Unfair to Americans with Employer-Based Insurance, Punish Work, and Incentivize Employers to Drop Coverage

Key Takeaways

- The ACA subsidies create major financial inequities for low- and middle-income Americans, penalizing those who receive health insurance through their employers.

- The ACA subsidies shift the tax code from rewarding work and employer coverage to subsidizing early retirement and non-work while discouraging upward mobility.

- The ACA subsidies create large incentives for employers—particularly those with a high concentration of low- and middle-income employees—to stop offering coverage:

- Coverage offerings have already dropped by nearly one-third at small firms.

- State and local governments have dropped retiree health plans by moving retirees into the exchanges.

- If the COVID credits are made permanent, more employers will drop coverage for employees, and more state and local governments will offload retiree health care expenses onto federal taxpayers.

- The COVID credits exacerbate all the underlying problems with the original subsidies.

Background on ACA and Employer Coverage

Most Americans who are not enrolled in Medicare or Medicaid receive health insurance through their employers or those of their spouses or parents. These workers pay for that coverage. Although commonly called the employer’s share of the premium, that amount simply represents wages the employee forgoes. Because premiums are excluded from income and payroll taxes, employees face a lower tax burden than if the same compensation were paid in wages. This is an untaxed earned benefit.

By contrast, the vast majority of people who receive coverage on the exchanges established under the Affordable Care Act (ACA) bear little, if any, of the cost. In effect, the ACA exchanges function as welfare—an unearned benefit provided by federal taxpayers.

The ACA created premium subsidies that limit the amount of income households must pay for health insurance on the ACA exchanges. The subsidies are structured to be much more favorable for Americans nearing retirement than for younger Americans. In 2021 and 2022, without any Republican support, Democrats expanded those subsidies—the so-called Biden COVID credits—and lifted the cap that had originally limited ACA subsidies to households earning less than four times the federal poverty level (FPL). Congressional Democrats set the COVID credits to expire at the end of 2025. As a result of that subsidy expansion, in 2024, federal taxpayers covered 83 percent of the revenue insurers collected for exchange plans and 87 percent in states using the federal exchange. 1 Moreover, roughly half of all enrollees were enrolled in fully subsidized plans that did not require enrollees to pay any portion of the premium.

As a result, two workers creating equal value for an employer receive dramatically different after-tax compensation depending on whether their employer offers coverage. If one worker receives employer coverage and earns a low or middle income, he is worse off, because part of his compensation must go toward that coverage. If he does not receive employer coverage, he generally qualifies for large premium subsidies—particularly after the Biden pandemic-era subsidy expansion—and will in most cases be much better off economically. Thus, the worker without employer coverage ends up with higher wages and greater federal health insurance benefits.

The authors of the ACA needed to build on employer-based health benefits—a characteristic of the American workplace since around World War II—for political and policy reasons. In an attempt to expand coverage with the lowest possible budgetary cost, the ACA included an employer mandate and barred people with offers of “affordable” employer plans from premium subsidy eligibility. Under the mandate, employers with 50 or more workers have to offer “affordable” coverage to at least 95 percent of their full-time employees (those who work for at least 30 hours a week) or suffer significant fines.2 The ACA defines <em>affordable</em> as no more than 9.5 percent of an employee’s household income.3

Of note, the Biden administration expanded eligibility for subsidies in the so-called “family glitch” fix by—with questionable legal authority—redefining affordability based on the cost of family coverage, not single coverage. By doing this, employers have less incentive to offer “affordable” dependent coverage, which means that more dependents will lose employer coverage and be shifted to the exchanges unless the Trump administration returns to the policy that prevailed in the Obama administration and first Trump administration.

The employer mandate penalty was necessary because the ACA’s subsidy design discriminates against low- and middle-income workers offered employer-provided health benefits. Without government coercion to continue offering health benefits under threat of severe penalty, many employers would have stopped offering coverage, leading their workers to enroll in exchange plans at significant additional cost to taxpayers.

