FinCanna provides financing to startup businesses in the cannabis industry in the form of perpetual royalty payments and/or loans.

The FinCanna management team has built a creative structure in which they help fund a highly capital-constrained industry – with strong growth prospects – at favorable terms.

While the investment portfolio remains unproven and significantly concentrated in one portfolio company, if the portfolio performs as expected FinCanna should generate ROI’s of 25%+ and support a high-margin business.

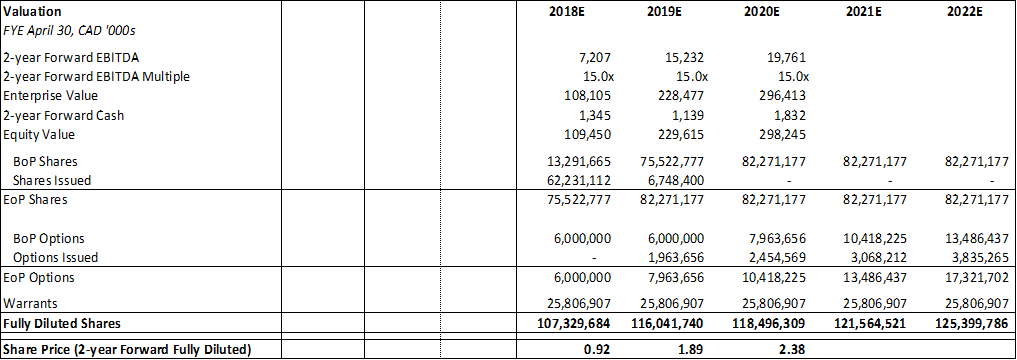

I value the company at 15x 2020 expected EBITDA, which equates to a price target for CALI of CAD 0.92.

Editor’s note: Seeking Alpha is proud to welcome Key Investment Partners as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to the SA PRO archive. Click here to find out more »

(Editor’s Note: Investors should be mindful of the risks of transacting in securities with limited liquidity such as FNNZF. FinCanna Capital’s listing on the Canadian Securities Exchange under the ticker CALI offers somewhat stronger liquidity.)

Overview of Investment Thesis

FinCanna Capital Corp (“FinCanna” or “the Company”) has developed a creative business model to finance startups in the capital-constrained cannabis industry. The management team invests in perpetual royalty payments at rates well above what could be earned in other industries given the limited number of competitors providing capital. FinCanna has funded three companies to date, all of which have shown positive momentum in their early days. However, on top of the numerous risks faced by most companies in the cannabis industry, FinCanna is exposed to significant concentration from its flagship investment, Cultivation Technologies, Inc. (or “CTI”). I value the company at 15x 2020 expected EBITDA, which equates to a price target for CALI of CAD 0.92. Once FinCanna’s royalties start flowing through the company’s P&L in FY’19 (year-end April 30), I expect that investors will take notice of this high-margin, scalable business model and that the stock price should rise accordingly.

Company Overview

Background

FinCanna was formed in Vancouver in November 2016 out of necessity. The management team of CTI had a permit approved to build a cannabis production and testing facility in Coachella, California (the “Coachella Project”) but needed funding (i) to acquire the real estate and (ii) to construct & operate the facility.

CTI’s management team began discussions with Astar Minerals Ltd. (“Astar”) regarding financing the project in 2016. Astar had initially formed as a project finance company for the exploration and development of minerals in Canada. After its initial exploration program returned inconclusive, Astar’s management team began exploring other business opportunities, which eventually led to the CTI introduction. However, Astar was publicly listed on the TSXV, an exchange which prohibits its listed companies from conducting cannabis business in the US. Instead, Astar’s principals connected CTI with individuals they viewed as capable of running a cannabis-focused investment vehicle, which became FinCanna. In turn, Astar was acquired by FinCanna in a reverse takeover (“RTO”)1 and was listed on the Canadian Securities Exchange (“CSE”), an exchange which does not have the same restrictions as the TSXV, in conjunction with the RTO. FinCanna now trades on the CSE as CALI and the OTCQB as FNNZF.

Business Model

FinCanna operates as an investor to companies in the cannabis industry, specifically focused on businesses operating in California. FinCanna has developed an investment portfolio over the past two years by raising capital through private placements of shares, then using those funds to invest in cannabis startups. The Company typically makes royalty investments, in which the portfolio companies pay FinCanna a certain percentage of their revenue in perpetuity (like the strategy commonly employed by Kevin O’Leary of Shark Tank). This structure provides an alternative option for cannabis companies who do not have access to financing from traditional sources and who may prefer to avoid giving up common equity at an early stage.

