Shares ofVertex Pharmaceuticals( VRTX 7.79% )were jumping 8.2% as of 12:01 p.m. ET on Wednesday. The nice gain came after the big biotech announced positive results from a phase 2 proof-of-concept study evaluating VX-147 in treating patients with APOL1-mediated focal segmental glomerulosclerosis (FSGS).

FSGS is a kidney disease caused by variants of the APOL1 gene. Individuals with FSGS can require dialysis or kidney transplants. Some eventually die of the disease, which currently has no approved therapies targeting the underlying cause.

Vertex reported that participants in the phase 2 study who were treated with VX-147 had "statistically significant, substantial, and clinically meaningful mean reduction in proteinuria [proteins in the urine] of 47.6%" at 13 weeks after dosing compared to their baseline levels. The company also stated that the experimental drug was well tolerated with no serious adverse events related to it and no treatment discontinuations due to adverse events.

These positive results provided a big boost for Vertex when it was much needed. Prior to today, the biotech stock had fallen nearly 21% year to date. The decline was primarily due to Vertex's disappointing results earlier this year for its alpha-1 antitrypsin deficiency (AATD) program. Investors now have reason to be more confident about Vertex's prospects beyond cystic fibrosis (CF), an indication where the company has achieved tremendous success.

Vertex now plans to advance VX-147 into pivotal development in the first quarter of 2022. The company's clinical studies will target APOL1-mediated kidney disease, including (but not limited to) FSGS.

Arbutus Biopharma Corporation (Nasdaq: ABUS), a clinical-stage biopharmaceutical company primarily focused on discovering, developing and commercializing a broad portfolio of assets with different modes of action to provide a cure for people with chronic hepatitis B virus (cHBV) infection and to treat coronaviruses (including COVID-19), today announced preliminary data from its on-going Phase 1a/1b clinical trial demonstrating that its next generation capsid inhibitor, AB-836, is generally safe and well-tolerated in both healthy subjects and patients with cHBV and provides robust antiviral activity.

Gaston Picchio, Ph.D., Chief Development Officer at Arbutus, commented, “These preliminary results demonstrate that AB-836 is generally safe and well-tolerated in both single- and multiple-doses in healthy subjects and at doses up to 100mg administered once daily for 28 days in cHBV patients. In addition, the mean Day 28 drop in HBV DNA observed to date with a relatively low dose suggests that AB-836 is a very potent inhibitor of HBV replication making it an ideal candidate to potentially completely suppress viral replication. We look forward to continuing to evaluate the safety and efficacy of AB-836 in Part 3 of this trial.”

The Phase 1a/1b clinical trial is designed to evaluate the safety, tolerability, pharmacokinetics and antiviral activity of single and multiple doses of AB-836 in healthy subjects and patients with cHBV. The trial consists of three parts. Part 1 evaluated alternating single doses of AB-836 or placebo ranging from 10mg to 175mg in a fasted or fed state in healthy subjects. Part 2 evaluated multiple ascending doses of 50mg, 100mg or 150mg of AB-836 or placebo once daily for 10 days in healthy volunteers. Part 3, which is still on-going, is currently randomizing HBV DNA positive cHBV patients who are HBeAg positive or negative to receive either 50mg or 100mg of AB-836 or placebo once daily for 28 days.

