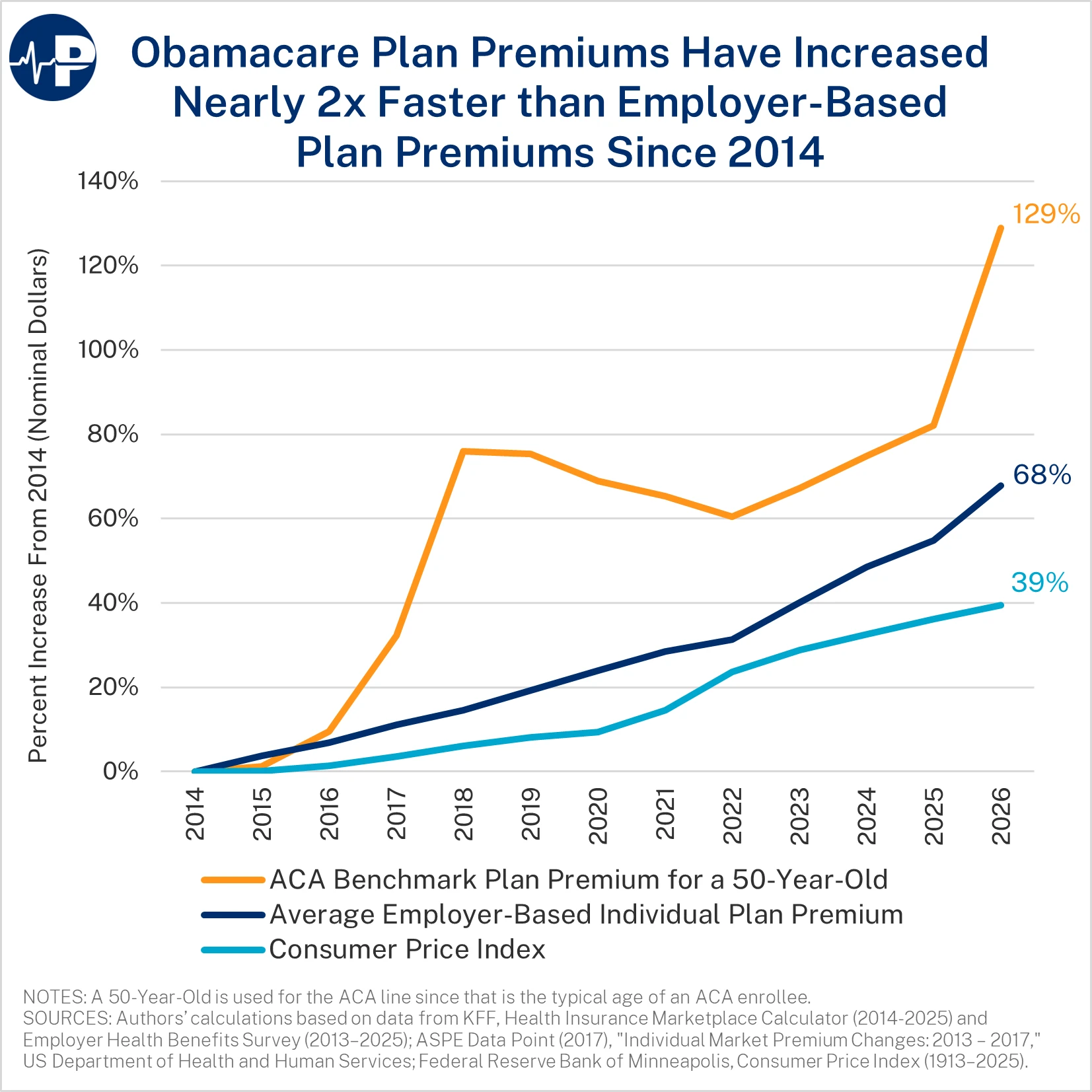

From 2014 to 2026, individual market premiums are up 129 percent, employer-sponsored insurance premiums are up 68 percent, and general inflation is up 39 percent.1 This is after individual market premiums increased nearly 50 percent from 2013 to 2014, the first year the ACA’s regulatory changes took effect.2 In 2026, the average deductible for an individual on a bronze plan is $7,476, and the average deductible for an individual on a silver plan is $5,304.3

During the annual open enrollment period, applicants estimate their household income for the following year, often with the assistance of brokers or agents. Based on this reported income, the government sends monthly subsidies, dubbed advance premium tax credits, to the insurer offering the plan selected by the applicant. Almost all of the subsidies are direct payments from the Treasury to health insurance companies. In many cases, the insurer receives more money than the enrollee was lawfully entitled to during the year—and the insurer gets to keep the excess payments, with some combination of the federal taxpayer taking the loss and the enrollee liable for a portion of the excess payment.

As a temporary pandemic measure, the American Rescue Plan Act increased subsidies for this coverage from 2021 through 2022. It increased taxpayer assistance for exchange plans in two ways. First, it reduced what people with income between 100 and 400 percent of the federal poverty level (FPL) need to pay for a benchmark plan, including making coverage fully subsidized for enrollees claiming income between 100 and 150 percent FPL. Second, it lifted the cap on subsidy eligibility at 400 percent of FPL. The Inflation Reduction Act did not introduce any reforms in the market and continued the expanded subsidies—setting them to expire after 2025.

If Congress wants to make health care more affordable, it must reform the ACA’s broken regulatory and subsidy structure itself, not throw more good taxpayer money after bad. In fact, the surest way to avoid meaningful reform would be to extend the pandemic-era subsidy boosts.