Prior to the RTO, FinCanna raised approximately CAD 6.3m through private placements2. In conjunction with the RTO on December 27, 2017, FinCanna privately placed shares for an additional CAD 7.1m. Year-to-date through August 16, 2018, the Company has completed two additional private placements for a total of CAD 10.0m. This capital (a cumulative CAD 23.5m) is being used to fund FinCanna’s investments (discussed further in Investment Portfolio). FinCanna plans to fund future investments through the cash flows generated by its existing portfolio. However, should FinCanna chose to invest in more companies in the near-term, the Company will likely need to privately place shares of CALI, leading to shareholder dilution3.

Investment Portfolio

CTI Permanent Facility: CTI is a provider of infrastructure, technology, manufacturing, and branding to the medical cannabis industry in California. CTI’ Coachella Project is a 6-acre medical campus and will include dedicated space for cultivation, manufacturing, distribution, lab testing and transportation. The 111,500 square foot facility will be developed in phases. Once at full capacity, the facility is expected to process 30,000 – 50,000 pounds of biomass per month, producing 18-30m grams of raw cannabis oil per annum.

FinCanna has committed to investing USD 8.1m in the Coachella Project in exchange for a 14% royalty from the facility. Additionally, this investment grants FinCanna the right to finance CTI’s next two licensed cannabis facility projects on the same terms (CTI is currently pursuing a second site in Colusa, California and has already obtained development entitlements for the first phase of the project)4.

In addition to the royalty payment, FinCanna has agreed to provide a USD 6.0m loan to CTI that matures in January 2023. This loan earns interest at 20% per annum and is secured by CTI’s assets. While the loan is outstanding, 7% of CTI’s revenues will be applied to pay down the interest and principal on the loan until it is fully repaid. Further, FinCanna has the right to convert the loan into a percentage (up to 5%) of CTI revenues on projects FinCanna chooses not to fund5.

CTI Interim Facility: While CTI’s permanent Coachella campus is under construction, an interim facility began operations in January 2018. The interim facility has the capability to process approximately 6,000 pounds of monthly biomass, which can produce approximately 3.7m grams of raw oil per annum. Further, CTI can add extraction equipment resulting in additional capacity of 3,000 pounds of monthly biomass. As of June 7, 2018, CTI’s interim facility had earned more than USD 1m revenue. While the interim facility is operational, FinCanna is entitled to receive 50% of its profits.

Green Compliance Inc.: FinCanna’s second investment, Green Compliance Inc., provides enterprise compliance and point-of-sale software (“ezGreen”) to licensed medical cannabis dispensaries and cultivators. Green Compliance has commenced sales in the US and targets dispensaries in all states (including Washington, D.C.) where medical cannabis is legal. FinCanna has agreed to fund USD 3.0m in tranches by September 2018 in exchange for a perpetual royalty of 10% of gross revenue, subject to certain buy-back options6.

Source: EzGreen – Compliance Mastered

Refined Resin Technologies Inc.: FinCanna and Refined Resin executed a royalty agreement in early July. Refined Resin is a cannabinoid research and refinement company that has leased a facility in Oakland and is currently in the process of retrofitting the facility, with plans to begin operations at the end of 2018. Refined Resin plans to produce bulk quantities of THC distillate and various concentrates and to provide white labeling services to other manufacturers who do not have access to compliant production facilities. Under the agreement, FinCanna will invest USD 3.0m in tranches in exchange for a tiered corporate royalty between 5% and 14% of Refined Resin’s revenues, adjusted based on revenue levels. FinCanna will also acquire an additional royalty of 2% of revenues for USD 1.795m (USD 0.5m in cash and the remainder in FinCanna shares), subject to certain repurchase terms.

