A superficial take of today's jobs report would note that both jobs and earnings "blew past expectations, flying in the face of Fed rate hikes", and while that is accurate at the headline level, it couldn't be further from the truth if one actually digs a little deeper in today's jobs numbers.

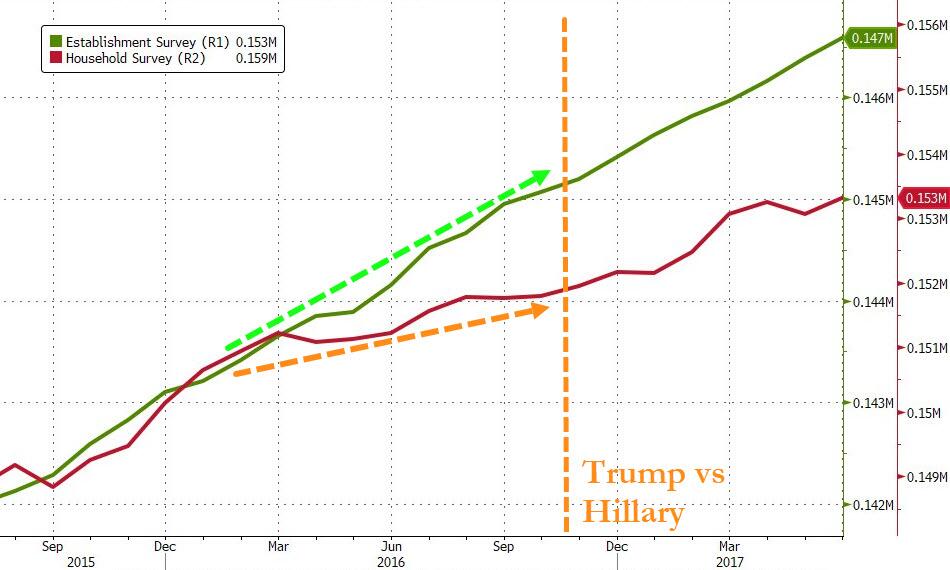

Recall that back in August, September, and October we showed that a stark divergence had opened between the Household and Establishment surveys that comprise the monthly jobs report, and since March the former has been stagnant while the latter has been rising every single month. In addition to that, full-time jobs were plunging while part-time jobs were surging and the number of multiple-jobholders soared.

Fast forward to today when the inconsistencies not only continue to grow, but have become downright grotesque.

Consider the following: the closely followed Establishment survey came in above expectations at 263K, above the 200K expected - a record 7th consecutive beat vs expectations - and down modestly from last month's upward revised 284K...

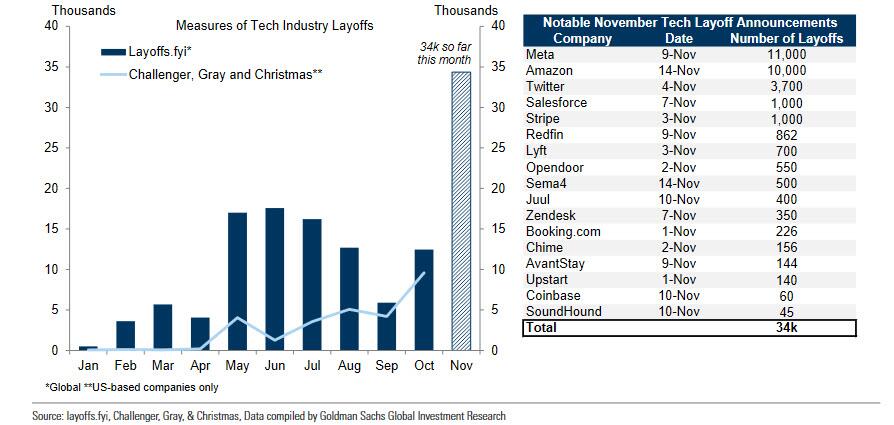

... numbers which confirm that at a time when virtually every major tech company is announcing mass layoffs...

... the BLS has a single, laser-focused political agenda - not to spoil the political climate at a time when Democrats just lost control of the House as somehow both construction (+20K) and manufacturing (+14K) added jobs according to the BLS, when even ADP now reports that these two sectors combined shed more than 100,000 workers in November.