How the ACA’s Subsidy Formula Fuels Premium Inflation

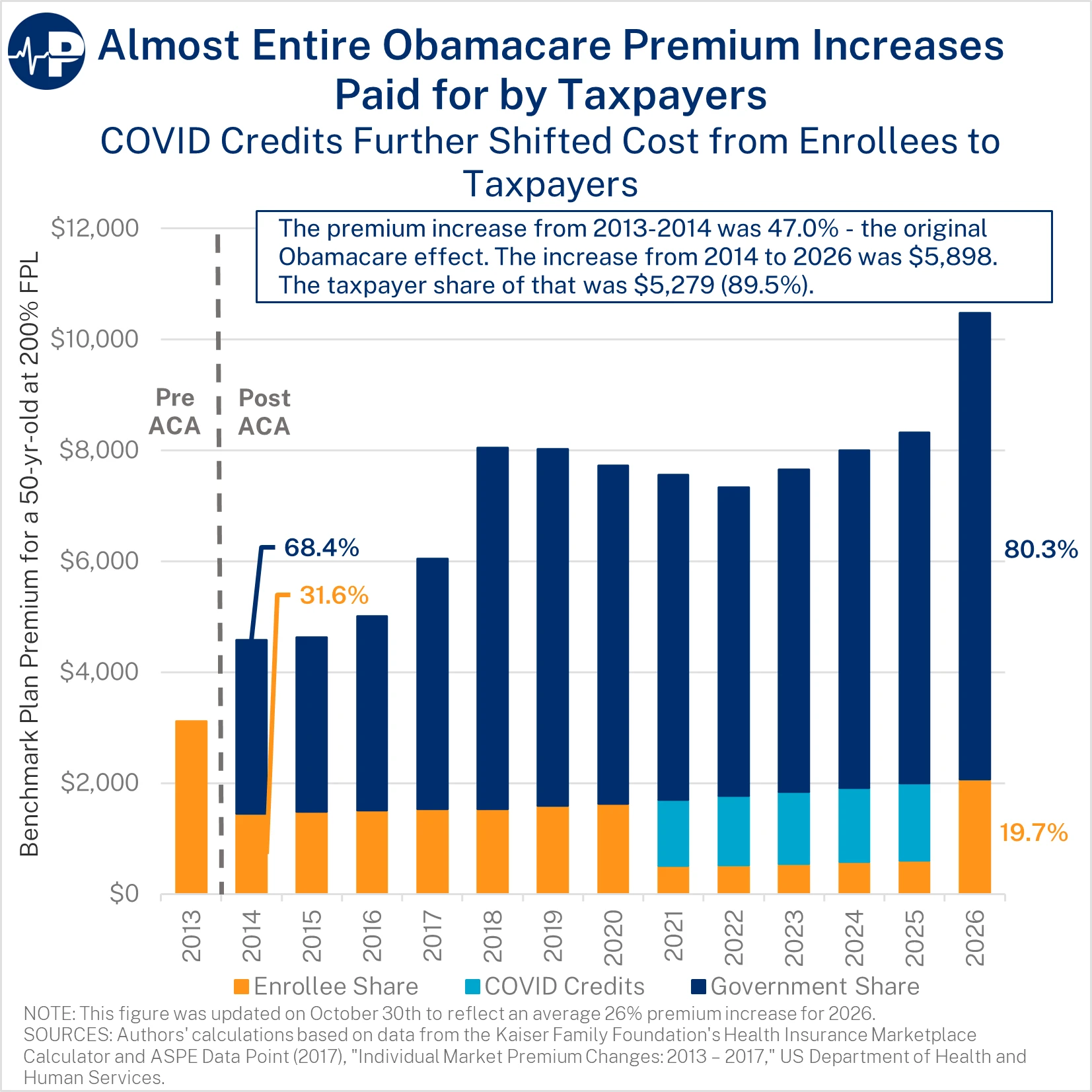

The ACA’s subsidies are ill-designed and inflationary in critical ways. The enrollee’s share of the premium is capped—regardless of the total premium. This structure is inherently different than other federal health programs, such as Medicare Part B and the Federal Employees Health Benefits Program, where enrollees pay a percentage of the premium. The figure below demonstrates the increase in premiums and the split between taxpayer and enrollee from 2014 through 2026 for a 50-year-old enrollee at two times the FPL. (This approximates the average ACA enrollee’s age and income.)

The federal taxpayer share of the premium increased gradually from 68 percent of the premium in 2014 to nearly 80 percent in 2020.4 As a result of the COVID-era subsidy boosts, the federal taxpayer share of the premium reached 93 percent from 2021 through 2025. Next year, when the COVID boosts expire, the federal share will exceed 80 percent. Because enrollees pay only a small slice of the premium, insurers face virtually no price discipline—giving them incentives to inflate costs rather than improve value.

The ACA subsidy structure does not just fail to control costs—it actively rewards insurers for raising them. A recent analysis by the Joint Economic Committee shows that consumers capture only 34 percent of the benefit, with roughly two-thirds captured by insurers through higher premiums and inflated benchmark prices.5 This occurs because subsidies automatically increase as premiums rise, insulating insurers from competition and enabling them to absorb most of the subsidies rather than pass savings on to enrollees.

ACA premiums will rise next year because of underlying flaws with the program and growing cost pressures. Only a small portion of the increase is from the expiring COVID subsidy boosts. As the next figure shows only 3.3 percent of the 2026 premium is from the expiration of the COVID subsidy boosts.6

How COVID-era Subsidy Boosts and Lax Oversight Produced Widespread Fraud

The enhanced subsidies transformed the exchanges into an environment where misstatements and unauthorized enrollments became highly profitable. Pandemic-era policies that suspended tax-filing and reconciliation requirements weakened the few guardrails that previously existed and opened the door to large-scale improper enrollment.

CBO’s most recent ACA subsidy baseline projection is 91 percent above its 2021 projection over the 2026–2033 period.7 Continuing the COVID credits would result in deficits about $40 billion a year higher over the next decade.

Many of those improperly enrolled do not even know about their coverage, as they are victims of fraud schemes designed to pocket commissions and subsidies. This is evidenced by the rising percentage of people who do not use their coverage at all, the rising number of government enforcement actions, and news stories and investigations.

Improper Enrollment Pressures Exacerbated by the COVID Subsidy Boosts

Improper enrollment is not a marginal issue—it is now one of the defining characteristics of the ACA exchanges, driven by a perverse subsidy design, weak documentation rules, and financial incentives that reward misrepresentation. From 2015 to 2020, exchange enrollment averaged about 10–11 million people8—about 60 percent below what the Congressional Budget Office (CBO) projected in May 2013 in its last analysis before the ACA’s provisions took effect.9 The sharp enrollment increase after 2021 did not reflect improved value; it reflected a surge of government subsidies, widespread income misrepresentation, relaxed verification rules, and aggressive third-party enrollment tactics that prioritized volume over accuracy.

COVID Subsidy Boosts Created Financial Incentives for Misreporting and Manipulation

COVID-era subsidy boosts resulted in fully subsidized coverage for people claiming income within a category—100 to 150 percent of FPL. This policy change created large financial incentives for applicants—and those allegedly acting on their behalf—to misstate income and enroll in this income category. In a June 2025 paper that I coauthored, we found the amount of improper enrollment grew substantially between 2024 and 2025 for those claiming income between 100 and 150 percent of FPL.10 The number of ineligible enrollees rose from an estimated 5.0 million to 6.4 million from 2024 to 2025. In total, 29 states had more sign-ups in this income category than the number of eligible individuals in the population, based on our conservative methodology for determining improper enrollment.11 In 15 states, there are more than twice as many enrollees in fully subsidized plans than are eligible. The estimated cost to taxpayers from this improper enrollment will likely exceed $27 billion in 2025 alone. Under more expansive assumptions, the number of ineligible enrollees in 2025 could reach as high as 7.1 million. The sheer scale of these discrepancies makes clear that improper enrollment is not incidental but systemic to the program.

Fraud, Misrepresentation, and Unauthorized Enrollment Are Widespread

Fraudsters took advantage of these relaxed eligibility checks. Many enrollees were signed up without their knowledge or consent. A recent Bloomberg investigation highlighted how large-scale deception rings take advantage of these perverse incentives, with some enrollees being coached on how to fill out their applications to take advantage of the fully subsidized coverage and some brokers and agents just enrolling people without their consent. Tactics include misleading “cash benefit” ads, aggressive lead-generation funnels, and brokers submitting applications without consent.12 One former customer service worker at a large brokerage firm said, “Half the time they didn’t even know they were signing up for insurance.”13

Lead generation companies used deceptive digital advertising to target lower-income Americans—promising “$0 coverage.” Some ads featured deepfake impersonations of Taylor Swift, Joe Rogan, Andrew Tate, Dr. Phil, and Steve Harvey on TikTok, claiming, “They’re giving out $6,400 to anyone who makes the call.” Once consumers click, they are prompted to enter a name, date of birth, state, and phone number—more than enough for a web broker to create or access an application. This information is then sold to brokerages and call centers. One call center made enough money to sponsor a NASCAR team, and former employees told Bloomberg that “almost all the callers were looking for cash cards, not insurance.” As one former agent put it: “You have to throw away a little bit of your morality.” This deceptive ad ecosystem exists because enrolling a fully subsidized consumer—even fraudulently—guarantees commissions for brokers and monthly federal payments for insurers, with essentially no downside risk for either.

