Wednesday, June 15, 2022

Aquestive: Positive Initial Topline Data in Trial Evaluating AQST-109 Epinephrine Oral Film

AQST-109 is the first and only orally delivered epinephrine product candidate in clinical development

Fastest median time to maximum concentration (Tmax) in studies to date at 12 minutes

Study continues to show AQST-109 is safe and well tolerated

Head-to-head comparison study to EpiPen® scheduled to commence in third quarter 2022

On track to request End-of-Phase 2 meeting with FDA in fourth quarter 2022 and thereafter to commence pivotal PK study

Remaining data from Part 3 expected to be reported in early third quarter 2022

New authorized Roche COVID-19 test can also detect viral loads

Roche announced today that it received FDA emergency use authorization (EUA) for its cobas SARS-CoV-2 Duo diagnostic.

Authorization covers the cobas SARS-CoV-2 Duo on the fully automated cobas 6800/8800 systems, expanding Roche’s COVID-19 portfolio and representing the first automated, RT-PCR assay for the in vitro qualitative and quantitative detection of SARS-CoV-2 RNA in nasal and nasopharyngeal swab specimens.

The assay performs quantitation of SARS-CoV-2 RNA levels in the connected specimen, while only the qualitative result of cobas SARS-CoV-2 Duo is intended for use as an aid in the diagnosis of SARS-CoV-2 infection in patients suspected of COVID-19 by their healthcare provider.

Basel, Switzerland-based Roche said in a news release that the potential benefits from reporting a standard viral load along with the qualitative result may help clinicians assess and monitor infected patients across laboratories over time.

The company plans to make the test available in the U.S. by the second quarter of 2022.

“With the SARS-CoV-2 Duo test, we are now able to detect the COVID-19 virus and simultaneously measure the viral load in an individual,” Roche Diagnostics CEO Thomas Schinecker said in the release. “The test’s performance suggests that, by earlier and more accurately identifying infected patients, the results may open the path for healthcare providers to more efficiently organize their therapeutic and monitoring interventions.”

Optinose Stock Moves Higher On Positive Second Chronic Sinusitis Phase 3 Trial

Optinose Inc (NASDAQ: OPTN) announced the statistically significant benefits of XHANCE in the ReOpen2 trial for the symptoms co-primary endpoint and the CT scan co-primary endpoint.

Significant improvement was seen in patients with chronic sinusitis who did not have nasal polyps treated with both doses of XHANCE (fluticasone propionate) nasal spray compared to a vehicle Exhalation Delivery System (placebo).

The co-primary endpoints were a patient-reported composite symptom score measured at week 4 and an objective measure of disease in the sinus cavities at week 24.

The safety profile and tolerability of XHANCE in this trial were generally consistent with its currently labeled safety profile.

When pre-planned analyses are completed, detailed results from ReOpen2 will be submitted for publication in a peer-reviewed journal and presented at future medical meetings.

Could Retail Bagholders Spark A Rally 'Smart Money' Will Be Forced To Chase?

by Charles Hugh Smith via OfTwoMinds blog,

There would be some deliciously karmic justice if the "dumb money" driving a rally that forced the "smart money" to cover their shorts and chase the rally that shouldn't even be happening.

Being cursed with contrarianism, as soon as a trade gets crowded and the consensus is one way, I start looking for whatever is considered so unlikely that it's essentially "impossible." Sorry, I can't help myself.

The crowded trades are 1) long the Commodity Super-Cycle and 2) long hurricane-force recession for all the persuasive reasons we all know: global scarcities, geopolitical tensions, soaring US dollar and interest rates, de-risking, crazy-stupid levels of debt and speculation, etc.

The consensus holds that "Smart Money" rotated out of tech stocks and other over-valued equities into oil and commodities. That was a smart move, indeed, and the earlier one rotated out of equities and into commodities, the smarter the trade.

In this scenario, retail owners of equities are the "Bagholders," those who continue owning the losers all the way to the bottom (Been there and done that). It's a market truism that Bull cycles only end when retail drinks the speculative Kool-Aid of the moment and buys into the final gasp of the rally, allowing "Smart Money" to distribute their shares to the retail chumps, who go down with the ship when the market finally rolls over.

