Former Stanford University President Marc Tessier-Lavigne, who resigned in July of last year after an investigation found flaws in his research, retracted a 2009 science paper formerly described as “groundbreaking.”

The prestigious science journal Nature announced the retraction in a December 18 article signed by Tessier-Lavigne (pictured below), the lead author, and his three co-authors, The Stanford Dailyreported.

In 2009, Tessier-Lavigne, a neuroscientist, was an executive at the biotechnology company Genentech, according to The Daily.

Two days after the paper’s publication, Genentech described it to its shareholders as “groundbreaking basic research about an entirely new way of looking at the cause of Alzheimer’s disease.”

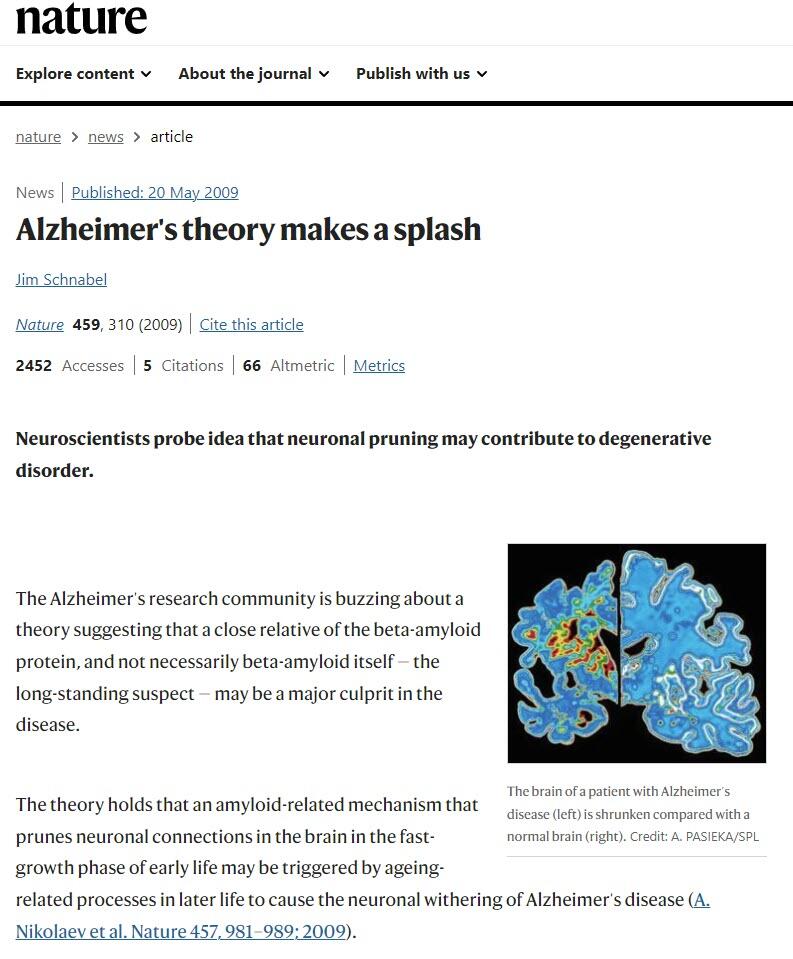

A Naturearticle published about the paper shortly after was titled, “Alzheimer’s theory makes a splash.”

Tessier-Lavigne told The Daily, “As with all of my papers, at the time of publication of Nature 2009, I believed the results in the paper were correct and accurately presented.”

“I absolutely believe that there are no falsified data in the paper,” he told The Daily in a subsequent email, it reported.

The retraction is Tessier-Lavigne’s fourth in four months, according to The Daily.

Such incidents are rare, as just eight out of every 10,000 science papers are retracted, according to Retraction Watch.

The Daily reported that “two of Tessier-Lavigne’s influential neurodevelopment papers published in Science and a third published in Cell were withdrawn earlier this fall after they were found to contain manipulated images.”

“Another Tessier-Lavigne paper published in Nature was issued an expression of concern over ‘manipulation of research data’ this month, implying it will likely face correction or retraction,” according to the paper.