Despite the ACA’s employer mandate, some anticipated a reduction in employer-based insurance offerings because of the exchanges and corresponding subsidies. The Congressional Budget Office (CBO) forecast that about 3 million fewer people would have employer-based plans in 2019, five years after the ACA exchanges launched—a reduction of about 2 percent.4 But some surveys of employers forecast a different result. A McKinsey and Company survey in 2011 attracted the most attention, finding that 30 percent of employers would “definitely” or “probably” stop offering health coverage under the new law.5 Among employers with a high awareness of the reform, the proportion choosing to drop coverage increased to 50 percent.

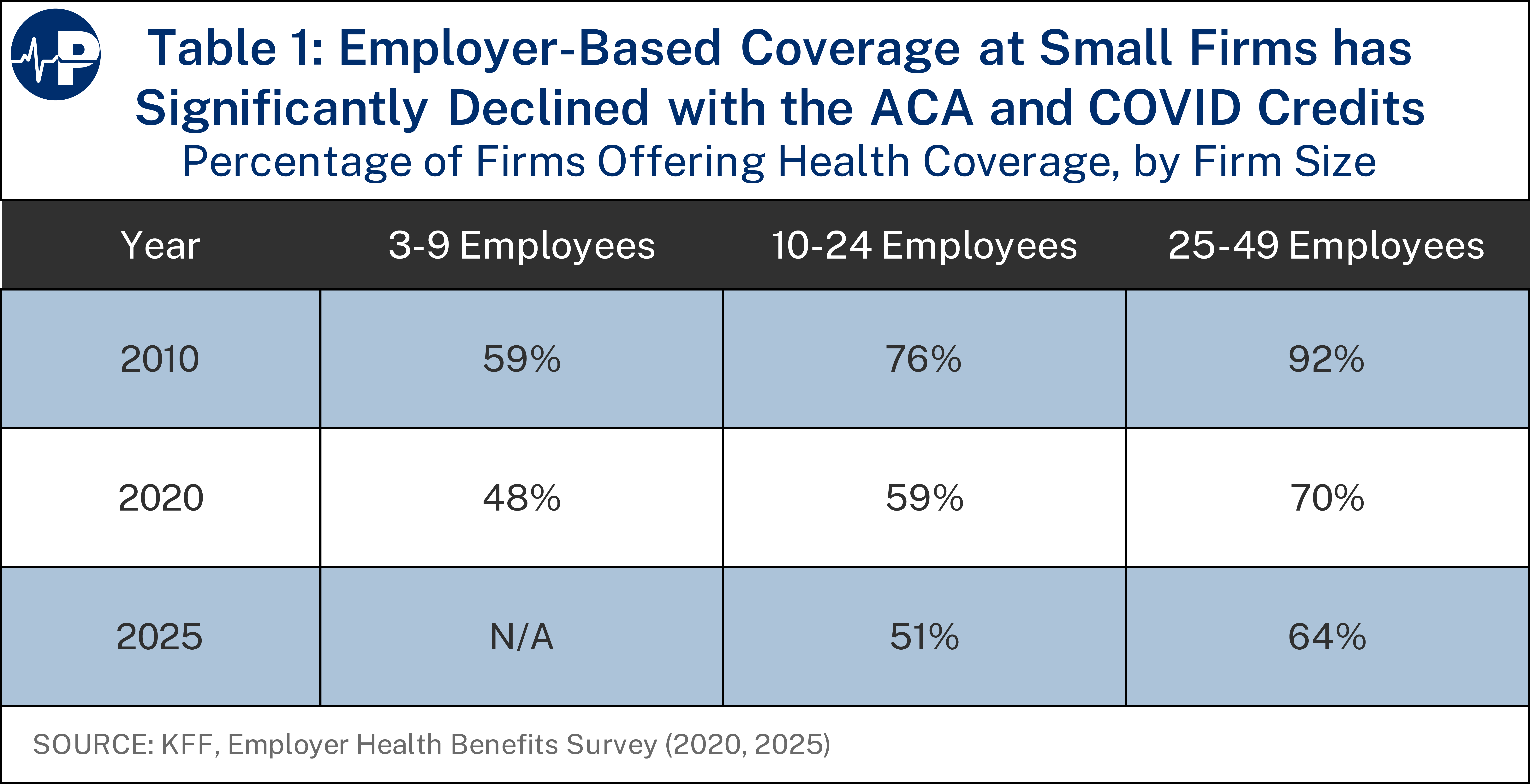

Although a large drop in employer-based coverage has not occurred, coverage has declined significantly at small firms. Exchange coverage was widely viewed as unattractive for employees, and few large employers altered their offerings because of the law. Because small businesses are exempt from the employer mandate, some dropped coverage after the ACA passed. As shown in Table 1, in 2010, 76 percent of firms with 10-24 employees and 92 percent of firms with 25-49 employees offered health insurance.6 By 2020 (the last year before the COVID credits), those numbers had dropped to 59 percent and 70 percent.7 By 2025, those numbers had fallen further—to 51 percent and 64 percent, respectively.8 There was also attrition in offerings at firms with three to nine employees from 59 percent to 48 percent from 2010 to 2020 (although this percentage was not reported for 2025). Small businesses are also more likely to drop coverage because administrative costs per employee for managing health benefits are higher at small firms than large ones.9

Although there has been a significant drop in small businesses offering coverage, the overall attrition of employer-sponsored insurance has been much less than expected, as almost all large employers (those with at least 50 full-time employees) have continued to offer coverage. For this reason, revenue collected from the employer mandate has been only about 1 percent of what CBO originally expected.10

This policy brief will discuss three key problems from the excessive subsidization of the ACA exchanges:

- Large discrimination against people with employer-provided coverage

- Large effective taxes on work, particularly for the most productive employees

- Large incentives for employers to drop coverage

Discriminating Against People with Employer-Provided Health Coverage

