The rotation back into growth and defensive parts of the market and out of reflation and value names over recent weeks has been swift, raising many questions about where next for the reflation trade that marked the “hope” phase of the equity cycle.

In a note addressing these concerns among the bank's clients, Goldman strategist Peter Oppenheimer writes that much will depend on near term data around growth and inflation, noting that "the cycle that started after the financial crisis was characterized by a powerful secular trend of growth outperforming value and defensive sectors outperforming cyclicals." While extreme relative to the standards of previous cycles, this dominant trend could be explained by a combination of growth scarcity (both in terms of nominal GDP and earnings – particularly outside of the US), ever lower bond yields – increasing the relative valuation of longer duration assets - and the dramatic bifurcation of earnings growth between growth (and predominantly tech stocks) and most of the rest of the market. Several value sectors faced unprecedented headwinds; the move towards zero interest rates (and negative in Europe) and the need to de-lever weighed on the banks while falling commodity prices hampered the energy related stocks.

Below we excerpt form Oppenheimer's note laying out some of the key observations from the Goldman strategist:

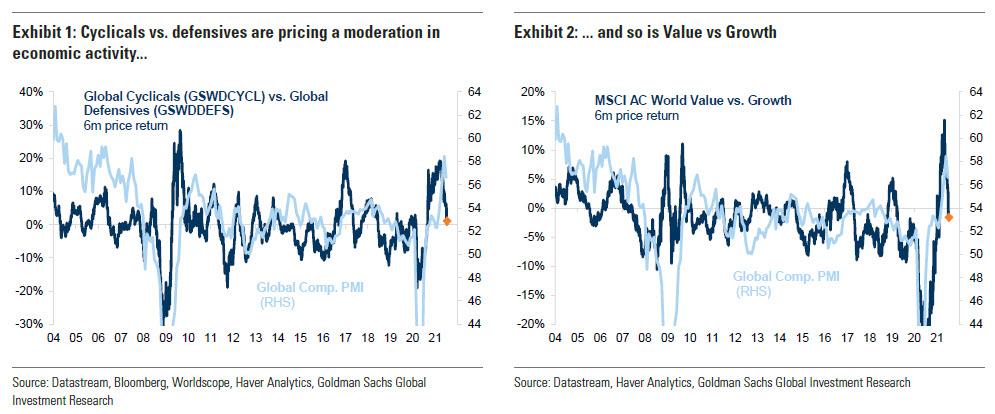

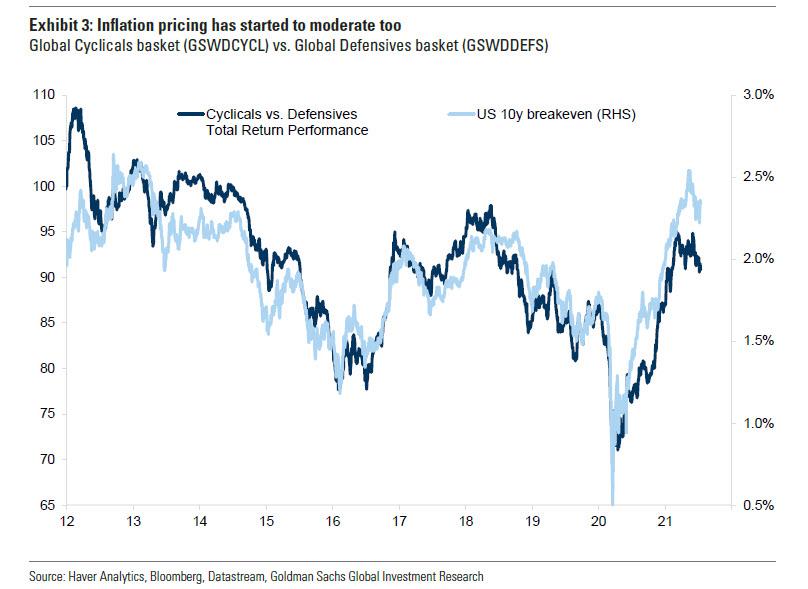