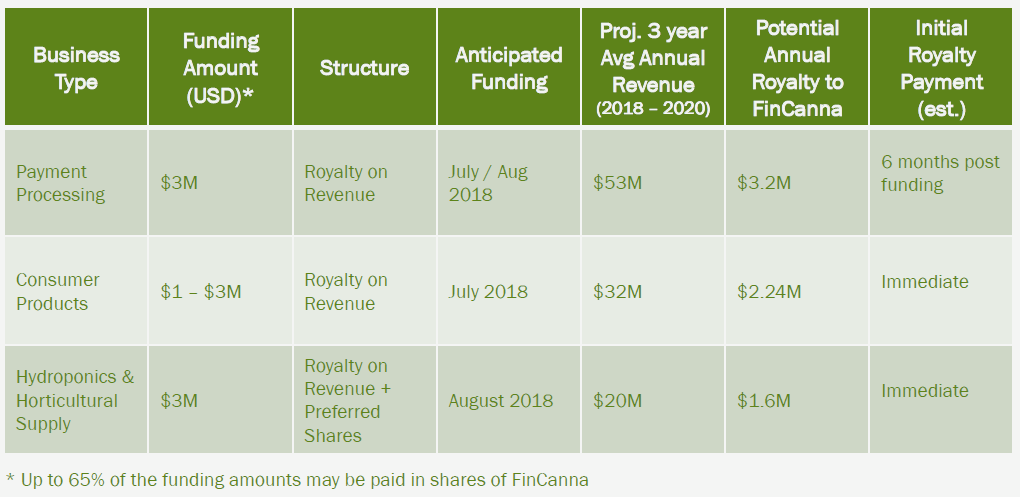

Pipeline Opportunities: As of June 1, 2018, FinCanna had three pipeline opportunities for future investments at the Term Sheet stage. Summary terms for those opportunities are as follows:

Management Team

Andriyko Herchak, CEO: prior to running FinCanna, Mr. Herchak spent 20 years on the executive team of various publicly traded companies. From 2015 to 2017, Mr. Herchak served as CFO of Jewel Holdings Ltd., the largest end to end spooling/piping welding company in Western Canada, and from 2013-2014 he served as CFO of Nexgen Energy Ltd, a publicly listed uranium exploration and development company. From 2007 to 2012, he was CFO of Harthor Explorations, also a publicly listed uranium exploration and development company that raised CAD 100m equity and was eventually sold to Rio Tinto for CAD 650m. Mr. Herchak currently serves on Sixty North Gold’s Board of Directors (CSE: “SXTY”).

Robert Scott, CFO: Mr. Scott has over 20 years of experience in corporate finance positions. Mr. Scott is also the Founder and President of Corex Management Inc., a private company providing accounting, administration and corporate compliance services.

Industry

Given the size of California’s market (it would be the 5th largest country in terms of GDP if it was a sovereign nation), FinCanna’s management team has decided to focus on funding California based-companies. Legal cannabis sales in the state are projected to total USD 4.3bn in 2018 and to grow to USD 6.5bn by 20207. Cannabis businesses have limited funding available to finance their startup costs for a variety of reasons, including (i) national banks refuse to fund the industry due to the plant’s federal illegality and (ii) traditional venture capital funds typically avoid the industry due to regulatory concerns and vice clause8 restrictions. This has left a gap in the market for companies like FinCanna to develop clever financing structures and receive favorable terms with ROI’s well above what could be earned investing in other industries.

Investment Merits

Above market financing terms. In today’s regulatory environment in which traditional lenders have generally avoided lending money to cannabis companies, FinnCanna fills a unique market hole by providing financing in exchange for royalty payments. Most other financiers in the cannabis industry typically take significant common equity from their portfolio companies, which many founders consider more expensive in the long run. FinnCanna has shown its ability to capitalize on these market dynamics by (i) lending expensive paper at 20% interest and (ii) making royalty investments, which I assume generate a three-year ROI of approximately 27% (discussed further in Financial Performance & Valuation).

Positive momentum at CTI. CTI remains FinCanna’s most important portfolio investment, representing approximately 64% of the Company’s investment dollars to date. While CTI is privately owned, thus making financial information highly limited, CTI’s Coachella Project has demonstrated positive momentum in recent weeks, including (i) reaching over USD 1m sales and (ii) winning the exclusive rights to manufacture Phoenix Tears THC products in California. Further, CTI’s interim facility was positively impacted by an unexpected regulatory change that allowed CTI to own 100% of the facility, in effect increasing their profit expectations from the interim facility 5x.

