A recent federal court ruling threatens to severely limit employers' ability to challenge fiduciary misconduct by their third-party administrators (TPAs) under ERISA who participate in Blue Cross Blue Shield national insurance networks.

On April 22, 2025, Chief Judge R. David Proctor of the Northern District of Alabama issued an order, which dealt a blow to the plaintiffs in the Owens & Minor v. Anthem matter. The order purports to enforce the 2020 $2.7 billion Blue Cross Blue Shield Antitrust Subscriber Settlement Agreement by blocking fiduciary breach claims brought by Owens & Minor (O&M), a self-funded employer, against its former TPA, Anthem Blue Cross and Blue Shield of Virginia.

At the heart of the ruling lies a judicial sleight of hand: the court claims ERISA claims remain intact, yet bars them outright when they involve the very infrastructure—BlueCard—through which the alleged fiduciary breaches occurred. How can a settlement that explicitly preserves ERISA claims nevertheless be interpreted to extinguish them—simply because they involve programs like BlueCard that were mentioned in the antitrust litigation?

Background: The BCBS Antitrust Litigation

The Blue Cross Blue Shield (BCBS) antitrust litigation was one of the most sweeping healthcare antitrust cases in U.S. history. It alleged that the BCBS Association and its affiliated insurers violated federal antitrust law by dividing geographic markets and limiting competition among themselves. The case centered on structural rules—like exclusive service areas and caps on non-Blue revenue—that plaintiffs argued suppressed competition and drove up costs.

Plaintiffs included individual subscribers and self-funded employers, who were represented as subclasses within the broader subscriber class. While providers were also engaged in related litigation, their claims followed a separate legal track. State attorneys general and the Department of Labor (DOL) were not formal plaintiffs or intervenors in the MDL but submitted comments or participated as observers during settlement negotiations and approval proceedings.

Notably, the litigation was about market allocation and anticompetitive behavior—not fiduciary conduct or ERISA compliance. Yet because employers were included in the class, the DOL raised concerns that the settlement could inadvertently interfere with fiduciary obligations. These concerns were purportedly addressed by adding express language to preserve ERISA claims.

The O&M Claims: Fiduciary Breach Under ERISA

In 2023, O&M sued Anthem in the Eastern District of Virginia, alleging that Anthem, acting as a fiduciary to O&Ms self-funded plan, misused the BlueCard Program to inflate costs and that Anthem improperly withheld and concealed key claims data. Anthem allegedly allowed other Blues (the "host" plans) to apply excessive fees and retain overpayments in "variance accounts," all while denying O&M access to records that would allow them to audit and validate those charges.

O&M’s claims were classic ERISA fiduciary breach allegations: Anthem failed to act prudently, placed the interests of the Blues ahead of the plan, and refused to provide information plan fiduciaries are entitled to receive.

The Carve-Out: Settlement Language on ERISA Claims

The Subscriber Settlement Agreement in the BCBS Antitrust case includes a broad release of claims but explicitly states:

“Nothing in this Release shall release claims, however asserted, that arise in the ordinary course of business and are based solely on... challenging a Releasee’s administration of claims under a benefit plan, based on either the benefit plan document or statutory law.”

That carve-out was critical to the Department of Labor (DOL), which raised concerns during the October 2021 fairness hearing. As the final approval order recounts:

“The DOL was concerned with various hypothetical questions about whether this settlement affects any duties employers or plan fiduciaries might have under [ERISA]... However, as the Settlement Proponents have made clear, (1) ERISA plan rights are not affected by the Settlement and, further, (2) the Settlement Agreement does not release any claims that an ERISA plan may have against an employer... To be clear, all ERISA duties still apply.”

The Decision: A Broader Reading of "Released Claims"

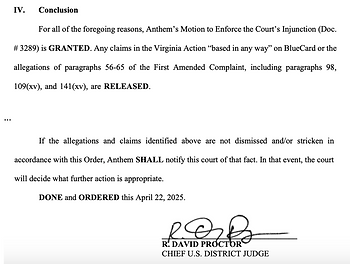

Despite this carve-out and the assurances made in court, Judge Proctor ruled that O&M’s claims were released. Why? Because they were "based in whole or in part" on BlueCard—a subject raised in the MDL proceedings.

“It simply cannot be the case that those claims arise in the ordinary course of business and are based solely on administration of claims under a benefit plan.”

This statement by Judge Proctor deserves closer scrutiny. At face value, this logic appears to negate the very carve-out that was inserted to protect ERISA claims. O&M alleged that Anthem’s fiduciary breaches occurred in its role as a TPA administering claims—precisely the kind of conduct the carve-out aimed to preserve.

Yet the court sidesteps this by emphasizing that the claims involved BlueCard, and because BlueCard was discussed in the MDL, any related fiduciary allegations are swept into the release. This interpretation stretches the concept of “based solely on” beyond recognition. It suggests that if the infrastructure used to administer claims also served some anticompetitive function—or was discussed in a prior litigation—then any ERISA-based oversight tied to that infrastructure is now off-limits.

This logic effectively weaponizes the very system used to cause the alleged harm as a shield against accountability. It’s a form of legal circularity that undermines both the settlement’s promises and ERISA’s fundamental protections.

Despite this carve-out and the assurances made in court, Judge Proctor ruled that O&M’s claims were released. Why? Because they were "based in whole or in part" on BlueCard—a subject raised in the MDL proceedings.

“Even if any argument could be made that BlueCard was not a part of the factual predicate... BlueCard was clearly an ‘issue raised... by pleading or motion.’”

This leaves employers and fiduciaries in a precarious position: told that their rights remain, yet shown that in practice, those rights may be unenforceable if the underlying misconduct shares a factual nexus with an antitrust matter.

Implications for Employers

This decision raises critical concerns for any employer that participated in the BCBS settlement:

Are ERISA fiduciary claims truly protected? The ruling suggests that if the facts of your case intersect with anything discussed in the MDL, your claims could be barred.

What good is a carve-out? If claims "based solely on administration" are still released because they involve topics raised in the MDL, then the carve-out language may be meaningless.

What does this mean for data access and fiduciary oversight? O&M’s case was not about antitrust. It was about whether a TPA mismanaged plan assets. That such a claim could be shut down so easily based upon a settlement in unrelated litigation raises alarms for all fiduciaries trying to comply with ERISA and the Consolidated Appropriations Act.

The Bigger Picture: A Get-Out-of-Jail-Free Card

Put plainly, the judge's ruling seems to block any fiduciary breach claims against the Blues that occurred prior to the settlement date. At least where the term "Blue Card" is mentioned in the Complaint, or the business practices of the Blues form a part of the fact pattern.

Despite the court’s and the DOL’s assurance that ERISA claims would be preserved, the ruling gives Anthem and other Blues a "get-out-of-jail-free" card. Because Anthem used BlueCard—at least in part—to carry out the very breaches alleged, it can now invoke the existence of BlueCard as the reason it cannot be held liable.

In other words, the very vehicle by which these entities allegedly caused extensive harm to employer plans is now the mechanism that insulates them from accountability.

Conclusion

The DOL may have accepted the settlement based on the understanding that ERISA rights were untouched. But in practice, this decision casts serious doubt on whether those rights can be enforced. The court has now interpreted the phrase "relating in any way to" broadly enough to override the very ERISA protections the settlement claimed to preserve.

Plan sponsors should revisit their litigation posture, review past settlements, and assess how much room remains to hold TPAs accountable when systems like BlueCard are involved. Because this much is clear: the line between antitrust resolution and fiduciary immunity just got dangerously thin.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.