Incyte Corporation (NASDAQ:INCY) presented its Second Quarter 2025 Financial and Corporate Update on July 29, 2025, revealing strong financial performance across its product portfolio. The biopharmaceutical company’s stock responded positively to the results, with premarket trading showing a 4.76% increase to $73.50.

The company’s presentation, led by CEO Bill Meury, highlighted continued growth momentum across its key products, with total revenues reaching $1.22 billion, representing a 16% year-over-year increase. This performance builds on the strong start to 2025 reported in Q1, when the company beat analyst expectations with EPS of $1.16 against a forecasted $1.04.

Quarterly Performance Highlights

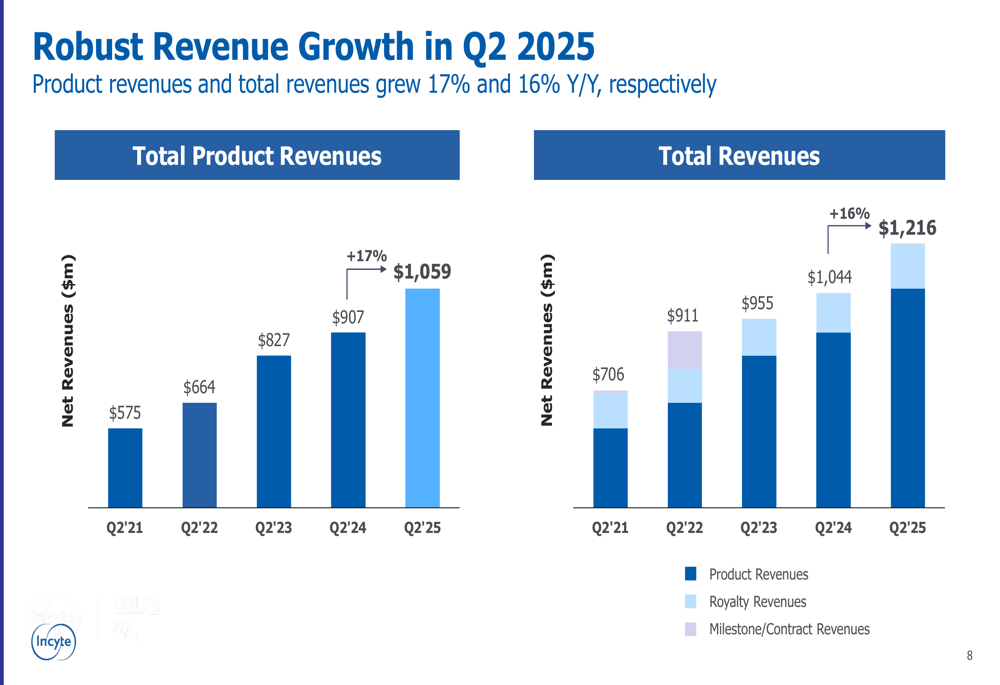

Incyte reported robust revenue growth in the second quarter of 2025, with total product revenues increasing 17% year-over-year to $1.06 billion. Total revenues, including royalties, grew 16% to $1.22 billion compared to Q2 2024.

As shown in the following chart of quarterly revenue growth:

The company’s financial performance has shown consistent growth over the past five years, with total product revenues nearly doubling from $575 million in Q2 2021 to $1.06 billion in Q2 2025.