Inexpensive valuation for the cannabis industry. Given (i) the uniqueness and complexity of FinCanna’s business model as well as (ii) the illiquidity of its stock due to low trading volumes, I view the Company as materially undervalued, especially relative to well-known and less scalable operators in the industry. I value the Company at a 15x 2020 EV/EBITDA multiple (discussed further below in Financial Performance & Valuation), which places the price target for CALI at CAD 0.92, well above the August 16, 2018 closing price of CAD 0.25. Given the industry-wide and company-specific risks discussed below in Investment Risks, I believe this significant upside potential (approximately 4x) is necessary to justify any investment in the cannabis sector.

Targeting the right market: California. As federal prohibition in the cannabis industry restricts companies from engaging in interstate commerce, each state that has legalized adult-use cannabis effectively acts as an independent nation with different regulations. FinCanna’s management team understands these dynamics and has intelligently chosen to focus on California, which is the largest legal market in the world and is still a very nascent industry (adult-use sales in the state just began on January 1, 2018).

Success of portfolio investments are not dependent on exit events. For financing companies that invest in cannabis businesses in exchange for common equity, the most important driver of their investment returns is an exit event (e.g. selling public shares of their portfolio company following an IPO or selling the entire business to a larger, strategic acquirer). Given the uncertain regulatory environment in the cannabis industry today, many companies have limited exit options, as (i) they are generally unable to meet the requirements for filing on a major exchange, (ii) companies listed on the CSE are often materially mispriced, and (iii) natural strategic acquirors like big pharma, big agriculture and big tobacco have generally shown reluctance to enter the cannabis industry. However, because FinCanna receives ongoing royalty payments based on revenues from its portfolio, exit timing is less of a concern for their book of business as their investments will generate recurring cash flows.

Investment Risks

Industry-wide risks. FinCanna faces numerous, industry-wide risks exhibited by most publicly traded cannabis companies, including:

- The legal cannabis industry is nascent and highly fragmented, consisting predominantly of early-stage and unprofitable businesses. Regulations are unpredictable and constantly changing, which can materially impact performance.

- Stocks traded on OTC markets and the CSE are thinly traded, which makes the investments more volatile than stocks listed on major exchanges (e.g. NYSE, NASDAQ and TSX). OTC securities are not registered with the SEC and are often unaudited, leading to less regulatory oversight and making these securities more susceptible to market manipulation (e.g. “pump and dump”).

- Stocks listed in USD on OTC markets derived from a CSE-listed Canadian security are even less liquid than the native Canadian security, which can lead to significant bid ask spreads. USD/CAD foreign exchange fluctuations uncorrelated to the underlying security’s performance are passed onto the investor, leading to more volatility in the security’s price.

Significant portfolio concentration in CTI’s Coachella Project. While FinnCanna’s management team continues working to diversify its portfolio of investments, 64% of its investments to-date have been made in the Coachella Project (27% in the form of a loan and 37% in a royalty investment). Key risks specific to CTI include (i) the inability to raise enough funding to complete the Coachella plant build-out, (ii) timing delays in construction which would restrict their ability to pay interest and principal on the loan and (iii) declines in California’s cannabis oil price. Given the early stage of FinCanna’s book of business, should the Coachella Project fail, FinCanna would also likely fail as they will have lost the confidence of public investors, whose money they need from subsequent equity funding rounds to make more investments.

The investment portfolio is unlikely to become self-funding until 2020 at the earliest. FinCanna’s ability to make new royalty investments, which will provide further earnings potential and diversify their risk from their existing portfolio of just three companies, is dependent on their current portfolio throwing off sufficient cash. CTI, ezGreen and Refined Resin are all very early-stage companies, so this model will likely not become self-funding until at least 2020. In the meantime, FinCanna’s management team will either need to pass on pipeline opportunities, or they will need to issue new shares of CALI, which will lead to dilution for the existing shareowners.

Information on the status of underlying portfolio companies is critical yet difficult to ascertain. Valuing FinCanna and projecting their future cash flows is very difficult, as their underlying investments are all privately owned and thus do not disclose their financial performance. This same restriction applies to FinCanna’s management team, who depends on their underlying investments providing accurate financials and paying the proper amount of royalties (although FinCanna does have audit rights over its investments)9. In a downside scenario where performance at CTI, ezGreen and/or Refined Resin declines, the management teams of those companies may be incentivized to falsely report their numbers to FinCanna and to underpay what they contractually owe.