The results are perverse: people who keep working and receive coverage through their employer lose out, while those who don’t—such as early retirees—receive the biggest subsidies. Consider the case highlighted by U.S. Senator Amy Klobuchar: a couple in their 50s, recently retired from public employment, earning nearly $140,000 per year in combined pension income.11 Under the COVID credits, they received a $15,000 premium subsidy in 2025—even though they are in the top income decile.12 Before 2021, this couple would have received no premium tax credit (PTC) at all. The expanded subsidies transformed the ACA into a program that subsidizes not only low-income workers but also wealthy early retirees who can now leave the labor force—and the connection to employer-sponsored health coverage—years before becoming eligible for Medicare. In 2023, only about 6.7 percent of enrollees with employer-coverage were 60-64 compared to about 13.0 percent of enrollees in the exchanges of that age.13

This example vividly captures how the ACA’s subsidy design discriminates against working families. While full-time employees must pay their share of employer-based coverage out of earnings, high-income retirees with guaranteed pensions can receive tens of thousands of dollars in federal health insurance subsidies. The inequity has widened since the pandemic-era expansion, and if Congress makes the COVID credits permanent, similar couples across the country would gain another incentive to retire early, while younger workers with employer-based coverage would continue to shoulder the costs through higher taxes and lower wages.

The status quo is extremely unfair to workers who receive employer-based health benefits, especially those who earn lower wages. While less severe at higher incomes, the discrimination persists well into six-figure salaries, especially under the COVID credits.14 The figures below demonstrate the underlying unfairness to workers with employer-based coverage created by the ACA’s subsidy regime and how the unfairness would significantly increase if Congress maintains the COVID credits instead of allowing them to sunset at the end of this year (and three years after the end of the pandemic emergency for which they were instituted).

For this paper, we make a simplifying assumption that $1 of employer-based coverage is equivalent to $1 of ACA coverage. However, there is strong evidence that ACA coverage is of lower quality than employer-based insurance. A 2023 survey found 20 percent of ACA enrollees reported a doctor or hospital they needed was not covered by their plan, whereas only 13 percent of enrollees in employer-based health plans faced this problem. This rose to 34 percent of ACA enrollees in only fair or poor health, versus only 16 percent of enrollees in work-based plans. Further, twice as many ACA enrollees skip or delay care because they cannot find a doctor who accepts their plan than those with employer-based benefits do.15

Beyond the numbers, this difference in quality makes the perverse financial incentives to drop employer-based coverage for ACA plans even more distressing. Taxpayers are subsidizing working people and their families to move from higher quality to lower quality coverage. These disparities are not abstract. They translate into thousands of dollars in after-tax compensation differences for two workers doing the same job.