The investigation leading to the former president’s resignation in July determined data “were manipulated in some published scientific papers on which he was a main contributor,”according to The Wall Street Journal.

An investigative panel also stated Tessier-Lavigne “failed to decisively correct mistakes in published papers as they were uncovered and had lapses in oversight of his labs at multiple institutions,” the outlet reported.

Given Donald Trump's absolute dominance over the current 2024 GOP field, Vivek Ramaswamy has a prediction:

Nikki Haley will become the establishment's 'puppet' candidate, and Ron DeSantis will be forced to join her ticket as VP.

"Here’s the plot: 1. Narrow this to a 2-horse race between Trump & a puppet they can control. 2. Eliminate Trump. 3. Trot their puppet into the White House. Prediction: next up, Ron DeSantis joins Nikki Haley’s ticket as VP. Ron may not know it yet, but he won’t have a say in the matter," Ramaswamy posted on X.

Of course, Chris Christie thinks Haley is 'gonna get smoked' because 'she's not up to this,' but we digress.

Haley and DeSantis take shots at Trump

On Wednesday, and we don't blame you if you missed it, Haley and DeSantis took shots at the former president (and each other) at a debate hosted by CNN in Des Moines, Iowa - after two other contenders, Gov. Asa Hutchinson and Vivek Ramaswamy, failed to meet the heightened requirements to participate.

At the start of the debate, Mr. DeSantis said—as he often has—that the former president is “running to pursue his issues.” Ms. Haley soon said that she doesn’t think the 45th president “is the right president to go forward,” touting herself as “a new generational leader.”

Mr. Tapper, one of CNN’s moderators, noted that President Trump had not accepted their invitation to take part in the pre-caucus debate. The former leader of the United States instead held a town hall elsewhere in Des Moines that aired on Fox News.

DeSantis tried to capitalize on his comments via X following the debate.

Haley, meanwhile, is right on course to piss off the more than 1/3 of US adults who say the 2020 election was illegitimate.

"That election—Trump lost it [and] Biden won that election," said Haley, adding that Trump would "have to answer" for Jan. 6, without specifying what she meant.

Haley and DeSantis also slammed Trump's claim of presidential immunity in a DC federal appeals court considering his 2020 election case, with DeSantis saying: "I think the D.C. circuit is going to rule against Trump on that issue," and that "a stacked, left-wing D.C. jury of all Democrats" is going to give Trump the business.

Haley suggested Trump's immunity argument is "absolutely ridiculous."

"What has President Trump done? You look at the last few years, and our country is completely divided," Haley said, apparently unaware that Trump hasn't been president 'the last few years.'

For a deeper dive into the Haley - DeSantis slap fight, the Daily Caller has a good writeup here.

Trump, meanwhile...

While Haley and DeSantis traded barbs, Trump sat down with Fox News hosts Bret Baier and Martha MacCalllum for a live town hall event, also in Iowa.

Joe Raedle/Getty Images

When asked by Baier about his plans for "retribution and looking backwards" during a second term, Trump said: "Well, first of all, a lot of people would say that’s not so bad," adding "Look, what they did: Russia, Russia, Russia hoax; the FBI/Twitter hoax; the 51 intelligence agents hoax – all of these different hoaxes that they did. You know, a lot of people would say that’s probably quite normal."

"I’m not going to have time for retribution," the former president continued. "We’re going to make this country so successful again, I’m not going to have time for retribution. And remember this: our ultimate retribution is success."

Trump has taken flack for March comments at CPAC, in which he told the crowd: "In 2016, I declared, ‘I am your voice.’ Today I add: I am your warrior, I am your justice, and for those that have been wronged and betrayed, I am your retribution. I am your retribution."

For well over two years, economists and analysts said rent was declining or soon would be. But for the 28th consecutive month rent and OER were up at least 0.4 percent.

Yet Another Groundhog Day for Rent

I repeat my core key theme for over two years now. People keep telling me rents are falling, I keep saying they aren’t. I thought this may finally be the month the rent trend breaks but it wasn’t.