More competitors (e.g. traditional lenders and venture capitalists) will enter the industry as fear of retribution abates. The regulatory momentum across the US has been overwhelmingly in favor of legalizing cannabis, and this momentum appears to be accelerating. While this shift is certainly positive for the industry from a macro perspective, it will cause FinCanna to lose its competitive advantage over time. Once banking legislation has been changed to protect financial services companies and more traditional lenders enter the industry, FinCanna’s ability to drive above-market terms on its investments will decrease.

CAD/USD FX volatility. Because the Company reports in CAD but funds investments/ generates revenue in USD, the Company is exposed to transactional and translational FX swings. American investors in FNNZF are partially hedged from these FX swings, as a stronger USD will increase FinCanna revenue in CAD but decrease the market price of FNNZF relative to CALI (and vice versa). Note that because the Company only invests in California in USD and plans to reinvest all cash flows back into the state instead of repatriating cash to Canada, FX swings do not impact the Company’s operations (only its financial statements).

Financial Performance & Valuation

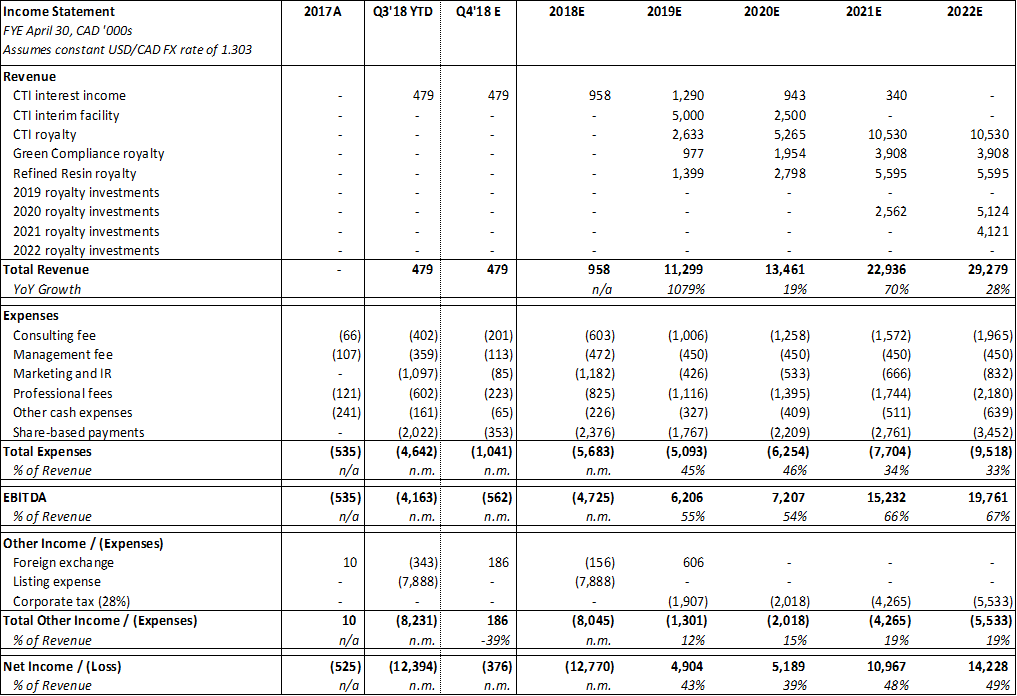

As noted in the Investment Risks above, projecting FinCanna’s financials is very difficult given the underlying portfolio’s (i) limited information available and (ii) uncertain timing of cash flows. However, I assume that once portfolio companies are operating at full capacity, they will generate royalties of approximately 100% of FinCanna’s investment each year, which is supported by the annual revenue expectations FinCanna presented for their Pipeline Opportunities. For example, the Payment Processing opportunity has the potential to generate a USD 3.2m annual royalty, approximately equal to the USD 3.0m funding amount, and the Consumer Products opportunity has the potential to generate a USD 2.24m annual royalty, approximately equal to the midpoint of the USD 1-3m funding amount. I further assume the portfolio companies take three years to reach their run-rate, returning 25% of FinCanna’s investment in year one, 50% in year two and 100% in year three and thereafter. This equates to an expected 3-year ROI of approximately 27% for each, which is a 700bps premium to the 20% interest FinCanna charges on the CTI loan.