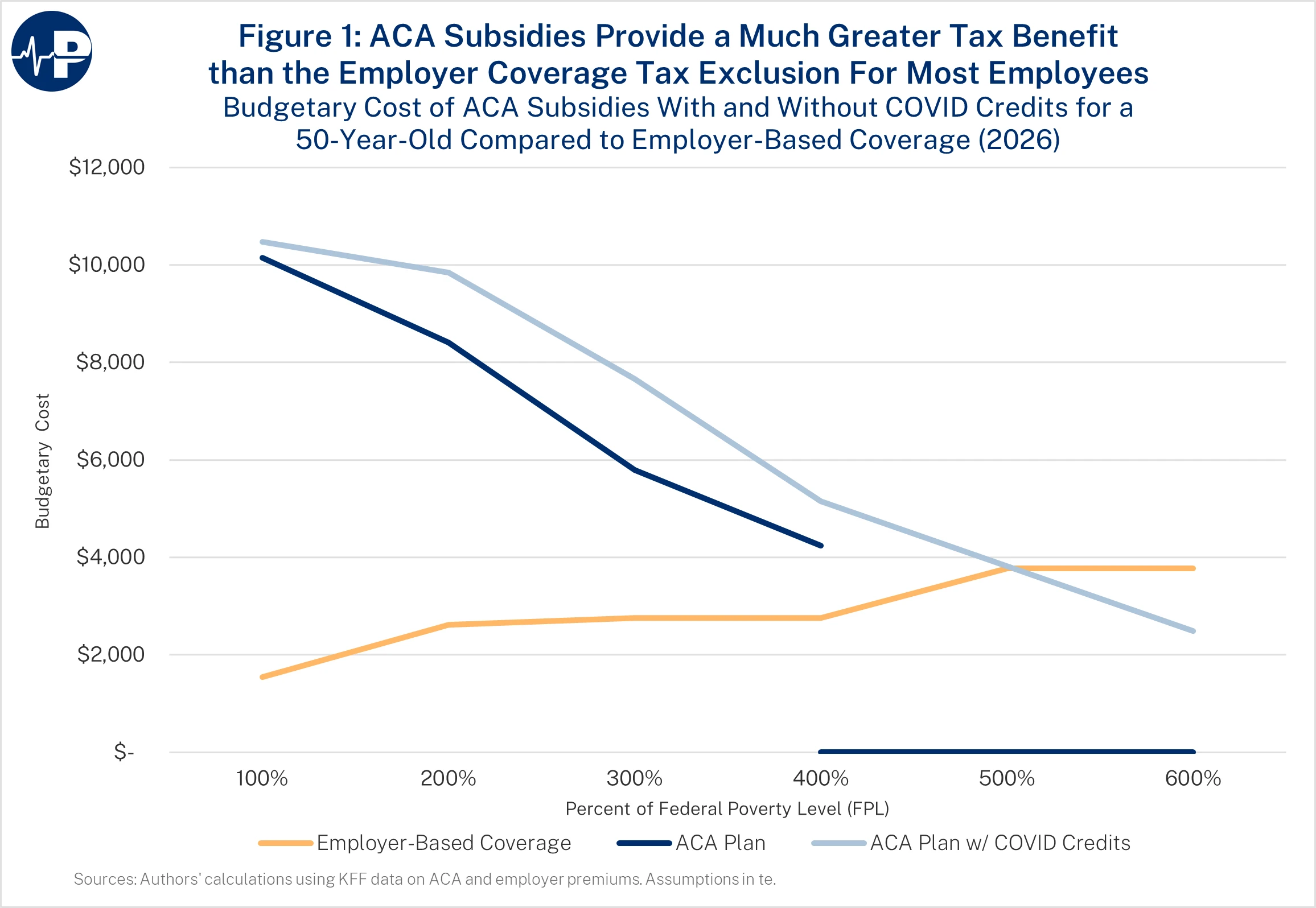

Figure 1 shows the size of the government health insurance benefit for a 50-year-old with single coverage at different income levels in 2026 for three scenarios: (1) employer-based coverage (orange line), (2) the original ACA subsidies (navy blue line) and (3) the original subsidies plus the COVID credits (light blue line). The government benefit in scenario 1 is from the exclusion of premiums from income and payroll taxes. The benefit in scenarios 2 and 3 is from the government subsidy for an exchange plan. The figure shows that lower- and lower-middle-income enrollees obtain much greater benefit if they do not receive coverage at work and instead enroll in exchange coverage. In other words, workers face a large penalty if they receive health insurance through their employers rather than through the exchanges.

