The mother of all US reshoring projects, Taiwan Semiconductor Manufacturing Company’s bid to turn the Arizona desert into its number-two production nexus, is exceeding expectations.

At least it is exceeding the expectations of TSMC founder Morris Chang, who predicted that, barring a war in Taiwan, “the effort to increase onshore manufacturing of semiconductors is a wasteful and expensive exercise in futility”.

Chang did get the expensive part right, though.

Diversifying TSMC away from its birthplace is a geoeconomic necessity as the digital age morphs into the artificial intelligence age and China insists on “reuniting” the neighbouring island of 23 million. Some 90 per cent of TSMC’s employees and all of its advanced chip production remain Taiwanese, notes Dylan Patel, CEO of US-based SemiAnalysis. “Three per cent of US GDP is dependent on one square mile in Southern Taiwan,” he writes.

For the same reason, relocation is the business equivalent of pushing water uphill. TSMC’s dominance of the world’s most critical technology depends on what TSMC’s co-chief operating officer, Cliff Ho, characterised as its “one-hour semiconductor system”, with suppliers and expertise almost literally within reach 24/7. The company oversees no fewer than 57 semiconductor programmes at 17 Taiwanese universities to prime its talent pipeline, Patel says. The Taiwanese public does not do Nimby where their national champion is involved.

Hopeful start

TSMC is off to a hopeful start in Arizona nonetheless, says Chris Miller, a Tufts University professor and author of the 2022 book Chip War. “At a high level, it’s going relatively well,” he says. “The US could go from zero to 25 per cent of global chip production by 2035.”

The Taiwanese giant is also building out production in Japan and Germany. But prime customers in Silicon Valley, plus the US’s superpower heft, make the Phoenix-area cluster by far the most ambitious in quantity and quality.

Last March, TSMC expanded its US investment target from $65bn to $165bn — partly to “power the future of AI,” as a press release put it, implicitly to head off the threat of Trump administration tariffs.

There’s a recognition across administrations that this is nationally important and won’t happen on its own

The $100bn jump, like other Trump-era investment promises, should be taken as aspirational, says Phelix Lee, the analyst covering the company for asset manager Morningstar. “Even TSMC can only project demand and technical details three to five years ahead,” he says. “The promise comes with a whole bunch of asterisks.”

