by Adam Sharp

Both President Trump and Iranian leaders are standing firm on their red lines.

Before peace negotiations restart, Iran has made 5 demands:

- Ending the war on all fronts, including Lebanon

- Lifting all sanctions

- Releasing frozen Iranian assets

- Compensation for war damages and losses

- Recognition of Iran’s sovereign rights over the Strait of Hormuz

Trump called the proposal “TOTALLY UNACCEPTABLE!”.

The President has criticized Obama fiercely for releasing frozen Iranian funds, and hasn’t backed down on that subject.

As far as paying compensation, that’s not going to happen either. Sanctions relief could come in time, but asking for a total end before negotiations restart is a pipe dream.

And ending the war in Lebanon would mean Israel would have to stop bombing Hezbollah and likely give up the 10% of the country it currently occupies.

Nearly every one of these 5 points is a non-starter. And Iran knows it.

To understand the thinking here, we have to apply game theory.

A Mexican Standoff

In the classic Spaghetti Western The Good, The Bad, and The Ugly, there is a classic Mexican standoff near the end.

All three men in the standoff want the gold buried nearby. All are armed and deadly with their weapons. The scene’s tension is legendary. You don’t see filmmaking like this anymore.

I won’t spoil the ending for those of you who (somehow) haven’t seen this excellent movie. But these standoff scenes have become a cinematic staple for a reason.

Here is how Wikipedia defines a Mexican standoff:

“A Mexican standoff is a confrontation where no strategy exists that allows any party to achieve victory. Anyone initiating aggression might trigger their own demise. At the same time, the parties are unable to extract themselves from the situation without either negotiating a truce or suffering a loss, maintaining strategic tension until one of those three potential organic outcomes occurs or some outside force intervenes.”

This is essentially where we are with Iran. Everybody is armed to the teeth, staring each other down, wondering if there’s a resolution that doesn’t involve missiles, bombs, and drones.

With our current situation, however, the world economy hangs in the balance.

Last Man Standing

Early on during the conflict, the U.S. Navy allowed Iranian oil tankers to continue passing through the Strait of Hormuz and deliver their cargoes, mostly to China.

However, on April 13th, Trump ramped up the pressure with a blockade. A few Iranian ships have snuck through, but most are stuck.

Iranian oil is piling up in storage. They are likely close to reaching capacity. And when that storage is full, things get tricky for Iran.

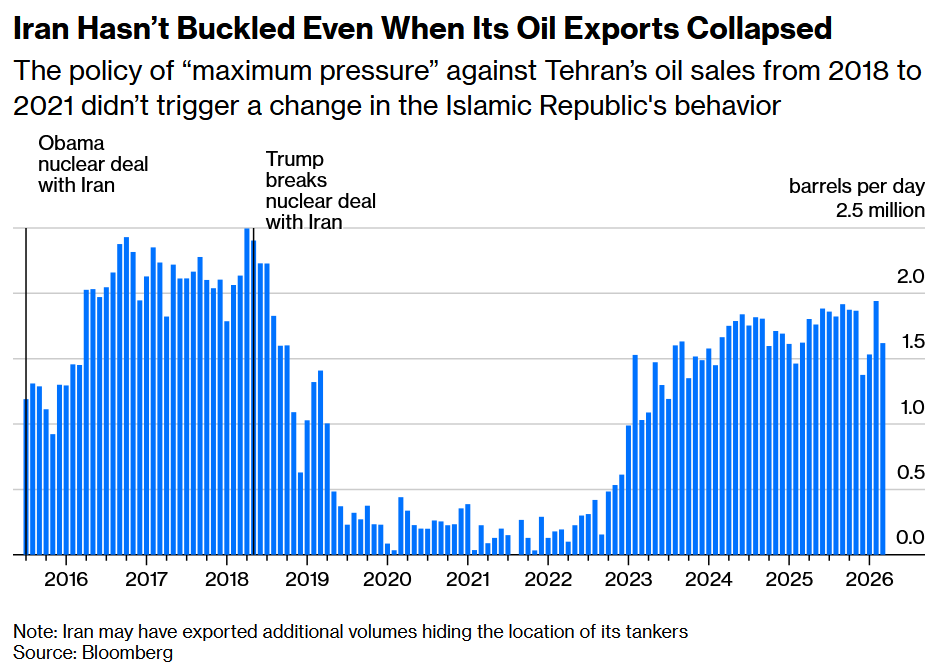

The country’s oil wells are particularly vulnerable to shut-ins (shutting down production). Stopping the flow can seriously damage the wells. We saw this during COVID, which combined with U.S. sanctions, crippled Iran’s oil exports for years:

This was an absolutely devastating blow for Iran. Oil is their biggest industry, by far. Their currency was annihilated, and it’s getting destroyed even worse today. But somehow they buckled down and weathered the storm from late 2019 to 2022.