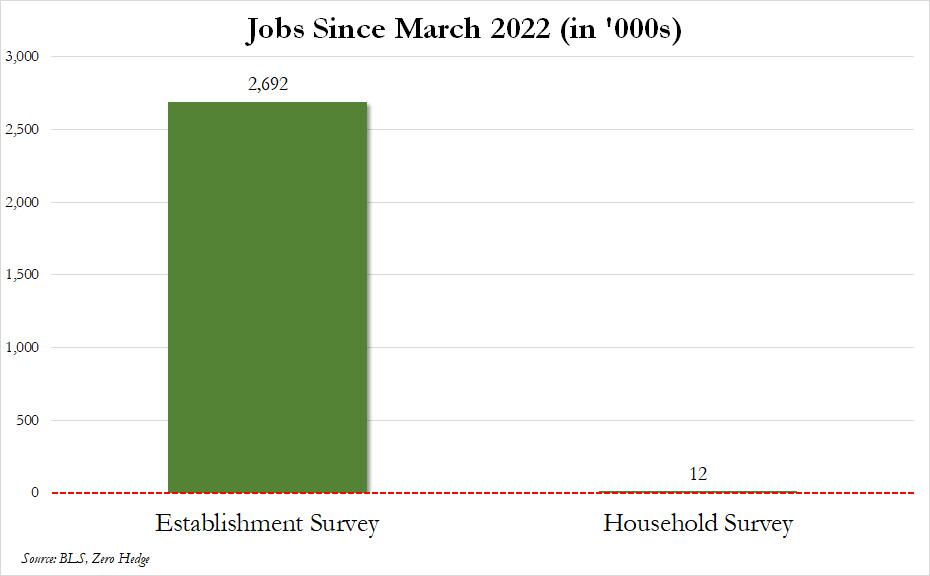

Alas, there is only so much the Department of Labor can hide under the rug because when looking at the abovementioned gap between the Household and Establishment surveys which we have been pounding the table on since the summer, it just blew out by a whopping 401K as a result of the 263K increase in the number of nonfarm payrolls (tracked by the Household survey) offset by a perplexing plunge in the number of people actually employed which tumbled by 138K (tracked by Household survey). Furthermore, as shown in the next chart, since March the number of employed workers has declined on 4 of the past 8 months, while the much more gamed nonfarm payrolls (goalseeked by the Establishment survey) have been up every single month.