The Centers for Medicare and Medicaid Services (CMS) received more than 200,000 complaints about unauthorized plan switches in 2024 alone.14 In 2025, the Department of Justice brought charges against insurance executives accused of defrauding taxpayers out of more than $160 million.15 In addition, a Florida-based brokerage executive pled guilty to a separate $133 million scheme that targeted homeless and mentally ill individuals to improperly enroll them in subsidized ACA plans.16

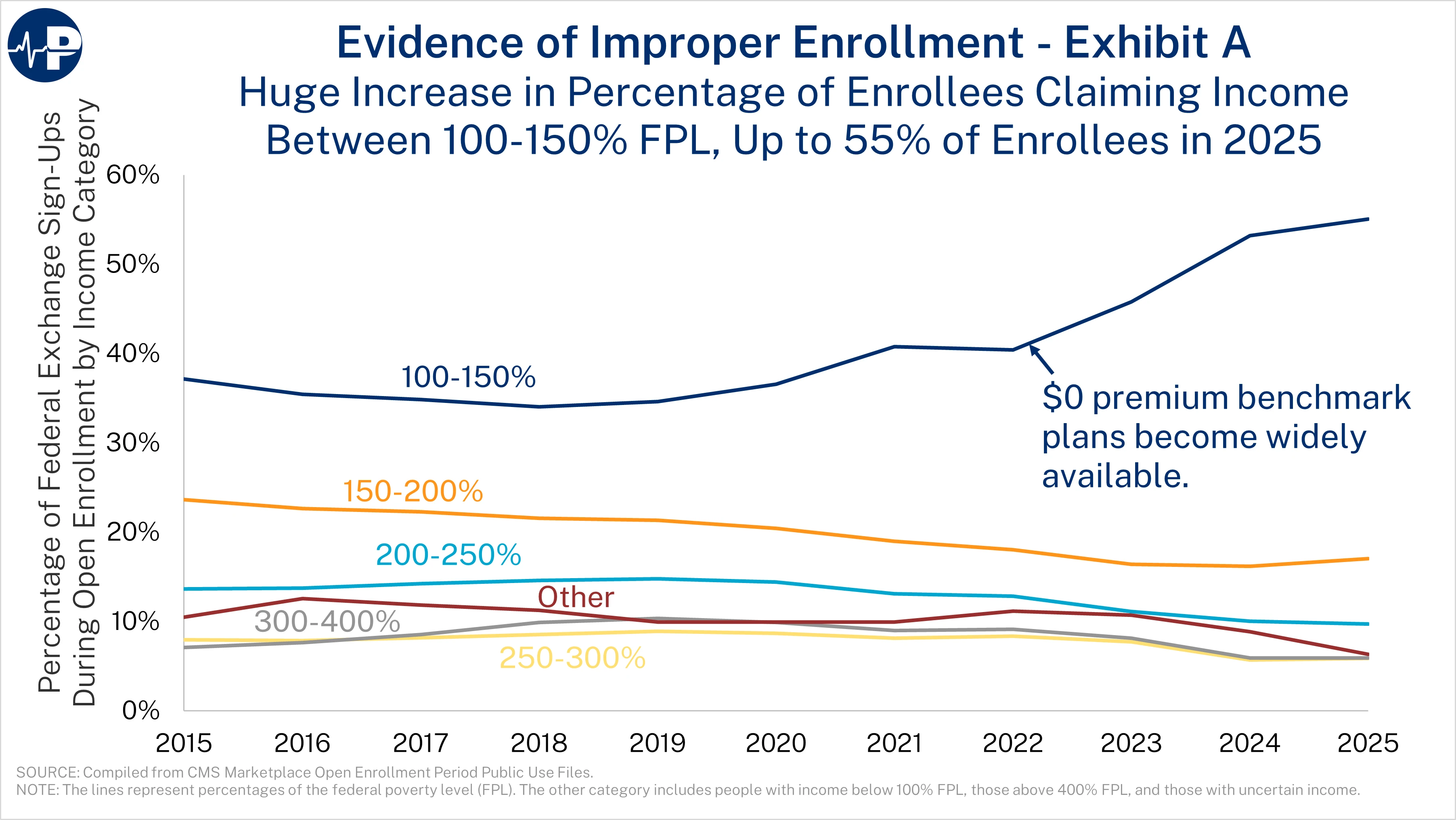

Four figures demonstrate the large scale of improper enrollment. The first figure shows the shift in overall enrollment to the lowest income category in the states that use HealthCare.gov. The first open enrollment period with fully subsidized plans was 2022.

By 2025, a stunning 55 percent of people who signed up for coverage during open enrollment reported that their income was between 100 and 150 percent of FPL.17 This figure shows only the federal exchange sign-ups, because not all states with state-based exchanges reported sign-ups by income grouping prior to 2022. We estimate that 62 percent of individuals reporting income between 100 and 150 percent of FPL in HealthCare.gov states are not actually eligible, meaning that for every two eligible enrollees, there are more than three ineligible enrollees in this category. Improper enrollment is further illustrated by the unprecedented surge in people who never use their coverage.