In FY’19 (the year ended April 30, 2019), I expect FinCanna’s portfolio to generate sufficient cash flow to fund their existing investment commitments, but not enough to fund any additional opportunities. In the subsequent years, I expect the Company to utilize 90% of free cash flow to make new royalty investments, which will follow the same 25%, 50% and 100% pay-out in years 1-3. Further, I expect the majority of FinCanna’s expenses to grow at approximately 25% p.a., driving the Company to a steady-state EBITDA margin of 65-70%. I further assume the Company should trade at 15.0x 2020 expected EBITDA of CAD 7.2m, equating to an Enterprise Value of CAD 108.1m or a price per share of CAD 0.92 once considering dilution from stock options, warrants, and the component of the Refined Resin investment issued in the form of FinCanna equity.

The August 16, 2018 CALI closing price of CAD 0.25 is materially lower than when FinCanna started trading in January 2018 at CAD 1.02 (75.5% decline). Much of this decline is likely attributable to the unfortunate timing of FinCanna’s RTO, which took place shortly after a bull-run in cannabis stocks and days before US attorney general Jeff Sessions repealed the Cole Memo10, which has been a major contributor to the broader cannabis industry’s price decline (the Global Cannabis Stock Index is down 36.1% YTD). There is not a clear indicator as to why FinCanna’s performance YTD has been so much worse than the broader cannabis index, but I would reiterate that given the stock’s illiquidity and dearth of institutional investors, the market price is not a useful indicator of the stock’s intrinsic value. Additionally, I believe other public investors are generally (i) unaware of the company due to its small market cap and lack of institutional, sell-side research coverage, (ii) do not understand the business model because of its uniqueness and complexity and (iii) have not taken the time to project financials, which show a clear pathway to strong profitability in a short timeframe.

Comparable Companies

Publicly traded comparables consist of specialty finance companies focused on investing in small-cap and middle-market companies, predominantly in the form of syndicated, secured debt. These companies trade at a median 19.7x EV/EBITDA multiple, to which I apply a discount of approximately 25% to arrive at the 15.0x multiple for FinCanna. This 25% discount is justified due to:

- FinCanna’s 2-year forward-looking EBITDA vs. comparable companies’ LTM EBITDA

- The higher risk of the underlying cannabis industry relative to the more mature, traditional industries financed by comparable companies

- The concentration of FinCanna’s investment portfolio

- The fact that comparable companies typically invest in loans fully secured by their portfolio companies’ assets, while FinCanna has not disclosed the underlying securitization of their royalty investments

These factors are partially offset by the stronger growth profile of the cannabis industry.

Conclusion

FinCanna utilizes its creative and scalable business model to fund cannabis companies that have limited other options for accessing capital. While the portfolio today is concentrated and early-stage, the Company is at an inflection point and should start receiving material cash flows over the next 12-18 months. The stock, which has been flying under the radar since the reverse takeover, has the opportunity for the material price appreciation necessary to justify the investment’s extremely high risk profile.