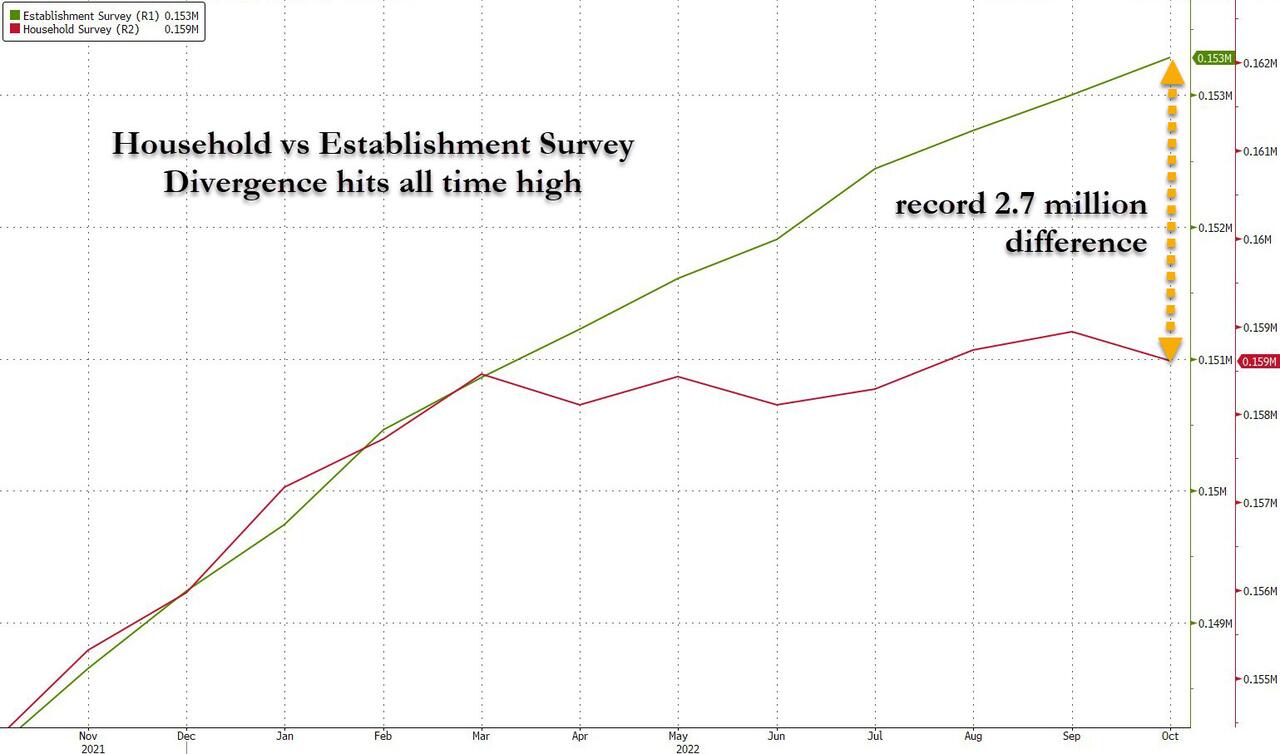

What is even more perplexing, is that despite the continued rise in nonfarm payrolls, the Household survey continues to telegraph growing weakness, and as of Nov 30, the gap that opened in March has since grown to a whopping 2.7 million "workers" which may or may not exist anywhere besides the spreadsheet model of some BLS (or is that BLM) political activist. In fact, one look at the chart below confirms all one needs to know about BLS "data integrity."

Showing this another way, there were 158.458 million employed workers in March 2022... and 158.470 million in November 2022 an increase of just 12,000 over 8 months, a period in which the number of payrolls (which as a reminder is the number the market follows) reportedly increased by 2.7 million!

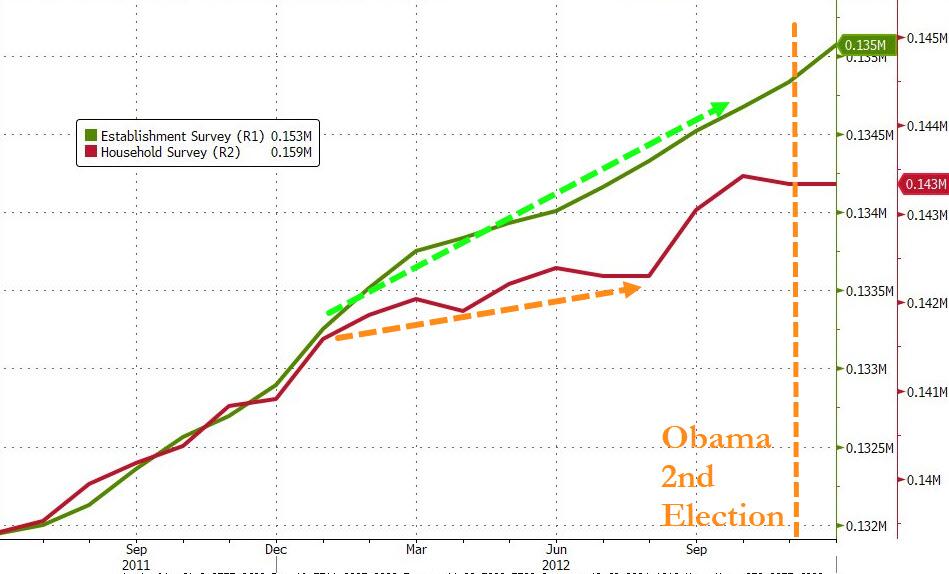

As an aside, it appears this is not the first time the "apolitical" Bureau of Labor Statistics has pulled such a bizarre divergence off: it happened right before Obama's reelection:

And then again: right before Hillary's "100% guaranteed election (because one wouldn't want a soft economy to adversely impact her re-election odds).