2022 has followed that script closely: as markets have been crushed, down 20% to 35%, and Wall Street sentiment is extremely bearish, retail owners haven't followed hedge funds in liquidating equities.

In the Bagholder / Smart Money script, the market can now descend into a Bear Market as liquidity dries up and buyers vanish, leaving the Bagholders to absorb the mounting losses.

Maybe this script plays out, maybe not.

The contrarian has these observations:

1. Institutions haven't liquidated their positions in Apple and other Big Tech stalwarts just yet. There's been trimming around the edges and that's why these stocks have been pounded by selling. But liquidation? Not yet. These companies are still quasi-monopolies and still immensely profitable.

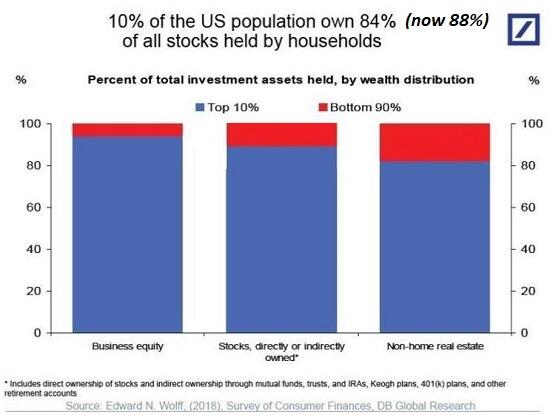

2. The mood on Wall Street might be extremely bearish ( The Mood On Wall Street Has Never Been More Apocalyptic), but the top 10% of households who own roughly 90% of financial assets may not be as close to panic as many seem to think. (Note that the majority of this wealth is held by the top 5%--the segment between 6% and 10% owns a relatively small slice of household wealth.)

A. Many of these households are old enough to have experienced the 2000-2003 Bear Market / dot-com collapse and the 2008-09 Global Financial Meltdown, a.k.a. Global Financial Crisis. They survived, and the take-away for many is that basic investment strategies weather downturns: avoid highly speculative fads (meme stocks, NFTs, iffy crypto schemes, etc.), diversify and patiently ride out the storm.

B. These households by and large did not speculate in meme stocks, NFTs, etc., so the staggering losses did not fall on them, or they limited their exposure to the degree that the losses were more painful to their self-image as savvy investors than to their total wealth.

C. Most of these households have multiple sources of income and stores of wealth. Even major drawdowns in equities don't threaten their financial security. Right or wrong, their experience is that even the gloomiest crises don't last.

D. Their gains are so stupendous even a 30% drawdown in every asset--real estate, stocks, bonds, precious metals-- still leaves much of their gains intact. For example, if the home you bought in the late 1990s for $200,000 is now worth in excess of $1 million, a 30% decline to $700,000 still leaves you up by $500,000.

E. Due to their earnings and range of assets, these households can add to investment positions in ways the bottom 90% cannot.

3. Commodities are priced on the margin, and a sharp decline in demand combined with a modest increase in supply could cascade into price declines that everyone who bought into the Commodity Super-Cycle do not believe are even possible, much less likely. But if supply drops 5% and demand plummets 10%, prices crash once the speculative hot air deflates the leveraged hot-money premium.

All this sets up the potential for "Bagholders" to "buy the dip" in stocks aggressively enough that "Smart Money" will be forced to cover their short positions and chase the rally. This will be frustrating to the "Smart Money:" don't those fools know we're heading into recession and they should panic-sell?

This will be frustrating for another reason: the entire point of distributing to Bagholders is to book profits and then wait for the Bagholders to sell at the bottom, in either panic or despair. Then the Smart Money scoops up the assets at bargain prices and awaits the re-entry of the burned-but- ever-greedy Bagholders.

There would be some deliciously karmic justice in the "dumb money" driving a rally that forced the "smart money" to cover their shorts and chase the rally that shouldn't even be happening, dang it. Stranger things have happened.