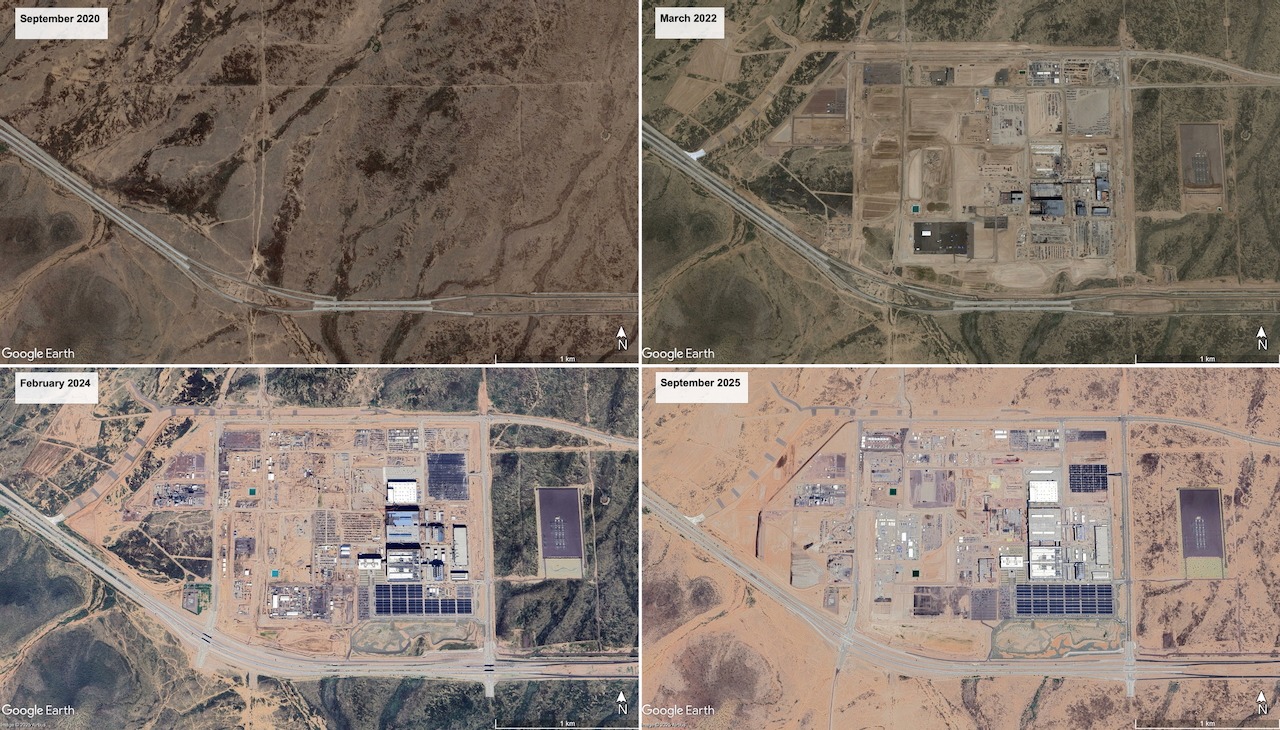

The first US fab was already producing near-state-of-the-art four-nanometre chips in 2024 with a higher yield than in Taiwan, the company claimed. While SemiAnalysis’s Patel suspects some statistical fiddle, “competitive yield on an aggressive ramp timeline is a positive signal for the Arizona project,” he assesses.

Construction on its second fab has also completed, with production expected to start in the second half of 2027, while work on fab 3 started in April 2025. Meanwhile, the company is positioning to further expand its Arizona supercluster. On January 7, it acquired another 900 acres of land adjacent to current site (extending over 1100 acres) and hinted at plans to build more capacity on an earnings call on January 16.

TSMC seems to be navigating the roiling waters of US politics, too. Its Arizona expansion was a poster child for the Chips and Science Act passed under former President Joe Biden, drawing a $6.6bn funding commitment in 2024. Trump has since disavowed this law, like most things stemming from Biden, telling Congress to “get rid of the CHIPS Act”. It remains on the books however, and TSMC betting is that Trump will help it in one way or another.

“There’s a recognition across administrations that this is nationally important and won’t happen on its own,” Miller says.

‘Speed bumps’ ahead

The problem is that recreating a one-hour semiconductor system on US soil will be terribly expensive, if it’s even possible. All systemic costs — construction, labour, energy and water — are much higher in Arizona than Taiwan, Lee points out.

Taiwanese managers are also getting a crash course in dealing with feisty US communities. Local resistance forced partner company Amkor Technology, which packages TSMC chips, to switch sites, though it has dug in at a backup choice near Phoenix.

Lee estimates final output at 15 per cent more expensive than in Taiwan. Miller thinks it could be 30 per cent. “We have always said that Arizona will be margin-dilutive for the entire company,” Lee summarises.

A 15–30 per cent cost increase is currently an inconvenience, not a deal breaker

Binil Starly, director of the School of Manufacturing Systems and Networks at nearby Arizona State University, is scrambling to substitute for those 17 universities funnelling personnel to TSMC back home. “The company’s needs go beyond manufacturing,” he observes. “They need chemical engineers and cyber security experts.”

The highest hurdle may be cultural, however. Compared to Intel, the US chipmaker that also works in the area, TSMC “has a very disciplined culture”, Starly says. “If your machine is down at 2am, you had better come in and fix it. That’s a cultural shift that’s not so common here.”

Morningstar’s Lee is blunter: “There could be speed bumps in introducing what some would call a ‘militaristic’ culture,” he says. “Following orders before questioning them.”

Such challenges are hardly unprecedented for multinational business. Japanese and Korean automakers with similar top-down DNA have learned to thrive in the depths of the US over the past 40 years. But the technical complexity, scale and geopolitical stakes of TSMC’s Arizona venture may be unique.

One big advantage for the company is that both it and some key US customers are near-monopolists in a mushrooming tech ecosystem. So a 15–30 per cent cost increase is currently an inconvenience, not a deal breaker. “Our base case is they are able to pass on those costs to Nvidia, Apple and others,” Lee says. “TSMC is working with 60 per cent margins anyway.”

Circumstances may change on the way to investing $165bn. So far, so good.

https://www.fdiintelligence.com/content/f24e3fc7-5d62-4686-95ab-5b1ce6524737

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.