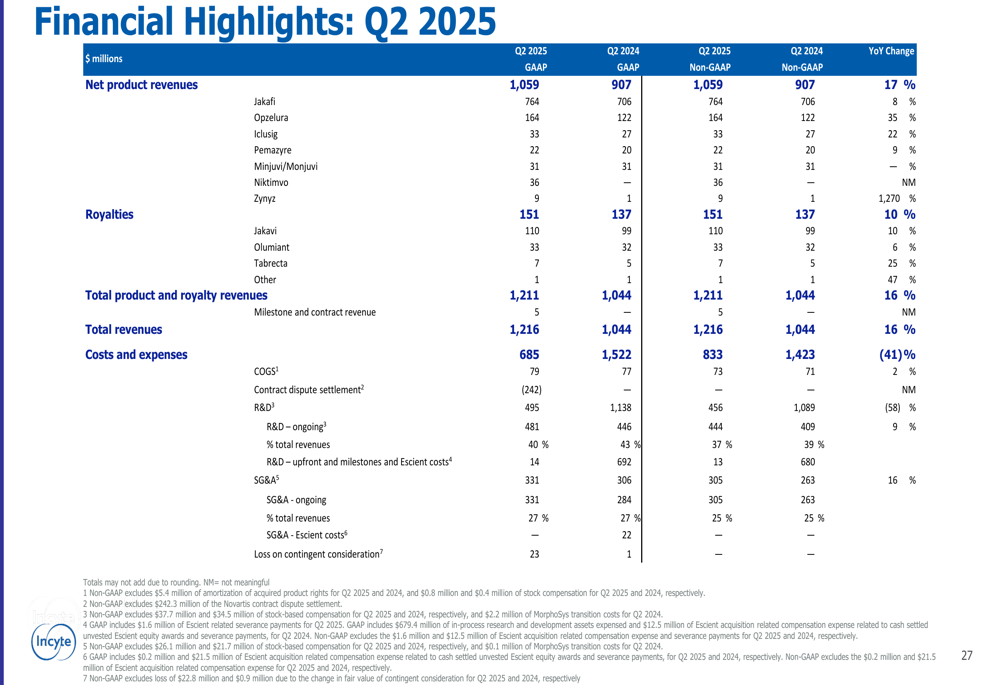

On the expense side, Incyte demonstrated disciplined cost management with R&D expenses decreasing by 57% year-over-year to $495 million in Q2 2025. SG&A expenses increased by 8% to $331 million, reflecting investments in commercial capabilities to support product launches and growth.

The following financial highlights provide a comprehensive view of the company’s Q2 2025 performance:

Product Portfolio Performance

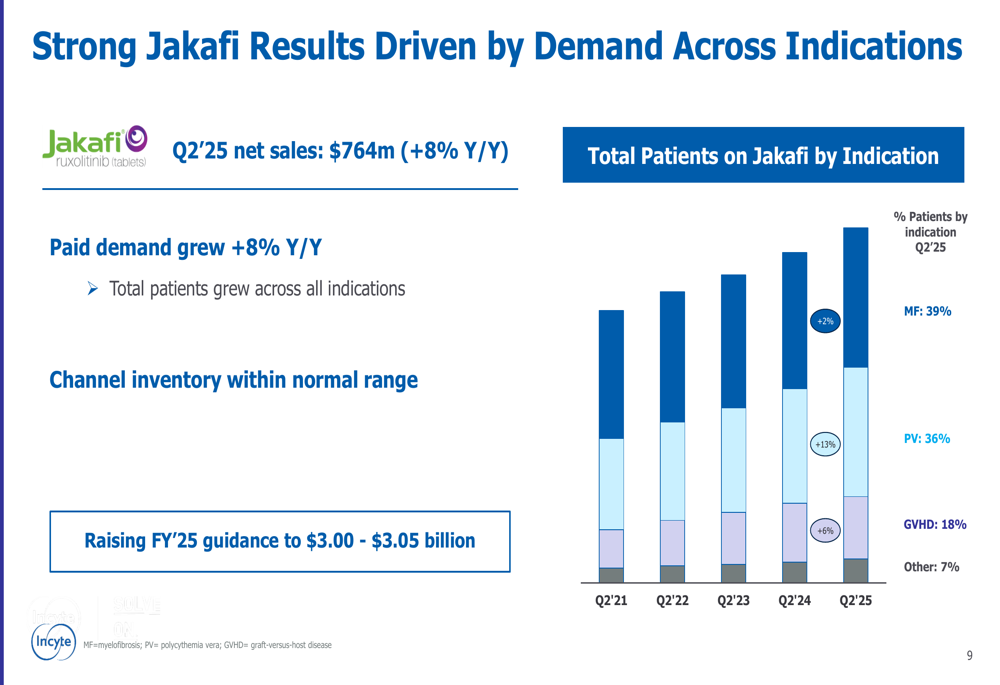

Jakafi (ruxolitinib), Incyte’s flagship product, continued to deliver solid results with Q2 2025 net sales of $764 million, representing an 8% year-over-year increase. The growth was driven by demand across all indications, with total patient numbers increasing in myelofibrosis (MF), polycythemia vera (PV), and graft-versus-host disease (GVHD). Based on this performance, Incyte raised its full-year 2025 Jakafi guidance to $3.00-$3.05 billion.