1. The shift towards more cyclical and value leadership that dominated the period from the 2020 March low to the beginning of this year reflected a particularly strong inflection point in growth and inflation expectations following unprecedented policy support and progress on vaccinations. Given that there were record valuation spreads between growth and value parts of the market prior to this inflection point, the shift in confidence had a big impact on market leadership. As Exhibit 1 shows, our baskets of global cyclicals relative to defensives started to outperform on a year over year basis, moving very closely with changes in growth expectations (represented here as the global composite PMI). The recent fading of cyclical outperformance has also coincided with a peak in growth momentum on this metric but would appear to be reflecting an expectation that the global PMI slows to the low 50s. As Exhibit 2 shows, this is also true when we compare global value versus growth.

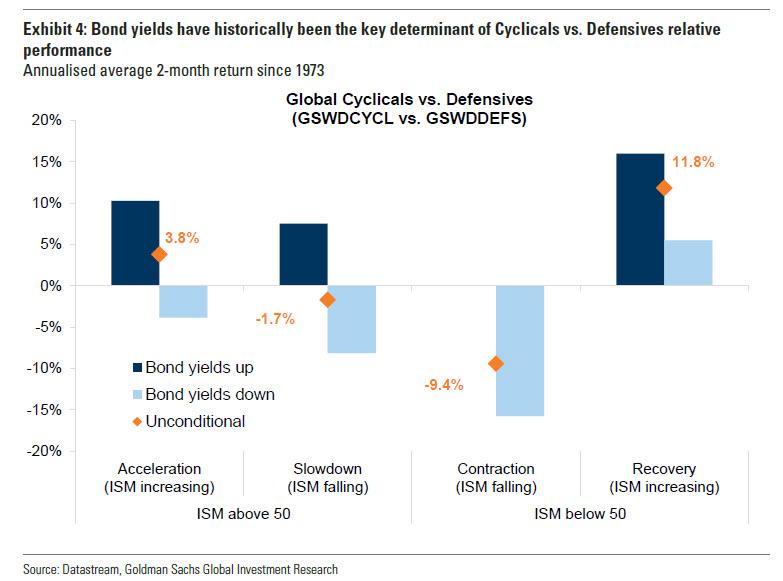

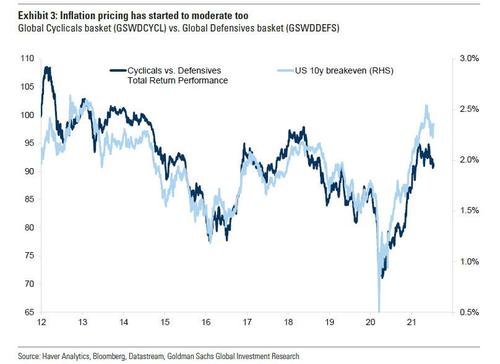

Another key driver of this rotation has been the shift in inflation expectations. As Exhibit 3 shows, the strong outperformance of the cyclical parts of the market also moved closely with inflation expectations which increased sharply in the first phase of the rotation, but has since moderated alongside the peak in growth momentum and also the shift in Fed dot plots.

