By Ye Xie, Bloomberg markets live reporter and strategist

The decline in China’s home construction has been remarkable, almost rivaling the US housing crisis of 2008.

It raises the question: Why are commodity prices so resilient if one of the biggest buyers is in malaise?

It turns out China’s demand for raw materials is more robust than the overall economy. In other words, there’s some decoupling between China’s housing activity and commodities.

US rates and crude oil remain the two most-important variables driving asset prices globally now. WTI crude rose to a one-year high near $94 a barrel. Ten-year yields jumped to 4.6%, pushing the dollar stronger along the way.

The strength in oil, and more broadly the resilience of raw materials, seems at odds with a sluggish Chinese economy, considering the commodity-heavy housing sector remains in trouble. The floor space of newly started housing averaged about 87 million square meters over the past 12 months, marking a 60% decline from a peak in 2021. That isn’t far from the slump in the US housing market during the financial crisis.

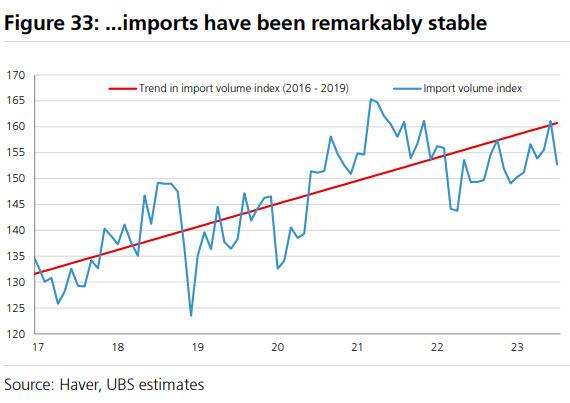

Yet, China’s import volume of commodities from oil and coal to iron ore remains in-line with the trend growth, as shown in this chart from UBS. What gives?

For oil, it’s easier to understand. The US consumes 20% of global oil, compared with China’s 15%. So part of the oil price increase reflects a strong US economy, plus OPEC+ output cut. And in China, while the economy struggles, measures of transportation such as domestic flights and trucking have already risen above the pre-pandemic level, underpinning the demand for fuel.

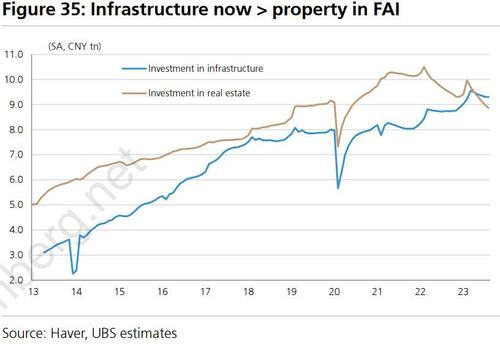

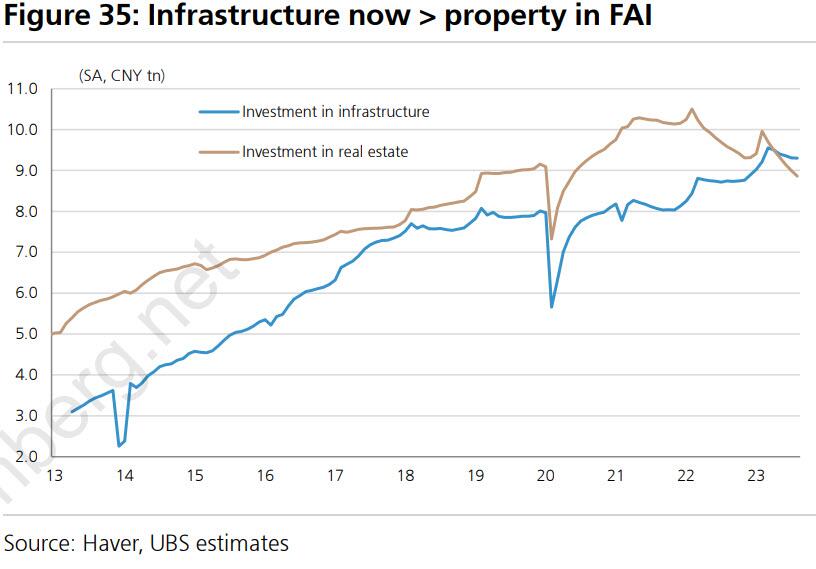

UBS’s strategists including Manik Narain noted two other supportive factors: strength in infrastructure and manufacturing investments, as well as export demand for commodity-sensitive products (steel) and inventory rebuilding (coal). Bloomberg also reported that railway construction has been robust.

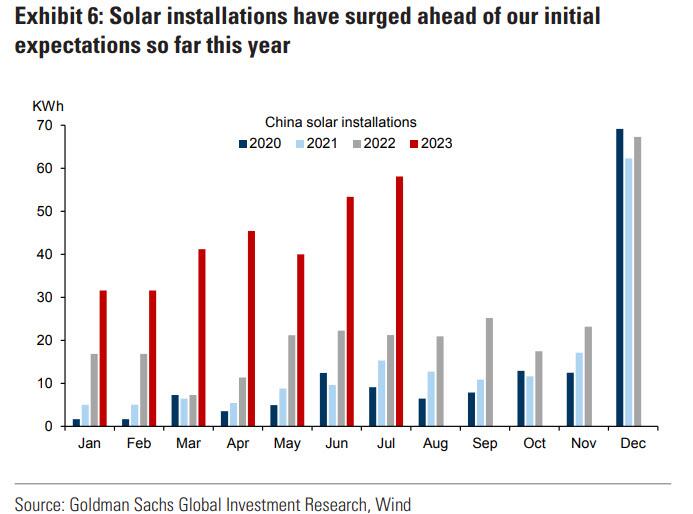

In a report published Wednesday, Goldman Sachs’s strategists Nicholas Snowdon and Aditi Rai also pointed out that the demand for copper and aluminum is supported by growth in renewable energy, the power grid and property completions. For example, China’s solar installations this year have surged.

{kind=link}

So the demand for commodities at idiosyncratic, micro levels is outperforming China’s macro economy. Is this a structural change? That remains to be seen. But for anyone who is bearish on China, shorting commodities hasn’t been a great trade so far.

https://www.zerohedge.com/economics/if-china-so-weak-why-are-commodities-so-strong

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.