Zero-Claim and Phantom Enrollment Has Exploded

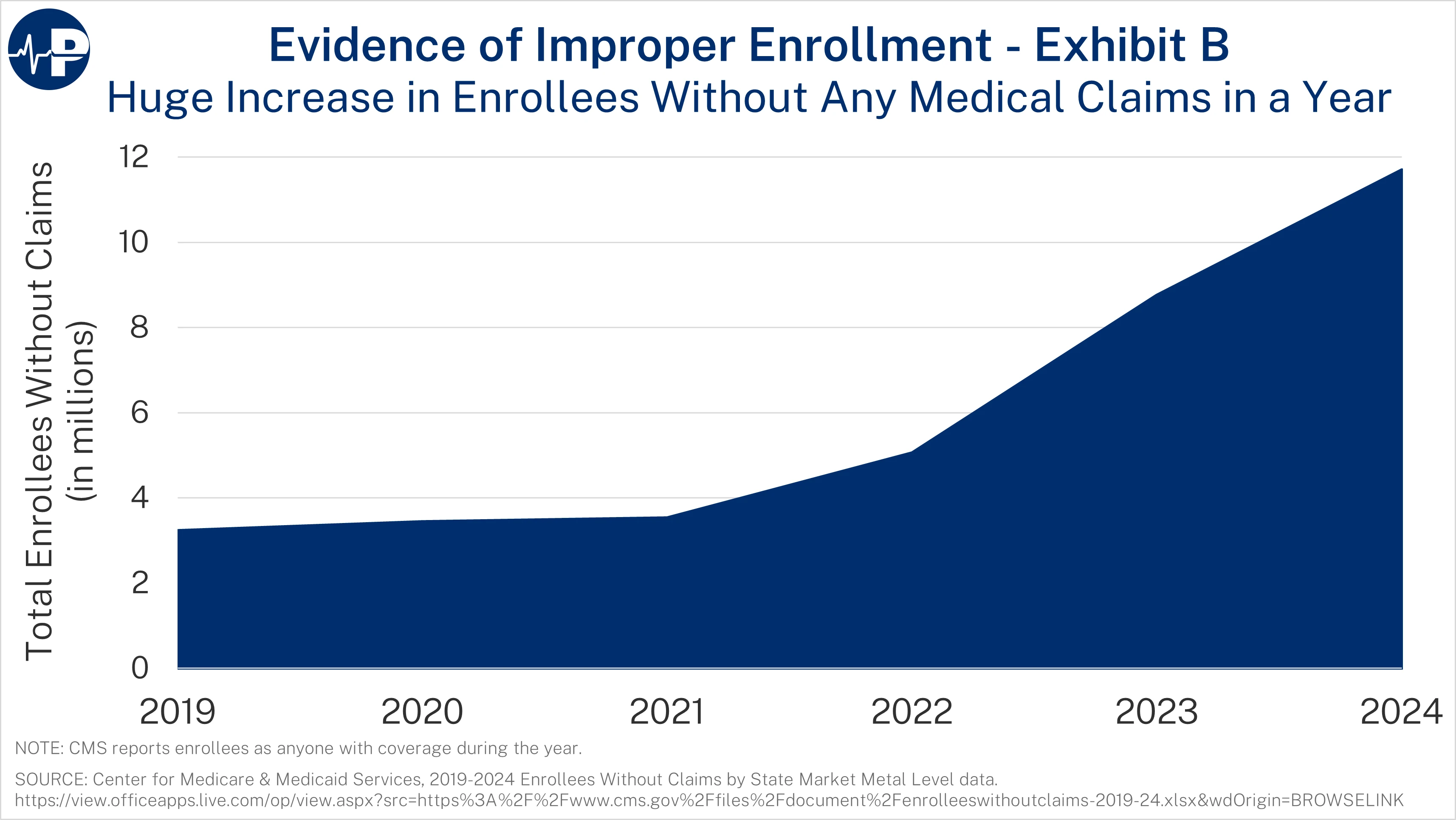

The next figure shows the explosive growth in zero-claim enrollees. From 2021 to 2024, the number of ACA exchange enrollees who did not use their plans for a single service tripled, reaching almost 12 million people.18 The zero-claim enrollment data include anyone enrolled during the year. Overall, 35 percent of enrollees did not use their plans a single time. A staggering 40 percent of fully subsidized enrollees used no medical services in 2024. These percentages are up from 19 and 20 percent, respectively, in 2021. Many of these zero-claim enrollees are “phantoms”—people who are unaware of their enrollment in the program or have duplicate coverage. Federal taxpayers sent more than $35 billion to insurers for people who did not use their plans a single time. In contrast, only 15 percent of people with private health insurance typically do not use their plans at all.19 When 40 percent of fully subsidized enrollees use no services—not even free preventive care—the most plausible explanation is that a large share were improperly enrolled, enrolled without consent, or enrolled solely for the purpose of generating subsidies.

These patterns persist despite aggressive insurer marketing that emphasizes free preventive care. If millions of people with $0 premiums are not accessing even free and commonly recommended services, the most plausible explanation is that a significant share were either enrolled improperly, enrolled without their knowledge, or enrolled but never intended to use coverage. These findings are consistent with new data from the Centers for Medicare & Medicaid Services, which identified 1.6 million people simultaneously enrolled in both Medicaid and ACA exchange plans.20

Meanwhile, yet another data study (see figure: “Obamacare enrollment: CMS vs CPS”), this one from Jeremy Nighohossian of the Competitive Enterprise Institute, is also suggestive of a surge of phantom enrollment in the ACA exchanges. According to Nighohossian’s review of federal data, twice as many people were enrolled in exchange plans in 2024 as reported having coverage, a much larger gap than in the years prior to the COVID credits.21

The collapse of demographic reporting further signals large-scale improper or unauthorized enrollment. In 2024 and 2025, the exchanges lacked race or ethnicity data for more than half of enrollees—a dramatic shift from 2021.22 This is yet another indication that many enrollees were likely signed up by agents or brokers who did not really know the applicant—obtaining only the minimum amount of information to get them enrolled in fully subsidized plans.

The Congressional Budget Office has confirmed that large amounts of improper enrollment permeate the exchanges. According to CBO, there are 2.3 million ineligible enrollees in the 100 to 150 percent FPL category in the 10 non-Medicaid expansion states who have overestimated their income to unlawfully qualify for a subsidy.23 CBO did not assess the other 40 states that adopted Medicaid expansion and did not assess the problem of people in the non-expansion states who underestimated their income to qualify for fully subsidized plans. Thus, CBO’s estimates are in-line with Paragon’s estimates of improper exchange enrollment.

Turning the Exchanges into a Wild West Where Fraud and Abuse Flourish

Bad policy and negligent oversight reward those who misstate income, and allow third parties to enroll individuals without consent, provide year-round access to fully subsidized plans without documentation, automatically renew improper or fraudulent enrollments, and compensate brokers in ways that create powerful incentives to exploit enrollees rather than assist them. And taxpayers are footing the bill—tens of billions of dollars for coverage that provides no value and undermines the integrity of the ACA. Moreover, enrollment fraud harms more than just taxpayers. When individuals are fraudulently enrolled despite having employer coverage or income above eligibility thresholds, they become legally responsible for repaying subsidies—often thousands of dollars—despite never having chosen the coverage. Many do not learn they were enrolled until the IRS rejects their tax return for missing Form 1095-A. Because CMS suspended enforcement of reconciliation rules between 2021 and 2024, millions of individuals continued receiving subsidies without filing taxes—creating enormous potential liabilities for innocent Americans who never chose these plans.

Here are the stories from just a few of the recent victims:

Mary Zhelyazkova of Miami, Florida,24 while struggling with addiction and homelessness, needed Suboxone to manage opioid withdrawal. She was receiving it for free through the Ryan White program—until an unscrupulous broker offered her $5 to sign up for a “free” ACA plan. What she did not know: the broker used fake information to get her enrolled in a plan she did not qualify for. That plan disqualified her from the Ryan White program, charged her copays she could not afford, and left her without access to medication. She went into withdrawal. She suffered. And the unscrupulous broker walked away with a commission.

Ashley Zukoski, an ultrasound technologist in Charlotte, North Carolina,25 had employer coverage but now faces a tax bill for an ACA plan she said she never signed up for. Ashley now faces a $700 tax penalty instead of a $4,100 refund as a result of being enrolled in a fully subsidized ACA plan without her knowledge or consent.

Michael Debriae of North Carolina26 was enrolled in an ACA plan without his consent two months after cancelling previous ACA coverage due to receiving employer coverage. Debriae now must pay back the $2,445 in premium tax credits paid to the insurer from less than four months of coverage.