'Fed Painted Itself Into A Corner,' 'Triggered A Vicious Cycle'

With the Fed set to hike 75bps - with single-digit odds of a 100bps hike creeping in - some are getting euphoric and buying up risk assets on hopes the Fed will finally catch up to the curve and put inflation in its place. Not everyone agrees: as Wells Fargo senior equity analyst Chris Harvey writes in a Tuesday note in which he says that it is "Time to Close The Reopening Trade", Harvey writes that a "hard landing" has become his base case, and notes that "the recent pop in 2yr UST yields above 3% is our catalyst, indicating a more hawkish the Fed and continued risk aversion."

According to Harvey, "the recession starts in the markets since the economy has the highest equity beta in decades—i.e., the stock sell-off weighs on sentiment, then discretionary spending, and ultimately the economy." Some more thoughts on this markets-driven recession: "In 2020, the real economy (and Covid) brought the stock market to its knees. In 2022, it is the reverse: equities are in the process of bringing the economy down. "

The strategist then notes something else we have discussed, namely that while excess savings may have risen (even if they are clearly depleted for most households in light of the surge in credit card usage), this is more than offset by the trillions wiped out in the recent market crash.

And here is Harvey's take: "Investors acknowledge, but in our view do not fully appreciate, the US consumer's exposure to equities. According to Fed data, at the end of 2021 nearly one- quarter (24.3%) of US household assets were in equities. We viewed this as a major risk as a material, extended sell-off likely would impair sentiment and discretionary spending. We believe this vicious cycle has been triggered—and is complicated by the corner the Fed has painted itself into. We estimate US household assets could decline some $6T (4%) in 2Q22 due to the market selloff."

Which brings us to the punchline of Harvey's note: i) the Fed Mistake and ii) how the Fed painted itself into a corner:

Fed Mistake. The conventional wisdom is the Fed is about to make a monetary policy mistake. We disagree: the Fed already has erred by sustaining QE from June 2021 until March 2022. The Fed continued to buy $80B of Treasuries + $40B of MBS monthly regardless of price, liquidity or any other market condition even as the economy was quickly recovering and consumer spending was rebounding sharply. This predictably created market inefficiencies and mis-allocations of capital.

Last year we discussed this cost-of-capital subsidy and its knock-on effects. In simple terms, this created one of the biggest duration mispricings we have even seen. The reversal in 2022 is helping to roil not just US capital markets but also global bourses, with free markets (not the Fed) deciding the proper cost of capital. In 2021, the Fed's crowding out effect from QE drove real rates to historically negative levels that boosted the housing market, indirectly placed pressure on the supply chain, aided inflation, provided an unnecessary incentive to consumer spending, and helped spur speculation (TINA/There Is No Alternative).

The Fed indicated that only in hindsight could it have seen the inflation now upon us. This rings hollow to those of us with kids in high school; we are all-too-familiar with explanations why they did not begin their term projects early enough—and only see the error of their ways after it's too late.