Rent of primary residence, the cost that best equates to the rent people pay, jumped another 0.5 percent in November. Rent of primary residence has gone up at least 0.4 percent for 28 consecutive months! [Note: somewhere along the way I got off by a month. Last month I said 28 months but it is 28 months this month].

The “rents are falling” (or soon will) projections have been based on the price of new leases. But existing leases, more important, keep rising.

Only 8 to 9 percent of renters move each year. It’s been a huge mistake thinking new leases and finished construction would drive rent prices.

Moreover, some of the alleged declines failed to take in seasonal adjustments. Most people move between May and September. It’s harder to fill a lease in December pressuring rents in the winter.

Let’s tune into the BLS Report for the more details.

CPI Month-Over-Month Details

The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.3 percent in December on a seasonally adjusted basis, after rising 0.1 percent in November.

The index for shelter continued to rise in December, contributing over half of the monthly all items increase.

The energy index rose 0.4 percent over the month as increases in the electricity index and the gasoline index more than offset a decrease in the natural gas index.

The food index increased 0.2 percent in December, as it did in November. The index for food at home increased 0.1 percent over the month and the index for food away from home rose 0.3 percent.

The index for all items less food and energy rose 0.3 percent in December, the same monthly increase as in November.

Indexes which increased in December include shelter, motor vehicle insurance, and medical care. The index for household furnishings and operations and the index for personal care were among those that decreased over the month.

CPI Year-Over-Year

CPI Year-Over-Year Details

The all items index rose 3.4 percent for the 12 months ending December, a larger increase than the 3.1- percent increase for the 12 months ending November.

The all items less food and energy index rose 3.9 percent over the last 12 months, after rising 4.0 percent over the 12 months ending November.

The energy index decreased 2.0 percent for the 12 months ending December, while the food index increased 2.7 percent over the last year.

Rent of primary residence was up 6.5 percent outpacing wage increases.

Rent vs Owners’ Equivalent Rent

OER stands for Owners’ Equivalent Rent. It is the price people would pay to rent a house unfurnished, without utilities.

People keep repeating the myth that OER is based off the question “If someone were to rent your home today, how much do you think it would rent for monthly, unfurnished and without utilities?”

That is false. Rather, that silly question is used to help set CPI weights, not prices. Prices are real measured prices of rent.

Real Measured Prices

Based off minor imputations, some claim OER is not a “real price”.

However, imputations are so minor that the correct attitude is “So what?”

CPI Weights and Other Issues

Rather than bicker over the measured price of OER, the far bigger issue is weight. OER is the single largest component of the CPI with a weight of 26.018 percent as of December 2023. Rent of Primary Residence is 7.714 percent. Shelter comprises 35.170 percent.

Do people pay OER? No they don’t. That’s what’s “unreal”, not the measured price. Roughly 64 percent own their own home with 36 percent renting.

The people who own their own home do not pay rent, they pay a mortgage. Most refinanced at or near 3 percent.

Some economists want to strike OER from the CPI on this basis. The problem I have with this discussion is that “Inflation matters” not just “consumer inflation”. Thus home prices matter. Asset bubbles matter.

The 36 percent of the people who do rent have been royally screwed by Fed policy that inflated assets, especially home prices, in turn causing rents to soar.

The CPI is totally screwed up as a measure of inflation and ignoring OER does not address the issue.

Finally, I expect inflation to be sticker than the Fed believes because when the Fed slashed rates to zero and mortgage rates dropped to 3 percent those refinancing had extra money in their wallets every month going forward.

Why Predictions of When the Price of Rent Will Fall Have Been Wrong

I provide solid evidence that the BLS has been doing no such thing.

Nonetheless, assume inflation slows along with rent. At some point it’s bound to happen.

The key question then becomes: Was inflation transitory or is it the easing that’s transitory?

The extra money home owners have in their pockets, coupled with Biden’s regulations, the end of just-in-time manufacturing, and totally inane energy policy all suggest it’s the current easing of inflation that is transitory, not the initial spike.