The distribution of Jakafi patients by indication is illustrated in the following chart:

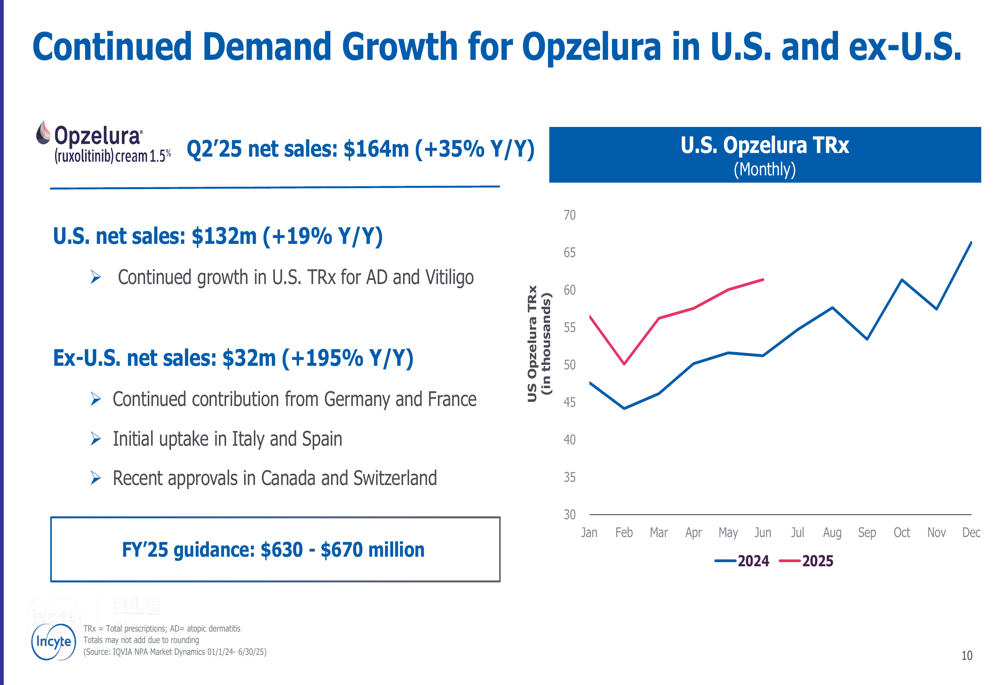

Opzelura (ruxolitinib cream) demonstrated exceptional growth with Q2 2025 net sales of $164 million, a 35% increase year-over-year. U.S. net sales grew 19% to $132 million, while ex-U.S. sales surged 195% to $32 million, benefiting from continued contribution from Germany and France, as well as initial uptake in Italy and Spain. The company maintained its full-year 2025 guidance for Opzelura at $630-$670 million.

The following chart shows the continued growth in U.S. Opzelura prescriptions:

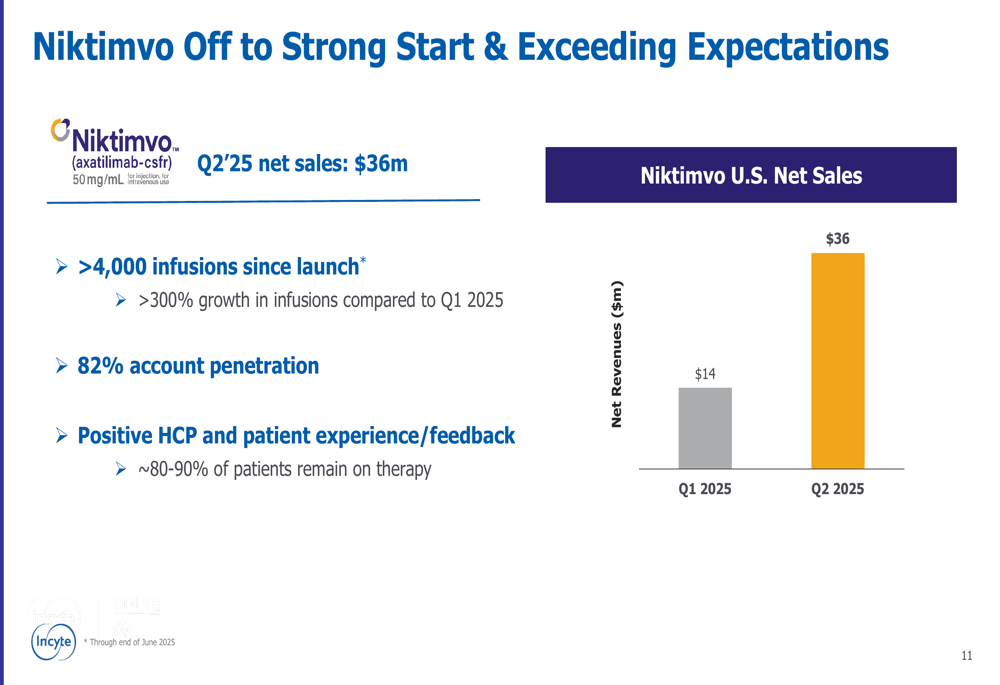

Niktimvo, Incyte’s newest product, demonstrated a strong launch with Q2 2025 net sales of $36 million, a significant increase from $14 million in Q1 2025. The company reported over 4,000 infusions since launch, with more than 300% growth in infusions compared to Q1 2025. Account penetration reached 82%, with approximately 80-90% of patients remaining on therapy.