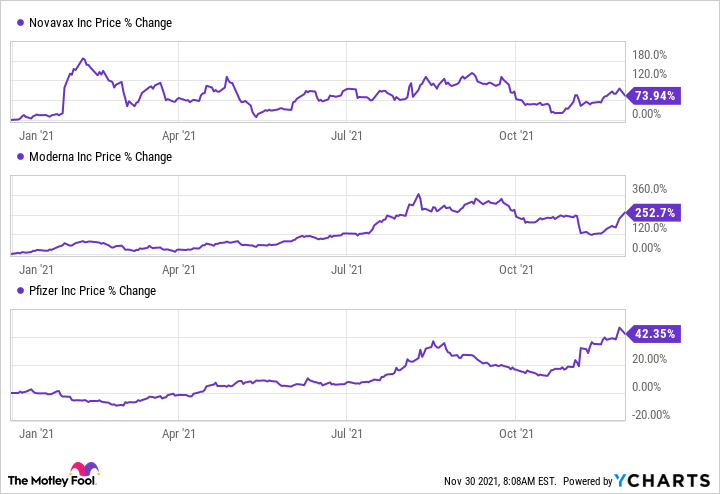

Moderna( MRNA -9.62% )andPfizer( PFE 0.24% )dominate the coronavirus vaccine market. Each has generated quarterly vaccine revenue in the billions. And they expect to report annual vaccine revenue of as much as $18 billion and $36 billion, respectively.Johnson & Johnsonalso sells a coronavirus vaccine. But the company has remained a distant rival since that product's authorization.

But the vaccine market soon may welcome another competitor. And that competitor has a potential vaccine that could carve out a decent share of the market. Now, the question is whether, right now, this latecomer represents a better buy than today's leaders. Let's find out.

So, which player am I talking about? None other thanNovavax( NVAX -7.19% ). The company is far from a stranger to the spotlight. The U.S. awarded the biotech $1.6 billion in funding in the early days of the vaccine race -- and a contract for the delivery of 100 million vaccine doses. Novavax fell behind due to struggles with its manufacturing ramp up. But in recent weeks, the company completed regulatory filings to various countries. And it's even won authorization from Indonesia and the Philippines.

Novavax plans on filing for authorization in the U.S. before the end of the year. A decision could come a few weeks later. But can Novavax still benefit this late in the game?

I think so. And here's why. Novavax's potential product is different from the Moderna and Pfizer vaccines. The candidate isn't an mRNA vaccine. That means it doesn't include mRNA to instruct the body to produce a copy of the coronavirus spike protein -- that's the protein used to infect. Instead, Novavax's candidate falls into the category of protein subunit vaccines. It includes a genetically engineered spike protein in nanoparticle form along with an adjuvant to boost immune response.

Some healthcare providers and individuals hesitate to go for a new technology like mRNA. And this is where Novavax can gain market share. Subunit vaccines already are on the market -- an example is the hepatitis B vaccine. This is a long-proven technology. So those who are hesitant about going for a coronavirus jab may more easily opt for Novavax.

The temperature difference

Also, Novavax's candidate is stable at refrigerator temperatures. Moderna and Pfizer vaccines can only be stored at those levels for a month. After that, they require freezer temperatures.

Novavax also may get a lift from the U.S. Food and Drug Administration's authorization of vaccine "mixing and matching." That means anyone who has received a primary series of one authorized vaccine brand may choose the same brand or another when it's time for a booster.

And finally, Novavax won't be left behind when it comes to dealing with variants of concern. A Novavax spokesperson told The Hill that the company has begun development of a candidate targeting the omicron variant. Health officials first detected omicron in South Africa early last month. Since, it's spread to other areas including Europe and North America.

Now, let's look at Novavax's stock price. It climbed more than 12% last month. From here, Wall Street predicts the stock could increase 30%, according to the average 12-month price forecast.

Year-to-date, Moderna has soared past Novavax. Pfizer remains the laggard. (That's almost expected. Pharmaceutical companies aren't as sensitive to vaccine news as their biotech rivals. That's because they depend on the sales of many products -- so they aren't as reliant on just one.)

Novavax is particularly interesting at today's level. That's because several catalysts lie ahead: regulatory authorization in various markets including the U.S., vaccine rollout, and real-world data once a product is on the market. Any positive data on how Novavax fares against the omicron variant also could offer a lift.

I'm positive on Moderna and Pfizer over the long term. But they've already been through the vaccine authorization and launch stage -- and reaped the rewards of share performance. In the coming months, it may be Novavax's turn. That's why this biotech stock may represent a better buy right now.