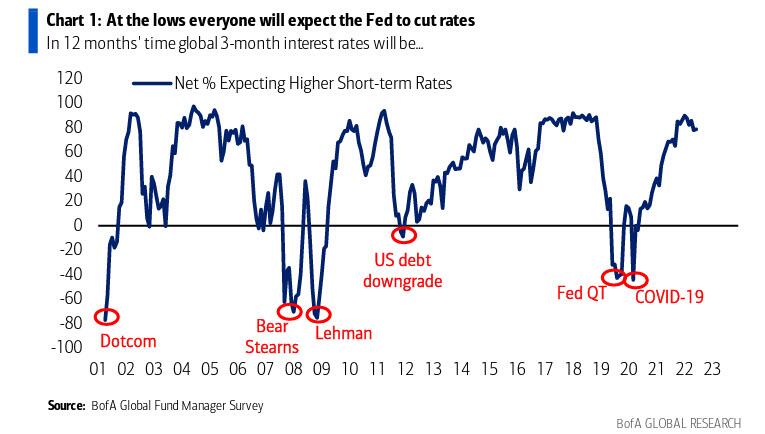

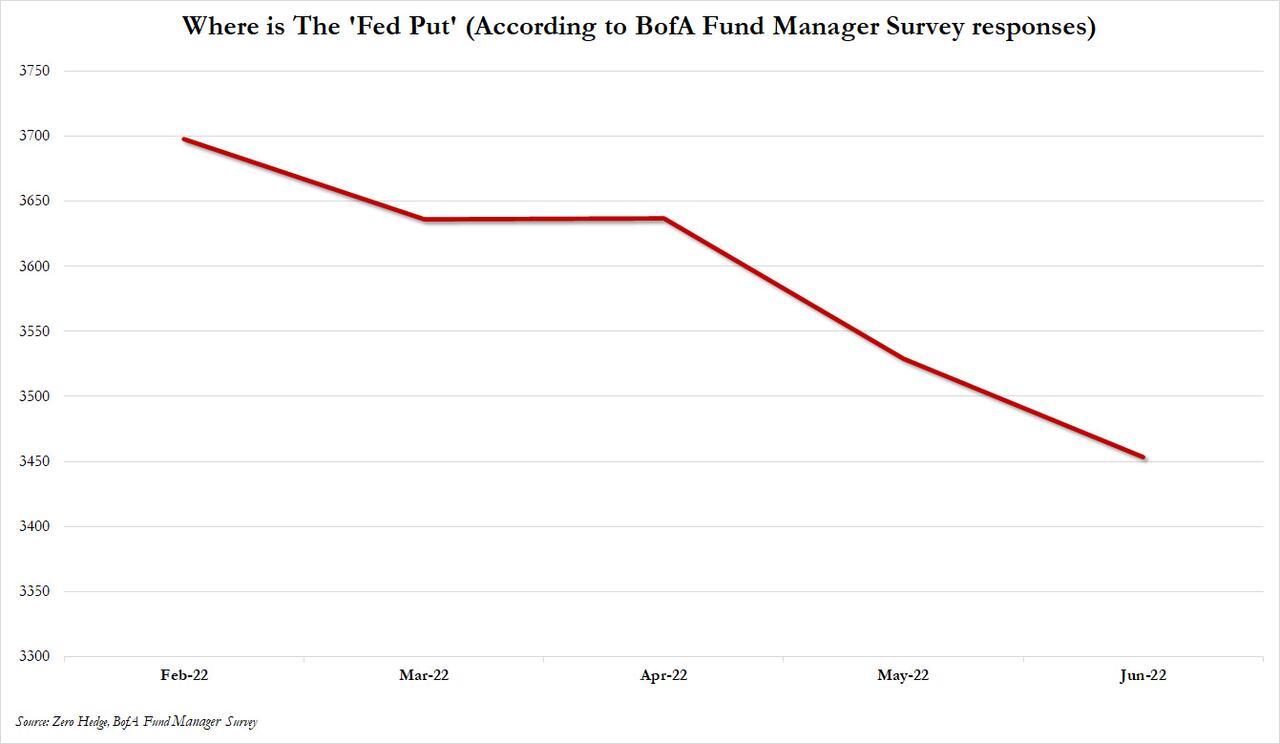

Finally, here is why Harvey thinks the Fed is now painted into a corner: "We believe the "Fed put" will not be triggered anytime soon and the economy has a higher equity beta than any time in decades. This suggests monetary policy will continue to weigh on risk products, and equity markets will lead us into recession. Once in recession, we would expect a quick turn toward easing. For equities, this would mean more volatility, a better bid for risk-aversion, and a decay of cyclicality until the easing cycle begins."

This is in line with the monthly Fund Manager Survey which has seen the consensus strike price of the "Fed Put" slide month after month, and is always below the current market level - for obvious reasons - because as we continue to slide and the Fed does nothing, all one has left is hope...

Before we go, here - as an added bonus - is Harvey's view on when we may finally bottom:

We are not looking for a level, but rather an event (or events) to stabilize equities. Stocks likely will find a bottom when the market believes Fed hikes will begin to decelerate. To get there, we will need to see jobless claims numbers continue to rise, suggesting supply/demand is better aligning and breakevens continue to decline (implying inflation expectations are abating). We believe this is still off in the distance. The relative performance of the Low Vol Index (see front page margin), as well as historically-low weights for defenses sectors, indicate the run toward risk aversion is not over.

Another way of putting this: we will bottom when everyone expects the Fed to be cutting rates. We are clearly not there yet...