Consider a worker earning $46,950 (300 percent FPL). With exchange coverage, he would receive a $5,797 PTC under current law—or $7,656 with the COVID credits. If a worker with the same job and salary has employer-based coverage, his tax benefit from the premium exclusion is $2,760. The difference—$3,037 under current law and $4,896 with the COVID credits—is effectively a penalty on the worker with employer-based insurance. Moreover, it is also a penalty on work. The worker with employer coverage earns his health benefit but is not taxed on that portion of his compensation. The person with employer-based health insurance does not earn the tax credit.

For a 50-year-old, the disadvantage of receiving employer-based coverage persists up to an income of 400 percent FPL under the original PTCs (because those above 400 percent FPL are ineligible for the original subsidies) and up to 500 percent under the Biden COVID credits (because the subsidy phaseout extends further up the income scale). This might explain why so few people at higher incomes who are working are enrolled in exchanges: They do not suffer the discrimination that lower-earning workers do and benefit from having jobs that offer health insurance. In 2025, fewer than 7 percent of exchange enrollees reported incomes above 400 percent FPL.16

Figure 2 demonstrates the differential benefit between the PTCs and employer coverage for a younger worker. The effects are not as pronounced, because younger workers qualify for lower PTCs as the plan premium is lower. Nevertheless, the effects can still be significant, because a 21-year-old is likely earning a much lower wage than her middle-aged colleague. If she earns $31,300 (200 percent FPL), her original PTC would be $3,798 and her PTC with the COVID credit would be $5,238, whereas the tax preference for an employer-based plan would be only $2,620. The difference between the PTC and her tax benefit for an employer-based plan, $1,178, is the increased tax burden she suffers if she chooses a job with health benefits. That burden would increase over two and a half times to $2,618 if Congress extends the COVID credits.

Figure 3 illustrates the effect for a young family with 35-year-old parents and two children, ages 7 and 10 years. If the family’s income is $64,300 (200 percent FPL), they will receive a PTC under the original ACA subsidies of $19,059. The tax break for an employer-based health plan for the family would be only $5,904. The difference is a $13,155 net government benefit for not receiving coverage at work. However, if Congress extends the Biden COVID credits, the family’s credit would be $22,017, and the net government penalty for receiving coverage at work would increase to $16,113.

Beyond discriminating among workers, the ACA subsidy structure also distorts how people make decisions about work and income.

ACA Subsidies Punish Work

By tying the government benefit to the absence of an employer-based health insurance plan, the government discourages people from working for employers who offer health coverage, which is most employers and virtually all large employers. This design distorts labor market decisions, encouraging people to opt for jobs or work arrangements that do not provide coverage simply to qualify for larger subsidies. Unlike employer-based benefits, which employers use to attract workers and have greater tax benefits when income increases, the ACA tax credits punish enrollees who increase their income, because earning higher income cuts their subsidies. By contrast, there is no disincentive to a worker with employer coverage who seeks to increase his pay by becoming more productive or working more. Because premiums are excluded from taxable income, the value of employer-provided health benefits rises as workers move into higher tax brackets. While there are drawbacks with employer coverage and the tax exclusion for premium payments,17 it does not punish workers who want to increase their earnings.

These inequities extend beyond fairness—they alter how people choose when and how much to work. The ACA subsidies present a disincentive for work and income growth as each additional dollar of income modestly reduces the subsidy amount. On average, the subsidy phaseout creates an implicit marginal tax rate of about 15 percent—so for every $100 in extra earnings, an enrollee loses roughly $15 in PTCs.18 As CBO projected in 2015, the ACA’s subsidy phasedowns would reduce the full-time workforce by roughly 2 million workers by 2025—underscoring how work-disincentive effects from the law have long been expected.19

Figure 4 illustrates this effect for a single 64-year-old—generally the oldest possible exchange enrollee. Under the ACA, he receives no PTC if his income exceeds 400 percent FPL ($62,600). However, if his income is up to that threshold, he would receive a PTC of $11,357—$8,597 more than his tax benefit if he received employer-based coverage. With the COVID credits, he would receive a total subsidy of $12,271, increasing the benefit of ACA coverage over employer coverage to $9,511. However, because the COVID credits extend beyond 400 percent FPL, the discrimination in favor of people who do not receive coverage at work persists even at very high income levels. We cut the figure at 600 percent FPL ($93,900), but the gap persists well into six-figure incomes.