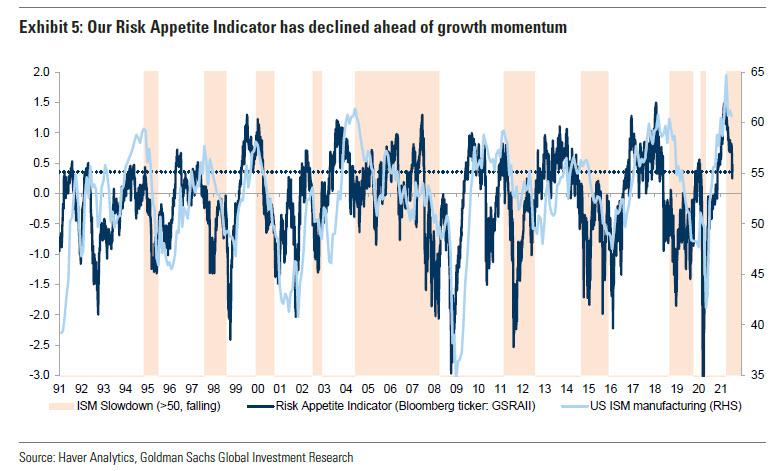

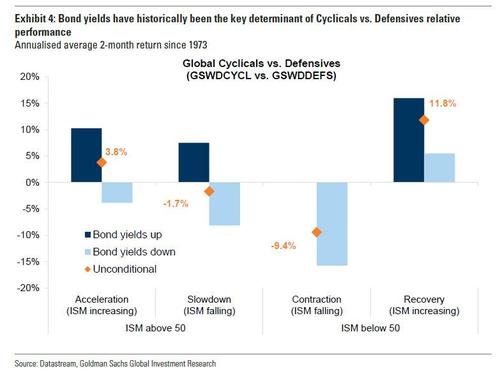

2. As we pass peak growth momentum, a mix of defensive and value areas of the market should continue to perform well and more frequent rotations between the sector styles are more likely now that we are in the “growth phase” of the market cycle. As Exhibit 4 shows, while the despair phase, or period when the ISM is contracting, is consistently negative for cyclicals and positive for defensives, the hope or recovery phase is largely the reverse. This is true irrespective of what is happening to bond yields. The growth phase, broadly consistent with periods when the ISM is above 50 and slowing, is much more ambiguous in terms of leadership and is very dependent on whether bond yields are rising or falling.

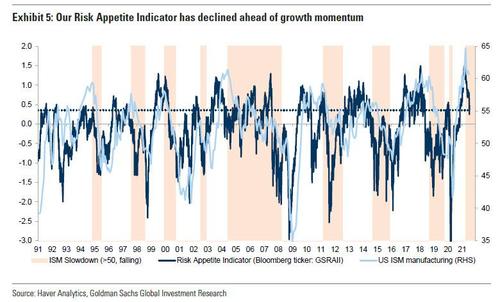

3. More recently, however, the cyclical and value leadership has not just faded but largely reversed. There have been a number of catalysts. A slowing of US growth momentum and the peaking of all four China PMIs in June together with China’s relatively unexpected 50bp RRR cut last week have raised concerns about a loss of global growth momentum. A sharp acceleration in the delta variant has added to this fear, while the shift in US dot plots has increased the focus of a possible policy error as a consequence of tightening policy too early. These worries have been reflected in the pull-back in Goldman's risk appetite indicator (GSRAII) which is also consistent with an expectation that the manufacturing ISM will slow markedly in coming months (Exhibit 5).