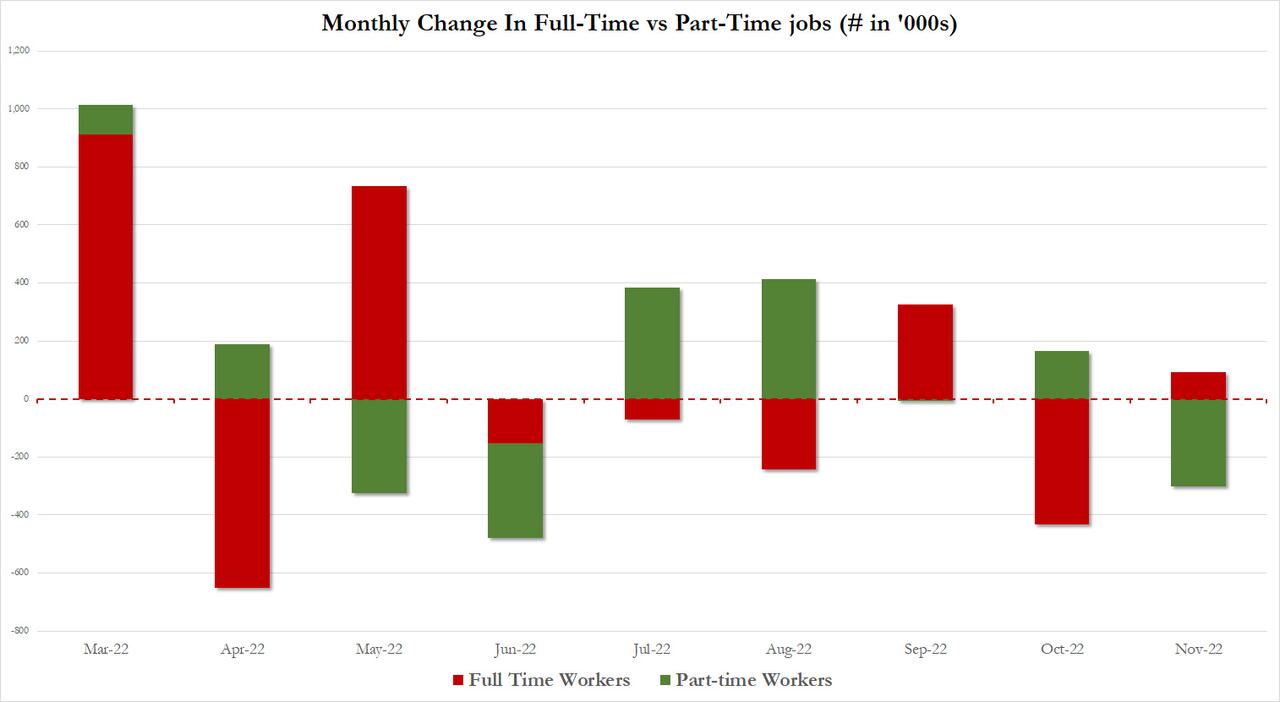

It gets better: digging in even deeper into the far more accurate and nuanced Household Survey, we find that the November drop in Employment was the result of a plunge in part-time workers, more than offsetting the modest increase in part-time workers which had declined in 3 of the past 4 months heading into November.

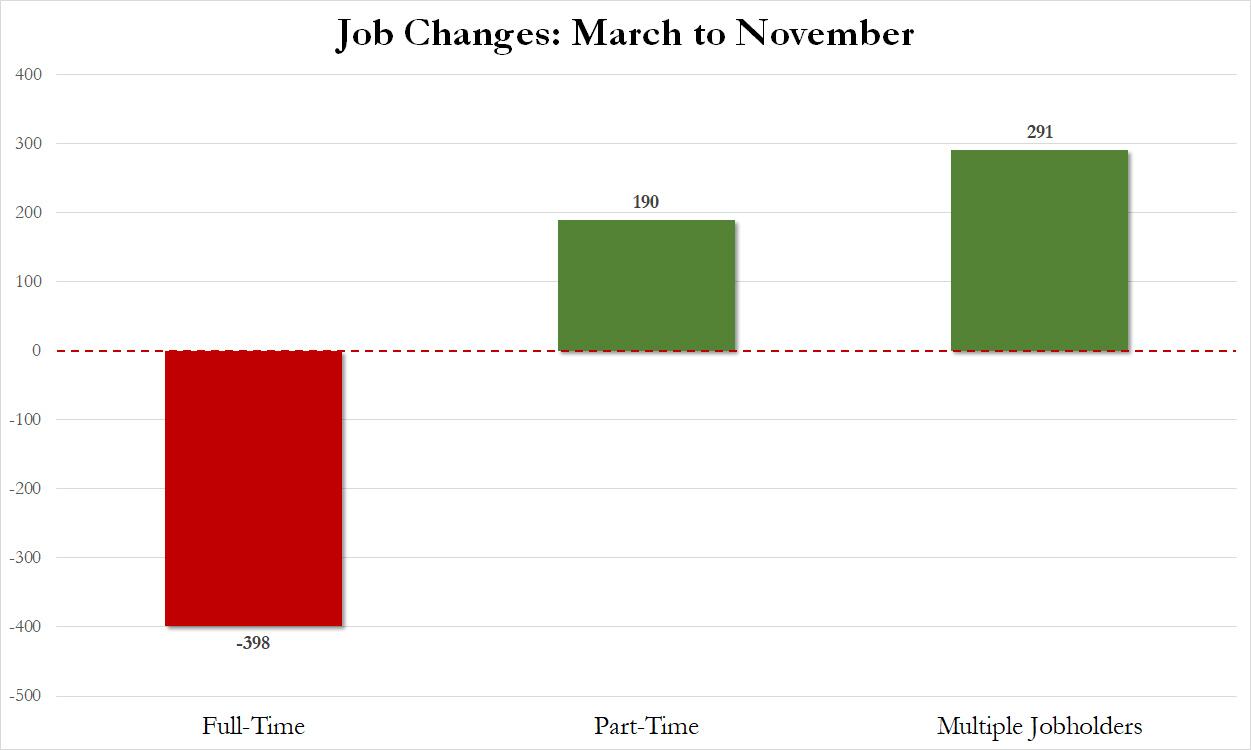

Further to this point, as shown below, since March, the US has lost 398K full-time employees offset by amodest gain of 190K part-time employees, while a whopping 291k workers were forced to get more than one job over the same period.