Lorie and Randy Delaney of Ohio27 had their ACA plan repeatedly changed without their knowledge and faced thousands of dollars in additional prescription costs. They realized something was wrong when Randy’s insulin prescription cost $1,096—far more than expected. Lorie contacted the exchange and learned their plan had been changed from Medical Mutual to United Healthcare by an insurance broker in Texas, whom they had never interacted with.

All of these elements—zero-premium plans, lax documentation, and EDE vulnerabilities—combined to produce a marketplace with almost no functional guardrails. As a result of expanded subsidies and lax Biden administration oversight, the exchanges became a “wild west” atmosphere, as described by one broker.28 The evidence is clear: Following the law has been optional.

Unscrupulous brokers and fraudulent entities make commissions they never would have earned, and insurers acquire additional customers whose premiums are largely—and often entirely—paid by the government. Moreover, these enrollees receive premium and out-of-pocket cost subsidies for which they are not eligible, and they often do not need to be fully paid back if their actual income turns out to be different than the income that they claim.29 This is a preventable, policy-driven scandal—one that knowingly prioritized increasing enrollment numbers over basic program integrity.

During the Biden administration and potentially still true today, CMS has permitted deceptive marketing practices, a marked contrast to its oversight of the marketing for Medicare Advantage plans. CMS’s failure led to large conglomerate practices of third-party Enhanced Direct Enrollment (EDE) firms. Enhanced direct enrollment platforms—a feature of the federal exchange (HealthCare.gov) but not state-based exchanges, enables brokers and agents, including web brokers, to more easily enroll people in coverage through integration with HealthCare.gov.

To date, CMS enforcement action has been limited to individual brokers, despite sophisticated fraud and large-scale improper enrollment primarily originating from EDE firms. EDE platforms exploited the COVID-era subsidy boosts plus weak income verification rules to manipulate eligibility and enroll ineligible people into coverage.

EDE platforms allow brokers and agents to access or create applications with only a name, date of birth, and state—far less information than is needed to actually verify identity or eligibility. Until April 2024, any agent or broker could view a consumer’s full Social Security number on HealthCare.gov, enabling rogue agents and EDEs to harvest identity information, reuse it, or reenroll people without their knowledge.30 While the full SSN is no longer supposed to be visible, an enrollee’s last four digits can still be accessed.

Additionally, EDE platforms exploit regulations and standards surrounding National Producer Number (NPN) overrides, allowing one broker to submit applications under another broker’s ID. This eliminates any clear line of accountability and creates a structure where fraudulent agencies can enroll thousands of people using a single NPN.

For example, one of the most egregious examples occurred in September 2024 when CMS suspended Speridian Health, an EDE entity that processed more than one million exchange applications.31 CMS cited credible evidence that Speridian altered exchange applications, enrolled people without their consent, and routed large volumes of enrollment traffic through overseas IP addresses in Hong Kong, India, Japan, Pakistan, Ireland, and Sweden. These weaknesses explain how large-scale unauthorized changes and fraudulent enrollments occurred without consumer consent.

The Biden administration created a year-round special enrollment period (SEP) for those claiming income between 100 percent and 150 percent FPL, creating more opportunities for unscrupulous brokers to perpetrate fraud. Fortunately, the Working Families Tax Cut Act shut down this SEP to better safeguard against fraudulent activity.

One particularly galling problem involved the intersection of zero-premium plans with the year-round Native American Special Enrollment Period.32 In 2025, Blue Cross Blue Shield (BCBS) of Oklahoma uncovered a “body brokering” scheme in which vulnerable Native Americans and homeless individuals were recruited, coached to misstate income, enrolled in zero-premium exchange plans, and transported to out-of-state treatment centers that billed insurers for tens of millions in fraudulent claims.33,34 BCBS Wyoming similarly reported a “significant health care fraud scheme” involving over 1,500 potentially fraudulent enrollments—fewer than 40 of which were legitimate.35 These cases show how SEPs combined with zero-dollar premiums are taking advantage of some of the most vulnerable communities in the country.

Insurance companies have full discretion to terminate contracts and rescind commissions with brokers who engage in misconduct or submit questionable applications. But in practice, they rarely do. The monthly payments insurers receive from the U.S. Treasury for each enrolled individual—regardless of the enrollee’s eligibility—create strong financial incentives to look the other way. As long as the subsidies keep flowing, there is little appetite to disrupt arrangements that drive volume, even when that volume is built on fraudulent or unethical practices.

Under current law, health insurance agents and brokers are prohibited from charging consumers directly for their services, meaning their income is dependent on commission payments from insurance carriers. This structure places ethical, independent brokers at a disadvantage when carriers refuse to police fraud within their networks. As unscrupulous brokers exploit the system to generate high-volume enrollments—often through questionable or outright fraudulent means—they continue receiving commissions. Meanwhile, legitimate brokers lose out on business, face reduced opportunities, and watch resources flow to bad actors who game the system with impunity.

The wild west atmosphere within the exchanges rewarded bad actors and punished good ones. Insurers, focused on maximizing enrollment, face little downside risk from continuing to contract with brokers who manipulate or falsify applications while shutting out ethical or independent brokers who play by the rules. The result is a program where fraud is tolerated, integrity is discouraged, and responsible intermediaries are pushed out—further entrenching abuse in the ACA.

Department of Justice Actions Against the Fraud

Federal prosecutors have now begun to intervene, underscoring how pervasive and profitable ACA exchange fraud has become. On November 17, 2025, the DOJ convicted a president of an insurance brokerage firm and a CEO of an insurance marketing company of orchestrating a massive exchange enrollment fraud scheme that sought over $233 million in fraudulent ACA plan subsidies for which the federal government paid at least $180 million. This case marks one of the first federal crackdowns on unscrupulous brokers and business models exploiting gaping vulnerabilities with the ACA exchanges to manufacture and submit fraudulent enrollments to rake in millions in commissions. “The defendants exploited a health care safety net designed for working families to carry out a $233 million scheme to defraud taxpayers,” said Acting Assistant Attorney General Matthew R. Galeotti of the Justice Department’s Criminal Division. According to the DOJ:

[Defendants] targeted vulnerable, low-income individuals experiencing homelessness, unemployment, and mental health and substance abuse disorders, and, through ‘street marketers’ working on their behalf, sometimes offered bribes to induce those individuals to enroll in subsidized ACA plans.

In April 2025, DOJ announced that a Florida insurance brokerage executive, Dafud Iza, pled guilty to a scheme to “fraudulently enroll ineligible individuals into ACA plans that offered tax credits to eligible enrollees.”36 According to DOJ, “Iza and his accomplices deceptively marketed subsidized ACA plans to ineligible consumers and falsely inflated consumers’ incomes to obtain the federal subsidies.” They even targeted vulnerable individuals, such as “low-income individuals experiencing homelessness, unemployment, and mental health and substance abuse disorders.”37

GAO Confirms Large-Scale Vulnerabilities in Exchanges: 96 Percent of Fake Applications Approved

A new undercover investigation by the Government Accountability Office (GAO) reveals just how fundamentally broken and vulnerable the ACA exchanges remain.38 GAO submitted 24 fictitious applications using fake identities, fake documents, and invalid Social Security numbers. The exchanges approved 23 out of 24—an astonishing 96% approval rate. And as GAO notes, these findings are “generally consistent” with its investigations from nearly a decade ago. In other words, nothing has improved. The system is still wide open.