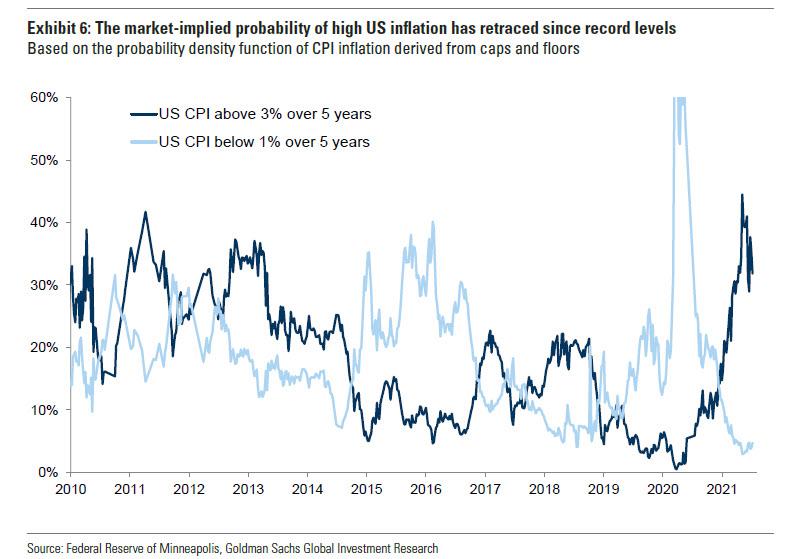

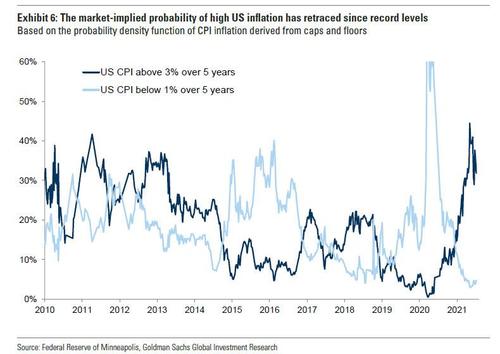

4. Alongside this, we have seen a huge rally in bond markets in recent weeks; US 10 year bond yields have fallen around 15bp and are now back down to 1.2% from 1.7% at the start of April and the 10Y-2Y yield curve has flattened by more than 40bp. The rally has not been confined to the US. German yields are now back down to below -30bp having at one point earlier this year been at -10. Positioning and technicals may have played a part but it is clear that inflation expectations have moderated. As Exhibit 6 shows, the market implied probability of US CPI rising above 3% over 5 years has retraced some of its earlier gains.

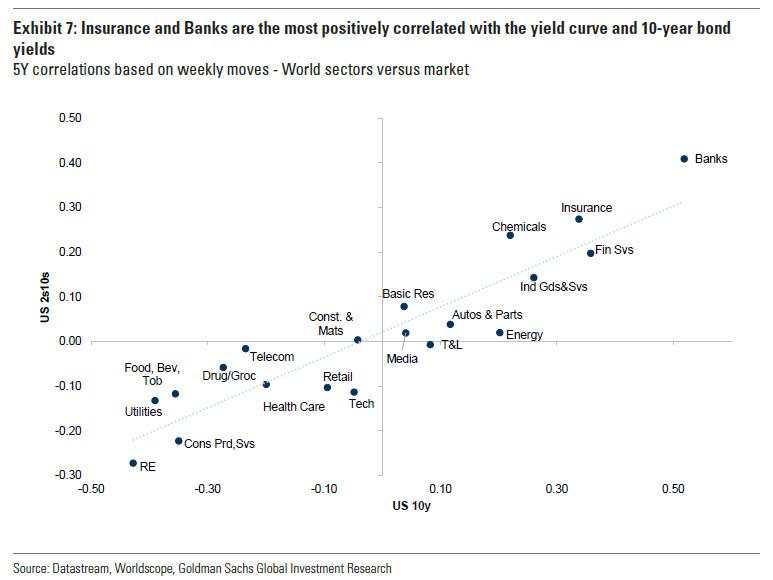

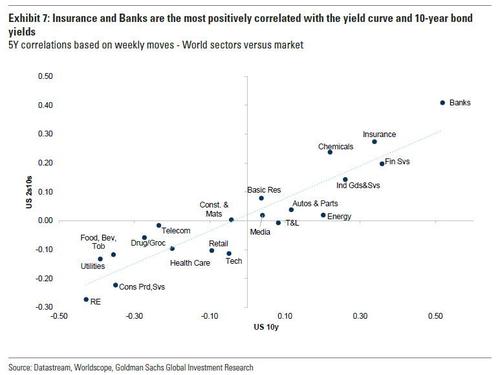

5. Inflation expectations, bond yields and the slope of the yield curve can have a significant impact on sector relative returns, particularly at perceived turning points. As Exhibit 7 shows, classic value areas of the market like banks, basic resources, energy and autos have the highest positive correlation of returns with the slope of the US yield curve and also with US 10 year bond yields. The sharp move lower in these that has occurred over the past few weeks has understandably hit the relative returns of these sectors. But our bond strategists continue to think that these moves have overshot the fundamentals.

6. What can we expect from here? Our view is that in the near term, in the absence of any clarity over the steady state for growth and inflation beyond the current bounce, investors will tend to extrapolate incremental data point, including the current earnings season, and trade the perceived shifts in direction until there is a clearer direction of the medium term trajectory. From conversations with clients, there appears to be no strong consensus on this. Many believe that the cyclical rotation was a short-lived phenomenon driven by a one-off recovery from an unusual recession. Following the sugar rush of stimulus provided by a mix of monetary and fiscal support, we could well go back to a “secular stagnation” environment of slow growth and low interest rates and inflation. This argument is also supported by the fear that higher government debt levels will weigh on future growth should bond yields rise, providing a kind of automatic brake that constrains future growth and inflation. Such an outcome would clearly favour a return to the secular leadership of growth and defensives.