Novartis has backed away from its pursuit of Cytokinetics, the Wall Street Journal reported on Thursday, citing sources.

Shares of Cytokinetics slumped over 25% on the news in afternoon trade.

The Swiss pharmaceutical giant's move came in the past day or two, the report said. Novartis or another suitor could re-emerge as Cytokinetics runs its sale process, it added.

On Monday, Reuters reported that Novartis is in the lead to acquire Cytokinetics, ahead of other bidders that include AstraZeneca and Johnson & Johnson.

Cytokinetics could also pursue another type of deal like a capital raise, the WSJ report said.

Both Novartis and Cytokinetics said they do not comment on market rumors and speculation.

Shares of Cytokinetics with a market capitalization of nearly $10 billion, as of Wednesday's closing price, have more than doubled in value since Oct. 31, when reports of the company attracting takeover interests first surfaced.

Ahead of its fourth quarter earnings next month, Oscar Health CEO Mark Bertolini expects 2024 to be a profitable year.

The insurtech recorded a $65.7 million net loss last quarter, but he expects the insurtech will reach 1.3 million members once open enrollment concludes this year, marking a 31% increase year-over-year.

Its long-term strategy, to be unveiled at investor day later this year, will focus heavily on individual coverage health reimbursement arrangements (ICHRA) in the next few years, with an intent to throw its hat into the Medicare Advantage ring beyond that.

"Our first market opportunity will be in ICHRA," he said. "We believe ICHRA's time has come. We believe we have a different approach than most other people in that marketplace that will give us an advantage in growth in 2024 and 2025."

The company's first goal is to hit 5% or better operating margin this year and then utilize ICHRA, a market that includes 70 million middle market and small group insured employers that Oscar Health believes could benefit from its offerings. Bertollini said ICHRA is a hedge for employers who are trying to rein in costs from inflation, presenting a growth opportunity for the company to show employers they can reduce their costs. He noted Oscar Health obtained 240 members in this year's enrollment out of ICHRA plans without offering a product.

Bertolini declined to give any projections on how many members the company could add through ICHRA offerings.

He also said that he thinks Oscar Health is well-positioned down the line to handle Medicare Advantage business.

"I sort of see Oscar Health as a pirate ship with cannons amid Spanish galleons filled with gold," he explained. "They're called big insurance companies who are not going to want to give up middle market and small group insured or Medicare Advantage."

He said he sees Oscar Health approaching providers who are dismayed and dropping Medicare Advantage plans by signing patients up to +Oscar, enabling them to provide private-label opportunities instead of selling through brokers. Oscar Health would set up quota share with providers as part of an agreement.

"Ultimately, we will get into the Medicare Advantage business, but that's a few years out, using our +Oscar Health platform with health systems in the market, by enabling them to provide private-label opportunities ... versus having to sell through brokers to the market," said Bertolini.

Atreca (NASDAQ:BCEL) stock is rising higher on Thursday following news of a major stake in the clinical-stage biopharmaceutical company from an investment advisor.

According to a filing with the U.S. Securities and Exchange Commission (SEC), Baker Bros. Advisors LP now holds a 19.9% stake in the company. This comes through a mix of Class A shares of BCEL stock and Class B shares that can be converted to Class A shares.

Atreca notes that the ability to convert Class B shares to Class A shares with a limitation of a 19.99% stake in the company will go into effect on Feb. 21, 2024. Prior to this, Baker Bros. Advisors LP was limited to holding a 4.99% stake in the company.