The failures did not stop with initial enrollment. Eighteen of the GAO’s fake enrollees were still receiving subsidized coverage months later, meaning insurers continued to collect premium tax credits for people who do not exist. These phantom enrollees mirror what we are seeing across the country: a system that rewards volume, ignores verification, and has almost no mechanisms to detect or remove ineligible or nonexistent enrollees.39

GAO also uncovered egregious identity-verification failures. More than 66,000 Social Security numbers showed over 366 days of coverage in 2024, including one SSN used to generate more than 26,000 days of subsidized coverage across 125 different policies. Another 58,000 SSNs belonged to deceased individuals, with thousands showing enrollment beginning after the date of death. These are not minor errors—they reflect a program architecture that cannot reliably distinguish a real applicant from a synthetic identity or a dead person.

In addition, the IRS has no record of tax reconciliation for over $21 billion in premium tax credits for 2023 enrollees with SSNs. For years, CMS simply stopped enforcing the statutory requirement that recipients file taxes and reconcile subsidies. When the federal government abandons the most basic eligibility safeguard in the program, the inevitable result is the explosion of improper enrollment and fraudulent submissions we are witnessing today.

The ACA exchanges have become a high-risk environment for fraud, abuse, and improper payments. They routinely approve fake people, retain them on the books, pay insurers for them, and lack the oversight tools necessary to ensure program integrity. These latest GAO findings confirm what independent analyses and real-world cases have shown: the exchange system is structurally incapable of preventing large-scale fraud and continues to hemorrhage taxpayer funds as a result.

Important Exchange Integrity Reforms in the One Big Beautiful Bill

The OBBB includes several important program-integrity reforms that would meaningfully strengthen eligibility rules and prevent some of the abuses now documented in GAO investigations, DOJ prosecutions, and independent research. While each of these provisions is needed, it is critical to recognize that they address symptoms of the larger problem. The primary driver of fraud is the wide availability of zero-premium plans, which eliminates any financial stake for enrollees and creates irresistible opportunities for brokers and intermediaries to enroll people without their knowledge or consent. As long as millions of enrollees face a $0 premium, the exchanges will remain highly susceptible to fraud—no matter how strong the administrative guardrails. Ensuring that everyone pays at least some premium is the single most important step Congress can take to restore integrity to the exchanges.

Starting in 2028, Section 71303 restores a fundamental program-integrity tool: verification before enrollment. Requiring consumers to affirm their coverage annually and requiring exchanges to verify eligibility up front will reduce improper and fraudulent enrollment.

Starting in 2026, Section 71304 eliminates the year-round special enrollment period for people claiming incomes between 100 percent and 150 percent of the federal poverty level—a provision never authorized in the original ACA and repeatedly exploited by unscrupulous brokers. CMS reported that this SEP generated tens of thousands of complaints about improper enrollments and unauthorized plan switches in just the first three months of 2024. Ending this SEP will improve the risk pool and sharply reduce opportunities for fraud.

Starting in 2026, Section 71305 removes the ACA’s caps on repayment of excess subsidies for people who underestimate their income—or brokers acting on their behalf—to claim excessive subsidies, eliminating a powerful incentive to misstate income. Under current law, many enrollees who underreport income face only modest repayment obligations—even if they received thousands of dollars in excess subsidies.

These statutory reforms are essential, and they provide far more durable protections than administrative actions alone. The Trump administration issued a smart program-integrity regulation addressing many of these problems, but much of it has been stayed by a single judge. That experience demonstrates a central limitation of relying on regulation alone: a single judge can block key safeguards for years.

Ultimately, however, even the strongest statutory oversight cannot overcome the structural incentive created by zero-premium plans. When individuals can be enrolled in coverage without paying anything, they have little reason to monitor their accounts, verify eligibility, or report fraud—and brokers have every reason to enroll as many people as possible, regardless of eligibility. Requiring every enrollee to contribute something to the cost of coverage would dramatically reduce fraudulent enrollments and align incentives across consumers, brokers, insurers, and taxpayers. The most effective path is for the COVID-era subsidy boosts to expire after this year and for Congress to require a minimum premium payment from every enrollee, regardless of plan. Without this change, fraud will remain embedded in the program’s financial architecture.

Other Problems with the ACA: Harming Workers with Employer-Based Coverage, Employers Dropping Coverage, Incentivizing Early Retirement, Punishing Upward Mobility

Beyond fueling fraud and phantom enrollment, the ACA’s subsidy design—especially with the COVID-era subsidy boosts—harms work, productivity, and people who obtain coverage through a job. CBO has concluded that the enhanced subsidies in the Inflation Reduction Act increase deficits, reduce labor supply, and lower long-run economic output by diminishing the financial returns to work.40 When government will heavily subsidize coverage for those who earn less or retire early, people respond: some work fewer hours, some leave the labor force altogether. Lifting the original income cap so that subsidies extend well above four times the poverty line has even encouraged early retirement. It has produced situations such as a retired couple in their mid-50s with $136,000 in pension income from government service receiving roughly $15,000 in ACA subsidies—federal dollars that both reward non-work and crowd out resources that could be better targeted.41