7. The contrary view is that the markets underestimate the inflationary consequences of the current combination of monetary support and fiscal expansion. Despite the arguments of temporary supply bottlenecks driving inflation, the US June core CPI rose by 0.88% month-over-month, a fourth consecutive beat. Used cars and travel/transportation accounted for two-thirds of the increase, but the more persistent and cyclical categories exhibited some strength as well. In coming months, US growth should benefit not only from stronger job creation but also from a positive inventory cycle, following a likely large drawdown in Q2. This narrative is also supported by the expectations that the next few years will be very different from the past cycle. A marginal shift towards more localised supply chains, higher minimum wages and taxation will force higher consumer prices than we have seen before. At the same time policies to support a shift in the energy mix to comply with net zero carbon could add to energy prices paid by industry and consumers. Additionally, a huge boost in carbon neutral investment spending would generate higher material costs and inflation expectations, while increased capex could mop up excess savings, pushing up the level of real yields as well. This outcome would point to a much longer and structural support for cyclical and value parts of the market.

8. In the short term we think the rotation back to defensives and growth has gone too far. Our economists argue that there should be a sizable slowdown as reopening concludes and the fiscal impulse turns negative with spending out of pent-up savings providing only a partial offset (their growth forecast of 2.6% in the US in 2022 and 1.9% in 2023 on a Q4/Q4 basis is now ½-¾pp below the median FOMC projection - see more: Global Views: A Favorable Midyear Report, 6 July 2021), but a much sharper slowdown seems to have already been fully priced in the markets. Furthermore, our rates strategists believe current intermediate and longer maturity yield levels are much too low and do not reflect the macro environment. While they acknowledge that there aren’t any obvious near-term catalysts that will take them back up, they seem to be pricing a pretty adverse outcome and an assumption that BYs are never likely to rise, which we think is wrong - their YE forecast for US 10Y is 1.9%. Given the sharp pullback, we think the asymmetry is getting a lot better for investment in cyclicals/value and our commodity analysts remain positive about commodities.

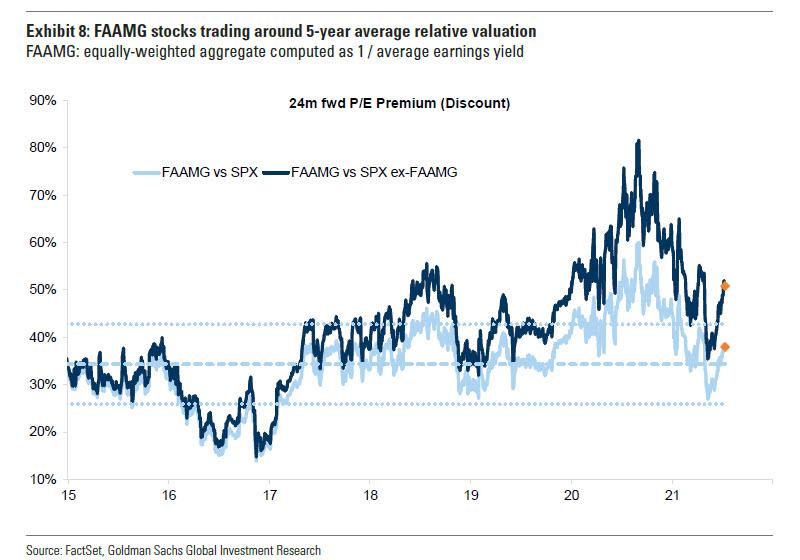

9. Over the medium term Goldman strategists continue to like technology, but their relative valuation has rebounded again and have gone back to pre-pandemic highs. Unprofitable tech, in particular, looks vulnerable to any back up in bond yields which would also likely challenge the renewed outperformance of the US market relative to others.

