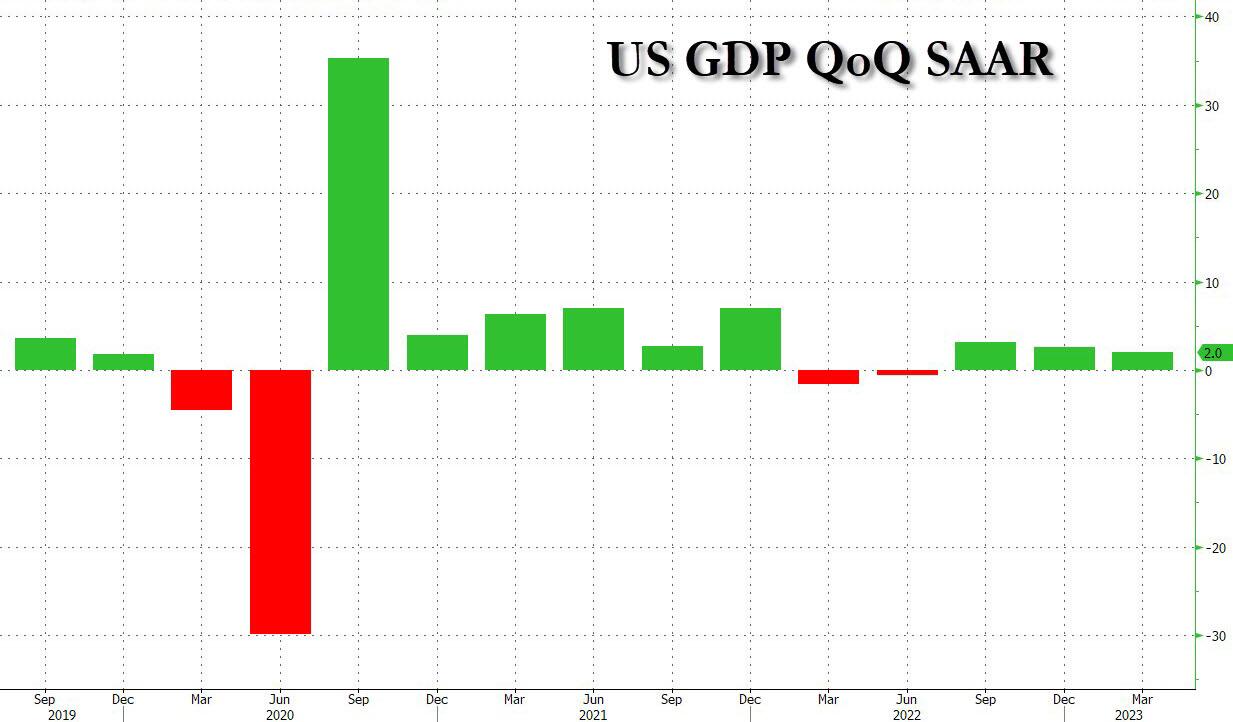

The second revision to Q1 GDP - data which comes some three months after the quarter in question is long over (and is still not the final revision as the data continues to be massaged higher or lower for years to come) - is usually a very boring affair: after all, the BEA is supposed to have all of the estimates and soft data replaced with hard actuals by now, and the bottom line number should be fine-tuned at best to the tune of 0.1%, 0.2% at most.

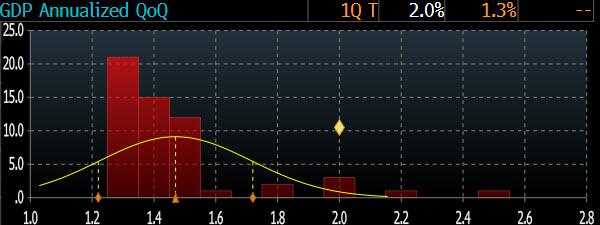

Not this time: moments ago, the BEA reported that according to the third estimate of Q1 GDP, the US economy grew much faster than expected at the start of the year, rising at a 2.0% SAAR, up dramatically from the 1.3% GDP print reported in the second estimate one month ago, and up almost 100% from the 1.1% initial Q1 GDP report published two months ago.