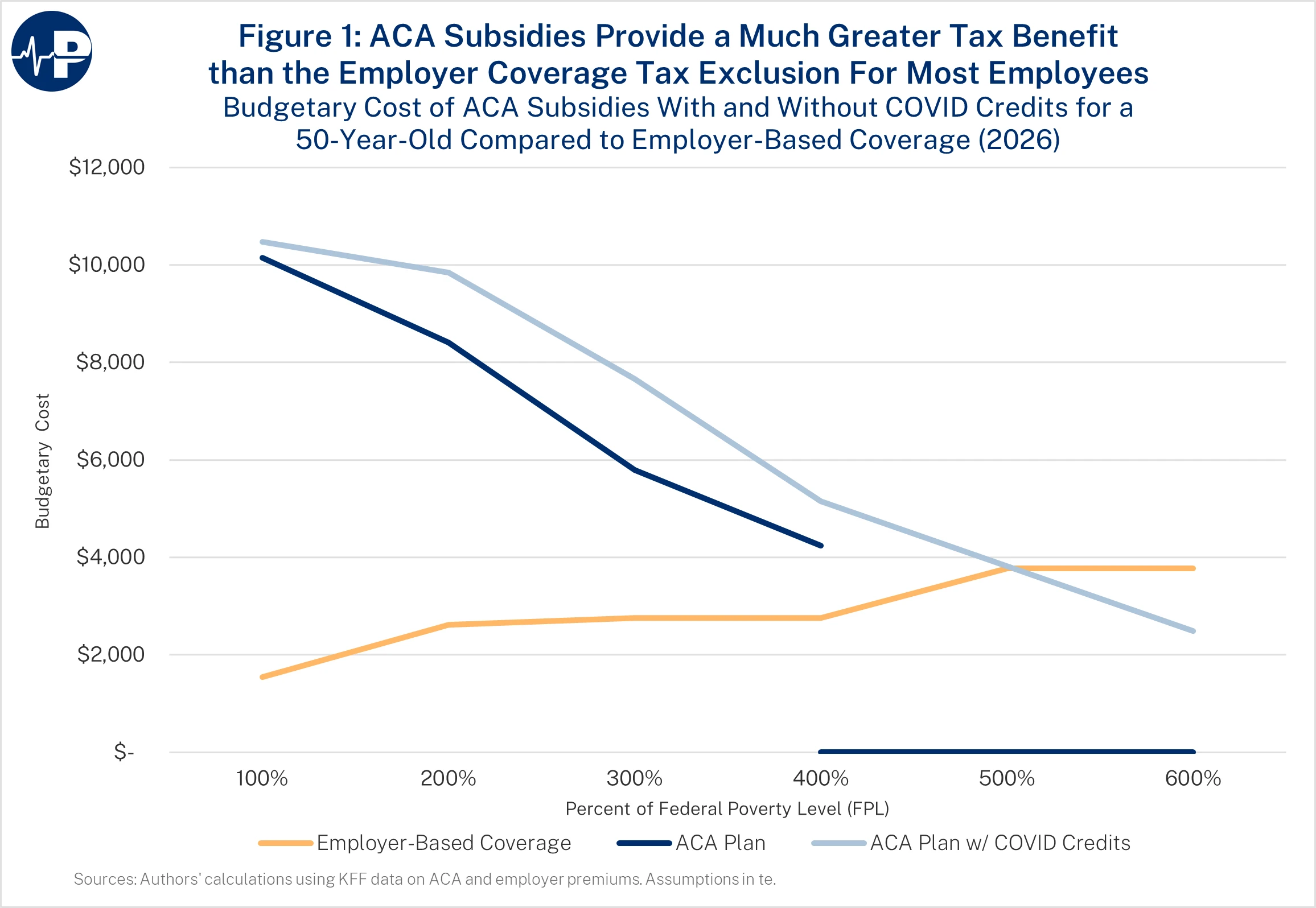

At the same time, the ACA penalizes people who earn their health benefits at work and pressures small employers to drop coverage.42 The tax exclusion for employer-sponsored insurance reduces income and payroll taxes on premiums, but for low- and middle-income households the value of that tax break is dwarfed by what they can receive through ACA subsidies—especially with the COVID add-ons (see figure: “ACA Subsidies Provide Much Greater Tax Benefit”). For a typical young family at twice the poverty line, the original ACA subsidy is already more than three times as large as the tax benefit for job-based coverage; with the Biden COVID subsidy boosts, the gap grows even larger, turning that advantage into a five-figure government penalty for receiving coverage at work.43

Take a young family with 35-year-old parents and two children, ages 7 and 10 years. If the family’s income is $64,300 (200 percent of the federal poverty level), it will receive an original ACA subsidy of $19,059. The tax break for an employer-based health plan for the family would be only $5,904 (in a state with no income tax). The difference is a $13,155 net government benefit for not receiving coverage at work. However, if Congress extends the Biden COVID subsidy boosts, the family’s subsidy would be $22,017, and the net government penalty for receiving coverage at work would increase to $16,113.44

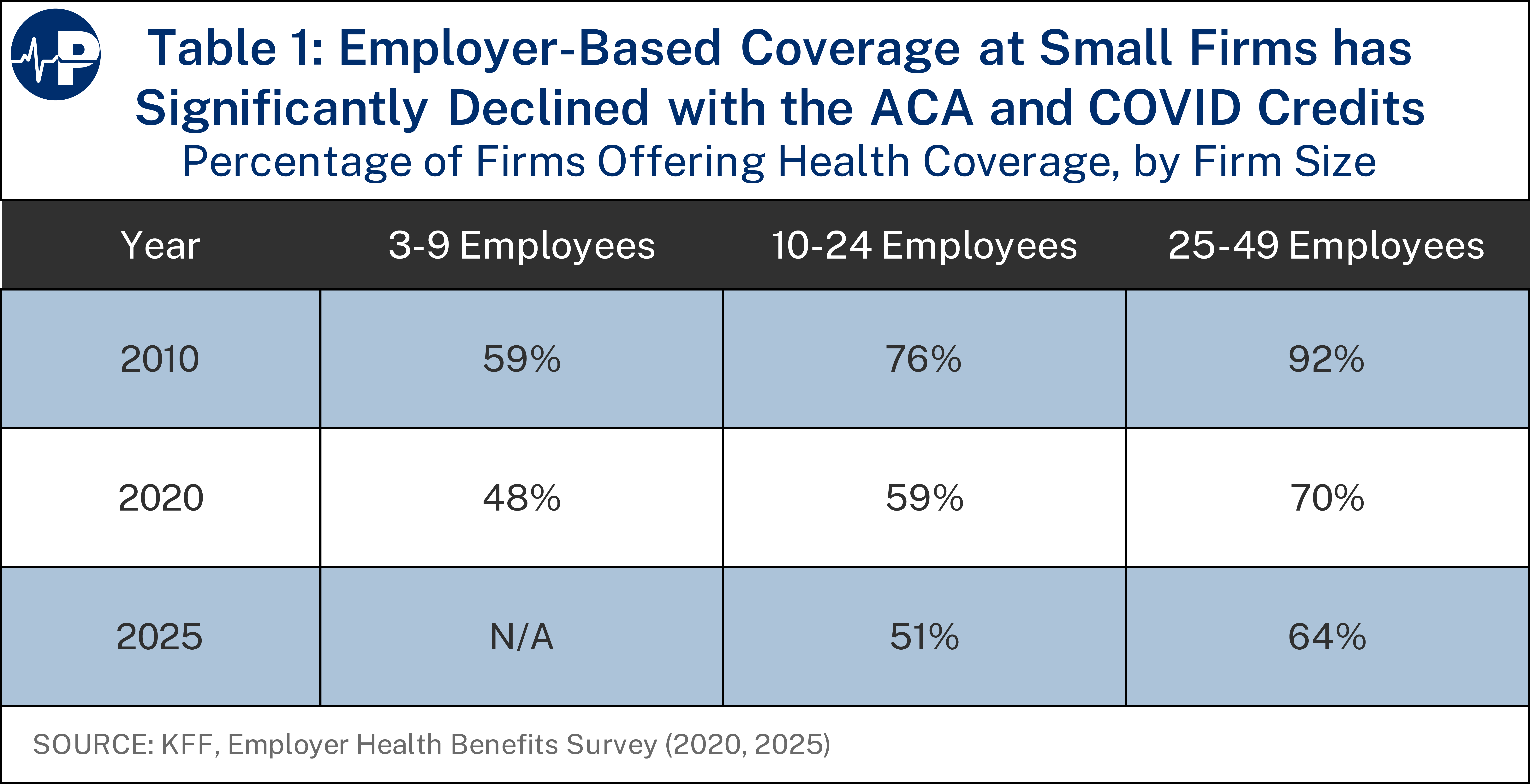

CBO projects that over 4 million people would replace employer or unsubsidized individual coverage with subsidized exchange plans if the COVID credits are made permanent. 45 And the share of small employers offering health plans has already fallen by about one-third since 2010, shifting millions into a more expensive federal program.46