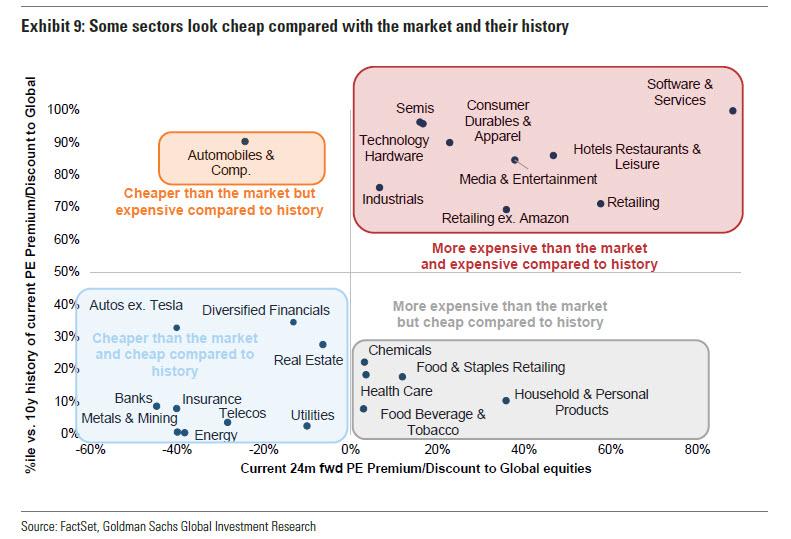

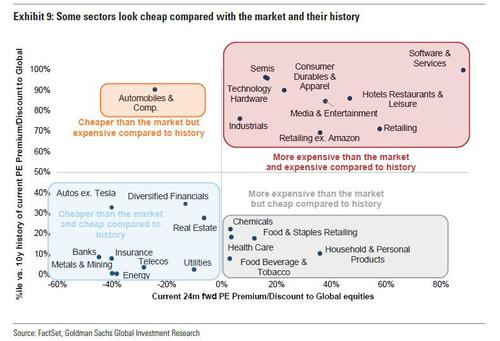

In terms of value, the mix of sectors that look cheap has also shifted over recent months. Exhibit 9 shows the relative valuation based on 24 month forward consensus numbers of the x-axis and the percentile of the relative valuation relative to history on the y-axis. For much of the past cycle the top right would be dominated by mainly long duration growth and defensive sectors while the bottom left would be mainly a mixture of value and growth. In mid June, the cheaper areas were a mixture of deep value (financials, energy mining and autos for example) and some defensive areas like healthcare and consumer staples while the top right was dominated by a combination of long duration technology, like software services, together with many traditional industrial cyclicals.

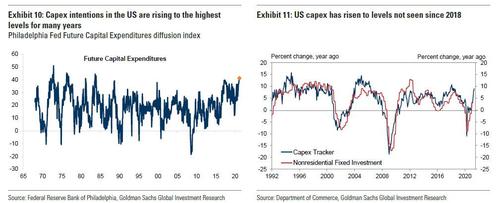

Currently, the same deep value areas remain in the bottom left while some cyclical sectors like industrial and semis have de-rated somewhat and chemicals have moved down from the top right to the bottom right-hand box. Goldman still believes that steeper yield curves will drive another rotation back into some cyclical parts of the market but expect a combination of defensive growth and deep value to offer the best shorter term opportunities. Beyond that, the market will be less dominated by clearly defined by factor and sector leadership in time. The opportunities for market leadership are starting to become more diverse across both sectors and geographies. Technology is becoming a larger component of all industries, while the shift to de-carbonisation is enhancing growth opportunities in the parts of the market that had underperformed for so long. As Exhibit 10 shows, capex intentions in the US are rising to the highest levels for many years, consistent with the readings from our capex tracker.

As Goldman concludes hopefully, "the clear distinction between Growth and Value is likely to fade and give way to a greater focus on alpha opportunities and increased sector and geographical diversification."

https://www.zerohedge.com/markets/whats-next-reflation-trade-9-observations-goldman