And while none of the above is really new - we have documented the record divergence between payrolls and employment for half a year now - there were two new developments: first, to facilitate its rigging of the data, the BLS has resorted to the oldest trick in the book, boosting the core goal-seek factor, the business "birth death" adjustments, which in October hit a record high 455K, and although it has since dipped to 14K in November, the trend in speculative BLS assumptions about the viability of the US economy (more businesses are created than are shut down only when there is economic solid growth) is clearly visible in the chart below.

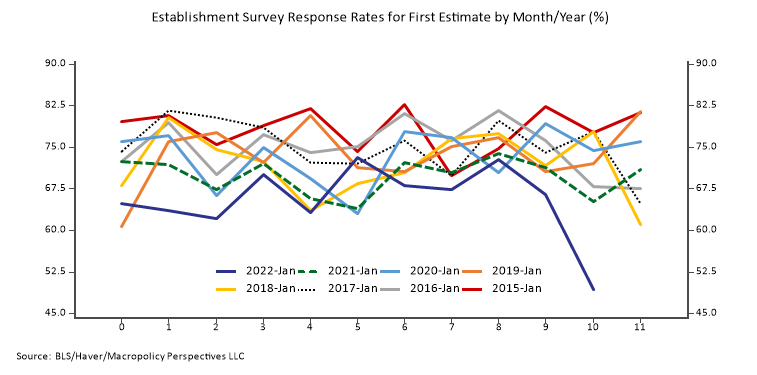

Another point: it appears that the BLS is now aggressively estimating the so-called hard data. As Goldman's Jan Hatzius observed, the 49% Establishment survey response rate was much lower than the 70-75% rate typical in November. The chart below shows just how much of an outlier the Nov 2022 payrolls report: it confirms that roughly a third of the report was not based on reality at all but on aggressive excel modeling and estimates.

One final point: a former Fed staffer Julia Coronado points out, we have reached the absurd part of the business cycle when average hours are declining in certain sectors even as hourly earnings are rising, prompting her to wonder if we are not in fact seeing a spike in hourly income courtesy of lump-sump severance payments.

So what's going on here?

The simple answer: as shocking as this may sound, there has been no change in the number of people actually employed in the past 8 months, but due to deterioration in the economy, more people are losing their higher-paying, full-time jobs, and switching into much lower- paying, benefits-free part-time jobs, which also forces many to work more than one job, a rotation which picked up in earnest some time in March and which has only been captured by the Household survey. Meanwhile the Establishment survey plows on ahead with its politically-motivated approximations, seasonal adjustments, and other labor market goalseeking meant to make the Biden admin look good and provide the Fed with ammo to keep rates high (thus forcing even more real layoffs, which unfortunately the BLS is incapable of capturing due to political reasons).

And since the Establishment survey is far slower to pick up on the nuances in employment composition, while the Household Survey has gone nowhere since March, the BLS data engineers have been busy goalseeking the Establishment Survey (with the occasional nudge from the White House especially now that the Biden admin needs something to hang its hat on after the GOP recaptured the House) to make it appear as if the economy is growing strongly, when in reality all they are doing is applying the same erroneous seasonal adjustment factor that gave such a wrong perspective of the labor market in the aftermath of the covid pandemic (until it was all adjusted away a year ago). In other words, while the labor market is already cracking, it will take the BLS several months of veering away from reality before the government bureaucrats accept and admit what is truly taking place.

As an aside, here we admit we were wrong: back in August we said that "we expect that "realization" to take place just after the midterms, because the last thing the Biden administration can afford is admit the labor market is crashing in addition to the continued surge in inflation." Little did we know just how stubborn and intent the White House is to stick to the broken narrative that all is well in the US.

Or, putting it otherwise as BofA's Michael Hartnett did earlier today (and as we will discuss in a subsequent post) - "unemployment in ’23 will be as shocking to Main St consumer sentiment as inflation in ’22."

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.