The blockade is currently costing Iran about $500 million per day. That’s a massive hit. President Trump has also sanctioned Chinese oil refineries for processing Iranian crude, which was a big trade war escalation.

However, it sounds like he may back down on this matter after his recent visit to Beijing. China has essentially told the refineries to ignore the sanctions, which is the first time that’s happened. Another Mexican standoff.

President Trump is betting that Iran will break first. I’m not sure that’s a great bet. This is a country that’s been under harsh sanctions for 47 years, cut off from the world.

And like it or not, the current leadership remains firmly in charge.

Iran vs. The World Economy

I ran some numbers this morning, and it looks like so far, the world has spent about an extra $600 billion on oil, fertilizers, and liquefied natural gas (LNG).

The energy crisis is beginning to work its way through the global economy. Inflation is picking up, as we covered yesterday.

When the price of fuels, plastics, and fertilizers spike, it affects almost everything. And it’s really only just beginning.

Yields on government bonds around the world are spiking. Investors are demanding higher yields to account for higher inflation. This is a bad sign for a debt-bloated world.

So while Iran is under serious pressure, so are the rest of us. Americans are struggling with high energy and food prices, and don’t want another prolonged war in the Middle East.

Last Man Standing

Despite Iran’s economy being put in a vise, I don’t expect them to give in.

For them, this conflict is existential. So they’re willing to accept prolonged economic pain. Or even a return to war.

Are they bluffing? Perhaps. But it doesn’t seem like it. They are united with a certain religious and nationalist zealotry.

Can we say the same? Are we willing to restart the war, or let the Strait of Hormuz remain closed for another few months, or even the rest of 2026?

If Hormuz remains shut, the pain will quickly become extreme. And despite his threats to end Iran as a civilization, I don’t think Trump wants to restart the war. We were the party which asked for a ceasefire via Pakistan. And we know that Iran will strike back at Gulf oil infrastructure and further damage U.S. and Israeli targets in the region.

I hate to say it, but President Trump has painted himself into a corner. It’s a classic Mexican standoff. There are no good exit options.

At the beginning of this conflict, back on March 7th, Jim Rickards made a bold statement.

In a war of attrition, really a war for survival, victory goes to the last man standing. That may be Iran.

At the time, almost nobody else was saying this. The U.S. appeared triumphant and unstoppable. He also predicted that U.S. munitions would become a problem, and they have. The March 7th piece, Jim Rickards’ Most Surprising Iran Takes, is worth a re-read today. He nailed it.

Exit Possibilities

President Trump wants to find an exit that can be spun as a win. Frankly, this is a longshot. So for now, the Mexican standoff will continue.

Eventually we may simply have to withdraw. It’s happened before. Vietnam, Afghanistan.

What that would look like isn’t exactly clear. Would all the U.S. bases in the Gulf be repaired and rebuilt? Even though they’re under threat from Iranian missiles and drones? If not, that’s a sea change in U.S. power projection in the region. If they are rebuilt, that’s going to be a rather expensive proposition, especially considering the new defensive measures which would be required.

Would the Strait of Hormuz remain under Iranian control? That’s another key consideration.

Ultimately, a deal remains the most likely outcome. But it could take years to reach a lasting agreement.

In the meantime the world economy will suffer. Somehow, stocks are just below fresh all-time highs. But I don’t see that lasting as this situation drags out.

This is why every past administration avoided a hot war with Iran. Now President Trump must find a way to salvage the situation. Even if that means making compromises.

If he can put aside his pride and make a deal, my respect for Trump will only rise. But it remains unlikely until the pain becomes unbearable. So buckle up.

https://dailyreckoning.com/a-mexican-standoff-with-iran/