More importantly, the number was a two-sigma beat to consensus expectations of a 1.4% increase, the biggest outlier to the third GDP estimate in over a decade, a testament to how unexpected today's beat was.

The GDP estimate for the first quarter was revised up 0.7 percentage point from the “second” estimate, primarily reflecting upward revisions to exports and consumer spending.

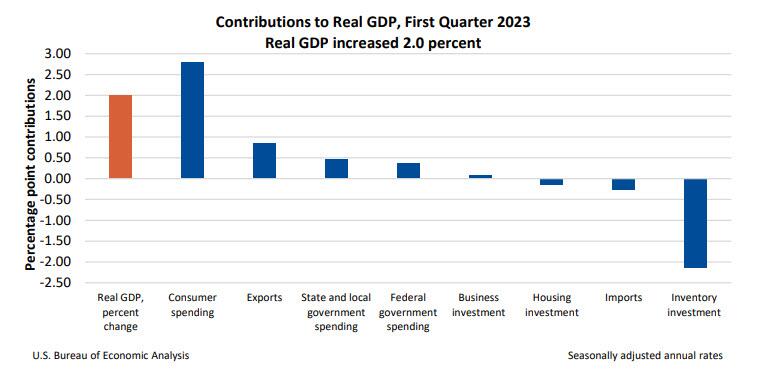

The increase in the first quarter primarily reflected an increase in consumer spending that was partly offset by a decrease in inventory investment.

- The increase in consumer spending reflected increases in both goods (led by motor vehicles and parts) and services (led by health care, food services and accommodations, and “other” services).

- The decrease in inventory investment primarily reflected decreases in wholesale trade and manufacturing.

Looking at the bottom-line contributors we get the following breakdown:

- Personal Consumption: 2.79% of the bottom line number, up from 2.52% in the second estimate.

- Fixed Investment: down modestly to -0.08% from -0.03%

- Change in private investment was unchanged at -2.14% of the bottom line GDP print.

- Net trade was the biggest change: exports were revised from 0.58% to 0.86%, while imports subtracted only -0.28% from the bottom line GDP, a big drop from the -0.57% subtraction previously. In total, net trade became a 0.58% contributor to growth, up from a tiny 0.01% booster in the latest revision, effectively responsible for almost all of the 1.3% to 2.0% GDP increase.

- Finally, government consumption was almost unchanged at 0.85%, down from 0.89%.

It was not immediately clear what was the source of this dramatic trade data revision.

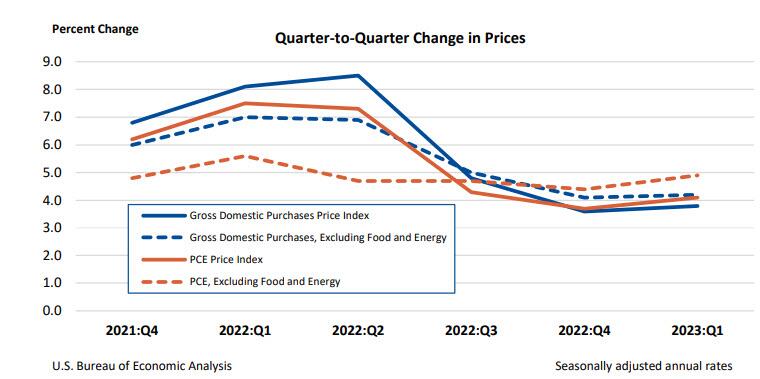

Elsewhere, while very much irrelevant now that we are about to enter July and the second half of the year, the report also revealed that according to the BEA, the GDP price index rose 4.1%, below the 4.2% expected, but up from 3.8% in the previous estimate. Core PCE also rose less than expected, up 4.9% vs exp. 5.0%.

While today's number is irrelevant for markets and the bigger picture, what is curious is how aggressive the upward data revision was. And as such, it suggests that the BEA's bean counters have far less "fudge" space to make Q2 and Q3 GDP look stronger, as such don't be surprised to find GDP in the current and next quarters come in well weaker than expected, which is key since many analysts expect the recession to start some time this summer.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.