From a federal budget standpoint, this is deeply problematic: employer coverage costs taxpayers roughly one-third as much per enrollee as Medicaid, CHIP, or exchange subsidies. 47 The ACA also led state and local governments to drop retiree health coverage and push early retirees under age 65 into the exchanges, offloading their own obligations onto federal taxpayers—an offloading that will accelerate if the COVID credits are extended.48

Enrollee Share of the Premium Will be Low Next Year When COVID Subsidy Boosts Expire

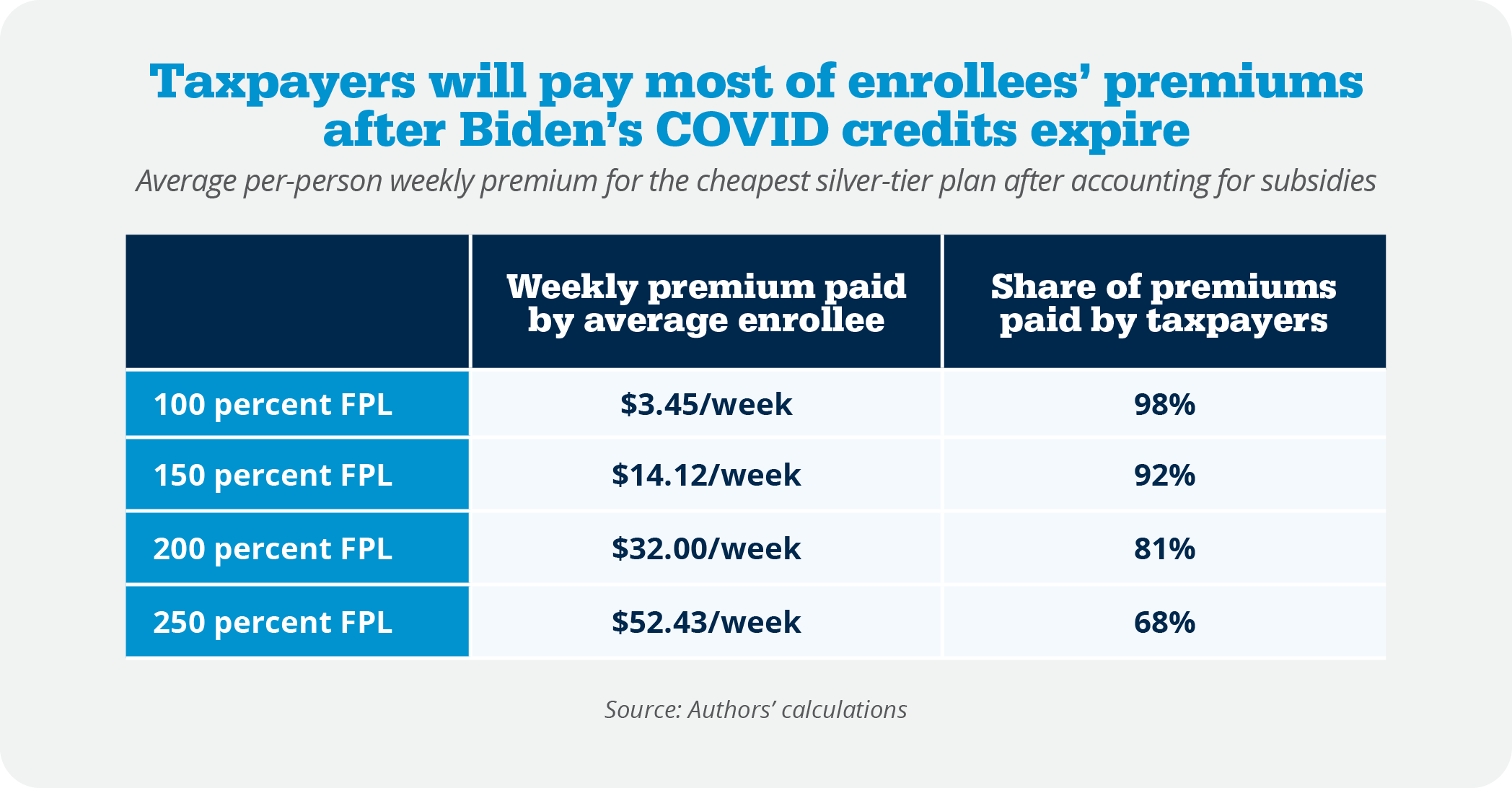

Even as premiums continue to rise because of the program’s underlying flaws, more than 93 percent of enrollees will still be insulated from most of the cost, with the vast majority paying modest monthly amounts while federal taxpayers shoulder roughly 80 percent of the premiums and even higher shares for lower-income enrollees. The table below shows the weekly premiums that enrollees would pay for the lowest-cost silver plans available to them.49 In 2025, 45 percent of exchange enrollees claimed income between 100 and 150 percent of FPL. Those enrollees would pay between $4 and $14 a week for silver plans next year. Another 20 percent of enrollees are between 150 and 200 percent of FPL and would need to pay up to $32 per week. Another 10 percent of enrollees are between 200 and 250 percent of FPL and would have to pay up to $52 a week for coverage.

In high-cost areas, the expanded subsidies deliver very large benefits to affluent households: in one Arizona market, a family of five can receive subsidies well into the six-figure income range and does not lose eligibility until income is around $614,000.50

Insurers Are Big Beneficiaries of the ACA and the Enhanced Subsidies

These enormous ACA subsidies, made even larger by the COVID subsidy boosts, flow straight to insurers. In 2024, more than 83 percent of exchange premium revenue came from the U.S. Treasury.51 Insurers’ business models now revolve around maximizing federal subsidies rather than designing plans that consumers value, and profits surged during the pandemic subsidy expansion not because coverage improved but because federal payments exploded.

Policies to Lower ACA Premiums and Expand Patient Control

In my testimony before the Senate Finance Committee, I discussed nine affordability ideas to address problems with the ACA—either reforms to the program or broader reforms focused on expanding choices for people harmed by the ACA or reforms to enhance competition in the market.52 I list the reforms here but for a discussion, please see my testimony before the Finance Committee.

- Appropriate the ACA’s cost-sharing reduction subsidies to address silver loading

- Enact the Health Savings Account (HSA) option to empower patients, not insurers53

- Make HSAs more flexible and accessible by creating another pathway for plans to be integrated with HSAs

- Limit the inflationary aspect of ACA subsidies by capping the premium used to calculate the subsidies at 125 percent of the average premium

- Expand access to short-term limited-duration health plans

- Expand employers’ ability to form Association Health Plans

- Make individual coverage health reimbursement arrangements more flexible for employers and employees

- Expand price transparency to enable greater market discipline

- Expand the availability of ACA catastrophic plans

During that Senate testimony, I also discussed several other government policies that inflate health care prices and costs, with recommendations for reform. These policies include:

- Medicaid money laundering schemes and state-directed payments,

- Medicare site of service payment differentials,

- the 340B program,

- the limitations in the ACA on physician-owned hospitals,

- the general growth in complexity from federal mandates and regulations,

- certificate of need laws, and

- scope of practice limitations.

Thank you for the opportunity to testify before the committee today, and I look forward to your questions

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.