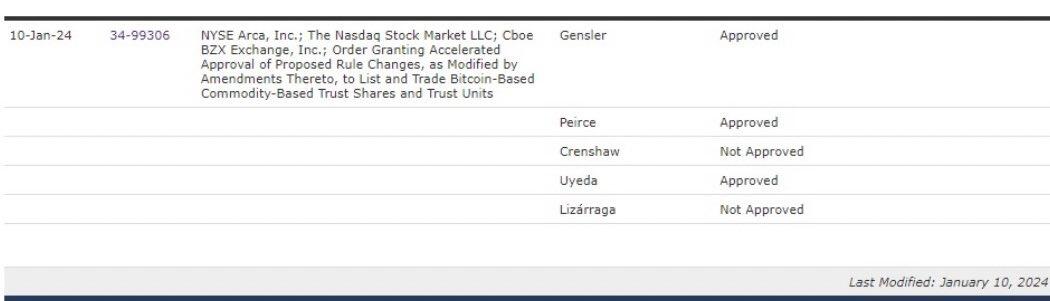

While Chair Gensler voted to approve the ETFs, he offered a personal statement worthy of the best cover-your-ass comment, warning that his decision in no way 'approves bitcoin' itself and that it's a very scary place for investors full of terrorists, money-launderers, and drug-traffickers.

“While we approved the listing and trading of certain spot Bitcoin ETP shares today, we did not approve or endorse Bitcoin,” Gensler wrote.

“Investors should remain cautious about the myriad risks associated with Bitcoin and products whose value is tied to crypto.”

Was Gensler genuflecting to Liz Warren in hopes of repentance?

His comments were not missed by ArkInvest's Cathie Wood:

“He just denigrated the whole crypto space. I couldn’t believe it,” Wood said in a Bloomberg Radio interview aired on X.

“This is par for the course in disruptive innovation.”

For some reason, the two Democratic SEC Commissioners chose to dissent, dis-approving of the ETFs...

Of course, their decision was not political at all - though they offered no rationale for their dissents.

Why would they be against the democratization?

Grzegorz Drozdz, market analyst for the European Union-based financial services platform Conotoxia commented that the general introduction of Bitcoin ETFs seems to have “significantly democratized” access to the market, “going beyond traditional cryptocurrency exchanges and wallets."

Ah yes that's why - because free-will and personal sovereignty are not part of the Marxist maxim preached from the left.

But it was Hester Peirce - so-called 'Crypto Mom' - that exposed the whole politcized farce in a wide-ranging rant statement after the vote.

Here it is in full (emphasis ours):

Today marks the end of an unnecessary, but consequential, saga. More than ten years after the filing of the first spot bitcoin exchange-traded product (“ETP”) application, the Commission finally has approved multiple applications by exchanges to allow the listing and trading of spot bitcoin ETPs. This saga likely would have spanned well beyond a decade were it not for the DC Circuit-ex-machina. You need not be a seasoned securities lawyer to spot the difference in treatment of bitcoin-related ETP applications compared to the many other ETP applications that have been routinely filed and approved over the past decade.

ETPs are an important innovation. Through them, investors can gain exposure to securities and non-securities, such as precious metals, in a convenient vehicle. Even if that exposure is available directly elsewhere, the ETP structure offers its own advantages. ETP shares trade continually on national stock exchanges at market prices, much as regular stocks do. By creating and redeeming shares of the fund, institutional traders, called authorized participants, help to maintain the price of these shares in line with the price of the assets in the investment pool. ETPs are accessible to investors and operate within the framework of the federal securities laws.

Since I became a Commissioner six years ago, one of the questions I have been asked most frequently is “When will the Commission approve a spot bitcoin ETP?” For reasons I have explained many times before, the logic of the long string of denials is perplexing. Predicting approval timelines for spot bitcoin ETPs was impossible because the review process for these filings did not resemble the fairly straightforward processes for approving comparable ETPs. The goalposts kept moving as the Commission slapped “DENIED” on application after application.

Bitcoin-based products have been trading for years under other regulatory regimes. In 2017, for example, the CME and the CBOE, which are regulated by the Commodity Futures Trading Commission, listed bitcoin futures. Foreign jurisdictions have long allowed spot bitcoin ETPs to trade. The Commission should have drawn comfort from the successful launch and smooth trading of these products, even through market stress and volatility. Instead, until today, the Commission remained steadfast in its unwillingness to let spot bitcoin ETPs into US markets.