The rapid growth in Niktimvo sales is illustrated in the following chart:

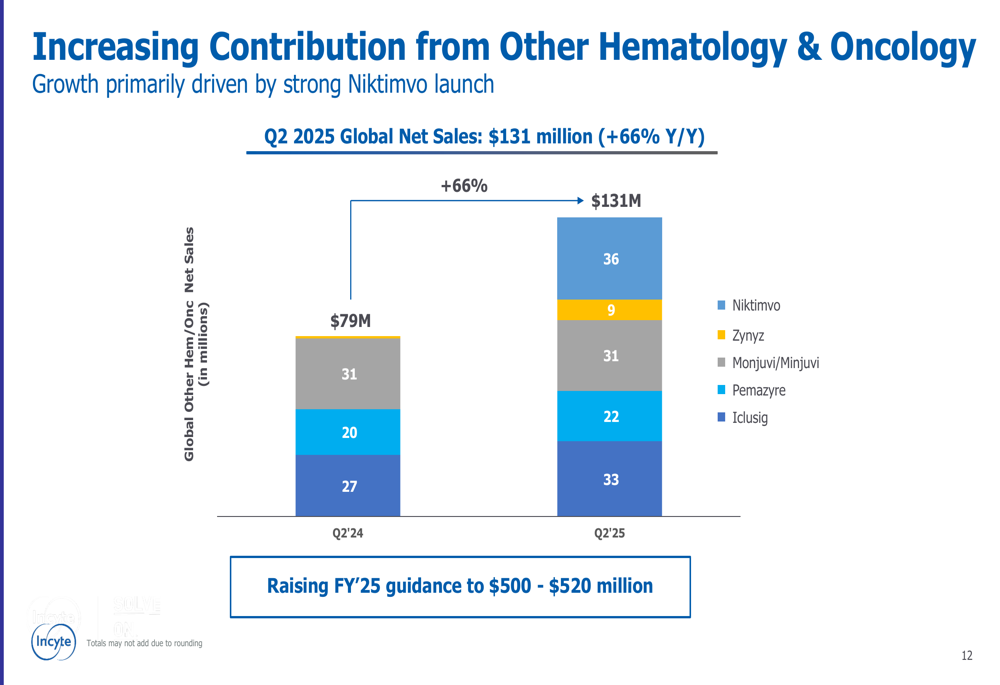

Other hematology and oncology products, including Zynyz, Monjuvi/Minjuvi, Pemazyre, and Iclusig, contributed $131 million in Q2 2025 global net sales, representing a 66% year-over-year increase. Based on this strong performance, Incyte raised its full-year 2025 guidance for this product group to $500-$520 million.

The increasing contribution from these products is shown in the following chart:

Pipeline Developments

Incyte’s presentation highlighted significant progress in its research and development pipeline, with multiple potential product launches expected by 2030 across three therapeutic areas: Dermatology/IAI, MPN/GVHD, and Oncology.