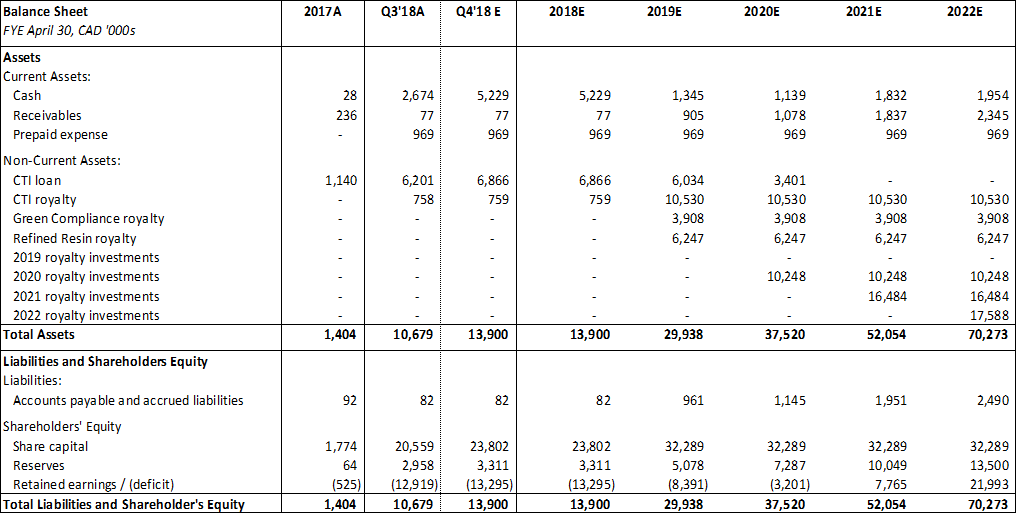

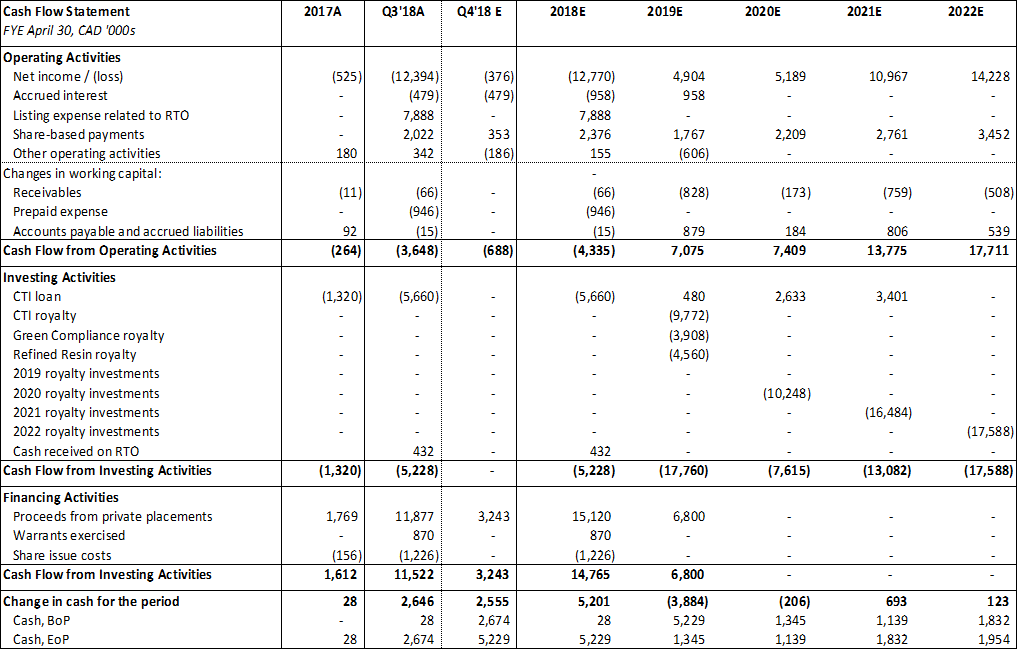

Financial Model

[1] Public Filing: FinCanna Capital Corp – Annual Information Form for the year ended April 30, 2017

[2] Public Filing: FinCanna Capital Corp – Consolidated Interim Financial Statements for the six months ended October 31, 2017

[3] Dilution refers to the reduction in the ownership percentage of a company due to the issuance of new equity shares by the company. When FinCanna privately places new shares, they have historically offered the new shares at favorable terms relative to the outstanding shares to attract larger investors. For example, during the last private placement, CALI shares were trading around CAD 0.30. Investors in the private placement were able to buy common shares at CAD 0.30 and also received a warrant to purchase an additional common share at an exercise price of CAD 0.45 for the next 24 months. As such, when valuing the company and setting a price target, I assume full dilution from outstanding warrants and options. As of June 1, 2018, the Company had 75.5m shares issued, 25.8m warrants and 6.0m options outstanding.

[4] Public Filing: FinCanna Capital Corp – Annual Information Form for the year ended April 30, 2017

[5] Public Filing: FinCanna Capital Corp – Annual Information Form for the year ended April 30, 2017

[6] Public Filing: FinCanna Capital Corp – Annual Information Form for the year ended April 30, 2017

[7] Arcview Market Research

[8] Restrictions imposed by the underlying investors in a VC fund that prevent the funds from investing in certain sectors such as alcohol, tobacco, or drugs.

[9] Public Filing: FinCanna Capital Corp – Annual Information Form for the year ended April 30, 2017

[10] Memorandum issued by Obama’s Attorney General James Cole in August 2013 which stated that the Justice Department would not enforce federal marijuana prohibition in states that “legalized marijuana in some form and … implemented strong and effective regulatory and enforcement systems to control the cultivation, distribution, sale, and possession of marijuana”.