For households like the early retirement couple cited above, the expanded subsidies also lower the effective cost of leaving the labor force. By guaranteeing heavily subsidized coverage to households with high pension income, the Biden COVID credits give affluent older Americans yet another incentive to retire early. The policy thus reduces workforce participation among the very people whose experience and productivity drive the economy while forcing taxpayers to finance their coverage.

Crowd-out of Employer Plans, and Rising Taxpayer Costs

The same subsidy design that discourages work also pressures small employers to drop coverage. When far larger government benefits are available for exchange plans than the tax exclusion for employer-based insurance, the financial calculus for firms—especially those with lower-wage employees—tilts toward not offering company health plans. Firms can increase worker well-being by raising wages and having workers qualify for premium subsidies on the exchanges. As more workers shift from employer coverage to subsidized exchanges, taxpayer costs rise sharply.

The worst discrimination caused by the ACA and the COVID credits is on Americans who receive employer plans and have modest incomes. Because of the fines on employers who fail to offer “affordable” health benefits, people who work at firms with at least 50 full-time employees are effectively unable to avoid this punitive tax treatment. Extending the COVID credits would reduce employer-based coverage by roughly 4 million people according to CBO, and it would impose a substantial deadweight loss on economic activity.20

However, employer plans are facing extreme cost pressure now, including the demand from employees to broadly cover GLP-1s. If the expanded COVID credits are made permanent, most employees would qualify for subsidies. Most small employers, particularly those with low- or middle-income workers, would have enormous incentives not to offer insurance. And some large employers, again those with low- or middle-income workers, would also have incentives to drop coverage. To the extent this happens, the growing cost of the ACA on federal taxpayers will escalate.

In addition to crowding out employer plans, <em>The Wall Street Journal’s </em>Allysia Finley recently highlighted that the ACA and its subsidies led many Democratic-dominated cities, such as Chicago and Detroit, to offload public sector retiree health care costs.21 These cities moved those retirees into the ACA exchanges, eliminating unfunded retiree health care liability. Finley correctly argues that the COVID credits make this dumping of public sector retirees’ health care obligations into the exchanges even more likely as few governments have set aside money to pay their retirees’ future health care costs. The COVID credits would make wealthy early retirees eligible for large taxpayer-financed subsidies for their health care, adding to the incentive for state and local governments to move those retirees into the exchanges. Finley also highlights the risk that this would make the ACA risk pool older and sicker, pushing up premiums and exacerbating structural problems in the program.

Conclusion

The ACA, compounded by the ill-conceived COVID credits, has produced a tax and subsidy structure that punishes workers with employer-based coverage. The underlying ACA subsidies, compounded by the COVID credits, penalize employment, reward early retirement, and leave taxpayers footing a rapidly expanding bill. Allowing the temporary COVID credits to expire is a critical step toward restoring fairness, strengthening work incentives, and improving fiscal discipline.

Brian Blase, Ph.D., is the President of Paragon Health Institute. Brian was Special Assistant to the President for Economic Policy at the White House’s National Economic Council (NEC) from 2017-2019, where he coordinated the development and execution of numerous health policies and advised the President, NEC director, and senior officials. After leaving the White House, Brian founded Blase Policy Strategies and serves as its CEO.

John R. Graham is a Visiting Fellow who contributes nearly three decades of health policy expertise to research across all of Paragon’s initiatives. He worked on Capitol Hill from 2021 to 2024 as a Professional Staff Member on the Senate Special Committee on Aging and the House Committee on Ways & Means. From 2018 to 2021, he served as the U.S. Department of Health & Human Services (HHS) Regional Director for Region 10 (Washington State, Oregon, Idaho, and Alaska), where he managed relationships with state governments and the private sector. In 2017-2018, John was the HHS Acting Assistant Secretary for Planning & Evaluation.