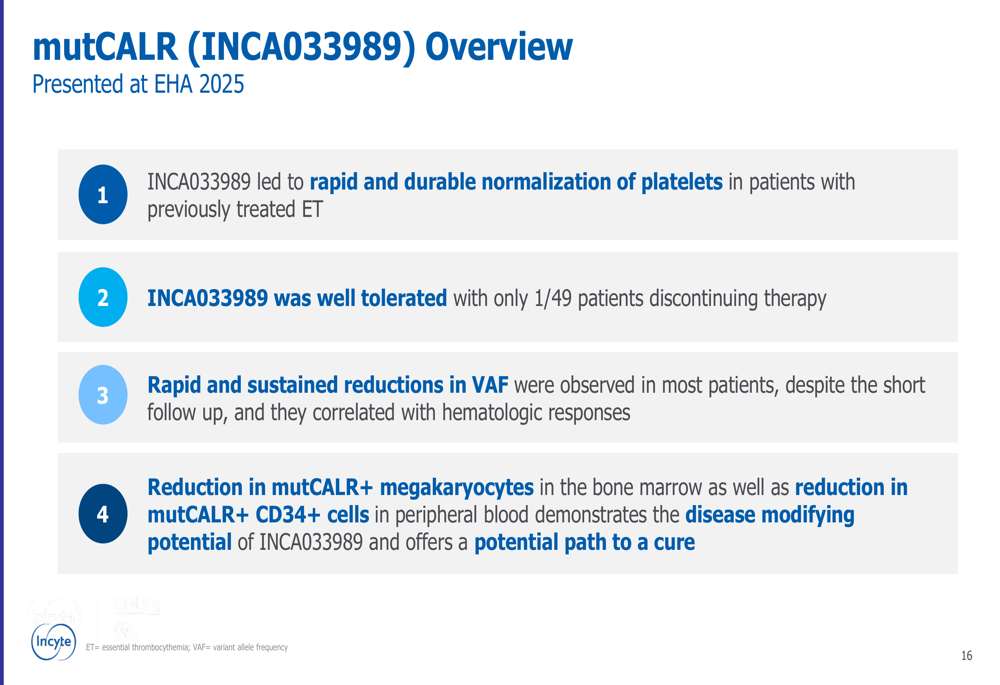

A key pipeline highlight was mutCALR (INCA033989), which showed promising results in patients with essential thrombocythemia (ET). The data presented at EHA 2025 demonstrated rapid and durable normalization of platelets, with only 1 out of 49 patients discontinuing therapy. The company plans to initiate a registrational trial in ET by early 2026 and will present data in patients with myelofibrosis in late 2025.

The key findings from the mutCALR study are summarized below:

Another significant pipeline advancement was the positive Phase 3 results for Ruxolitinib Cream in moderate atopic dermatitis (AD) from the TRUE-AD4 study. The study met both co-primary endpoints and all key secondary endpoints, with a consistent safety profile and no new safety signals observed.

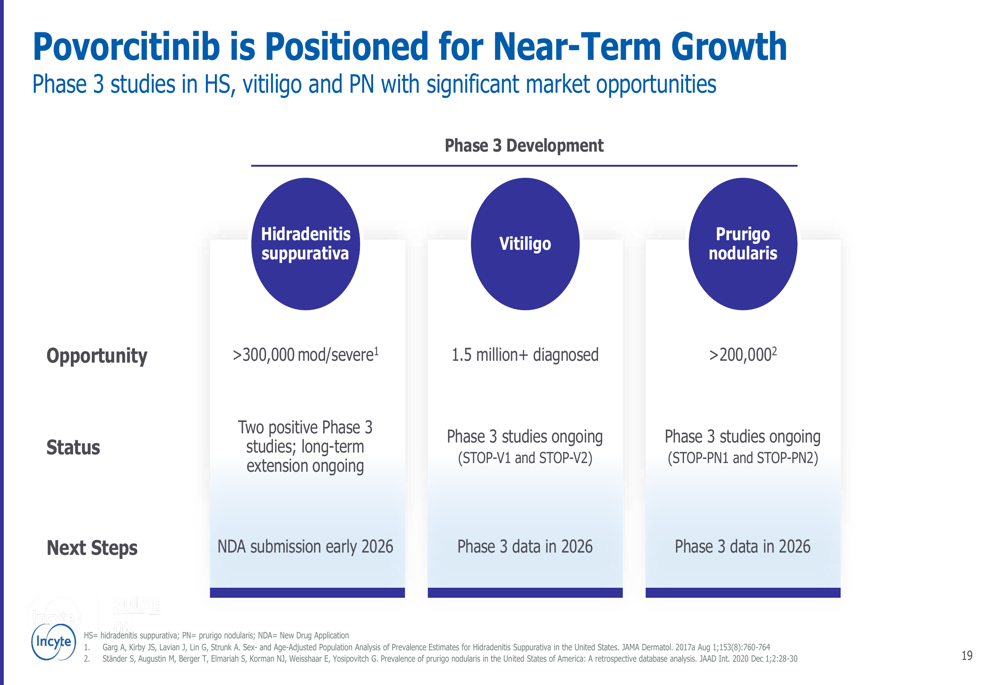

Povorcitinib, another promising pipeline candidate, is positioned for near-term growth with Phase 3 studies ongoing in hidradenitis suppurativa (HS), vitiligo, and prurigo nodularis (PN). The company plans to submit an NDA for HS in early 2026, with Phase 3 data for vitiligo and PN expected in 2026.

The market opportunities and development status for povorcitinib are illustrated below:

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.