In the meantime, the Commission has driven retail investors to less efficient means of attaining bitcoin exposure in the securities markets. For example, retail investors could hold it through non-exchange traded products or get some exposure by buying into companies or funds that owned or mined bitcoin. And, in 2021, bitcoin futures exchange-traded funds (“ETFs”), registered under the 1940 Act, started to trade given the Commission had no legal basis for stopping them. In 2022, the Commission approved the trading of bitcoin futures ETPs registered under the 1933 Act. These futures-based products are more complex and more difficult to manage than the spot product, which can translate into higher costs for investors. In any case, the Commission’s basis for letting these products trade should have been an equally compelling basis for letting spot products trade: the correlation between the bitcoin futures prices and the spot prices is high, which means that the regulated futures market is as relevant for a product based on spot bitcoin as it is for a fund investing in bitcoin futures. But, until a court reminded us that our “unexplained discounting of the obvious financial and mathematical relationship between the spot and futures markets falls short of the standard for reasoned decisionmaking,” we persisted in denying a spot bitcoin ETP.

The Commission, rather than admitting error, offers a weak explanation for its change of heart. In the past, the Commission, allowing our prejudice against the underlying asset to get in the way, has rejected applications on the basis that the bitcoin market was still immature and that there were outstanding manipulation concerns. Today’s approval order notes that the Commission now finds that means for “preventing fraud and manipulation” have been demonstrated because the prices on the CME bitcoin futures market and the spot bitcoin markets have been highly correlated throughout the past two-and-a-half years. We have denied multiple applications over that period, depriving investors of the opportunity to gain exposure to bitcoin in a more convenient and investor-friendly way. The only material change since we last denied a similar application was a judicial rebuke.

We squandered a decade of opportunities to do our job. If we had applied the standard we use for other commodity-based ETPs, we could have approved these products years ago, but we refused to do so until a court called our bluff. And even now our approval comes only begrudgingly, as demonstrated by our continued insistence that these products satisfy a correlation test we have not demanded of prior commodity-based ETPs. Perhaps the one silver lining here is now that we know that the Commission can execute a robust correlation analysis, perhaps the road to approving other spot crypto ETPs will not be as bumpy (even if the Commission insists on continuing to apply a test it applies nowhere else).

Today’s order does not undo the many harms created by the disparate treatment of spot bitcoin products.

First, our arbitrary and capricious treatment of applications in this area will continue to harm our reputation far beyond crypto. Diminished trust from the public will inhibit our ability to regulate the markets effectively. This saga will taint future interactions between the industry and our staff and will dampen the rich, informative dialogue that best protects investors.

Second, our disproportionate attention on these filings has diverted limited staff resources away from other mission critical work. Over ten years, likely millions of dollars of staff time has gone toward blocking these applications.

Third, our actions here have muddied people’s understanding of what the SEC’s role is. Congress did not authorize us to tell people whether a particular investment is right for them, but we have abused administrative procedures to withhold investments that we do not like from the public.

Fourth, by failing to follow our normal standards and processes in considering spot bitcoin ETPs, we have created an artificial frenzy around them. Had these products come to market in the way other comparable products typically have, we would have avoided the circus atmosphere in which we now find ourselves.

Fifth, we have alienated a generation of product innovators within our space. Our unreasonable approach to these applications has signaled that regulatory prejudice against new products and services can lead us to sidestep the law and unreasonably delay product launches. The industry has logged hundreds of meetings, has filed submissions, withdrawals and amendments, and ultimately had to resort to a costly legal battle to get us to today.

Although this is a time for reflection, it is also a time for celebration. I am not celebrating bitcoin or bitcoin-related products; what one regulator thinks about bitcoin is irrelevant. I am celebrating the right of American investors to express their thoughts on bitcoin by buying and selling spot bitcoin ETPs. And I am celebrating the perseverance of market participants in trying to bring to market a product they think investors want. I commend applicants’ decade-long persistence in the face of the Commission’s obstruction.

Roughly translated, her message is clear...

Weaponizing agencies? Politcized decision-making?

The 'people' seems happy as Bitcoin tops $49,000 and Ethereum rallies near $2700...

Source: Bloomberg

Wood maybe said it best: “It’s the old DNA basically bashing the new DNA."

{kind=link}