|

|

| This week's gainers and losers |

| Up: Tower Semiconductor +29.84% : Investor appetite for semiconductor stocks shows no sign of fading, especially when companies deliver strong results. The U.S. company also announced contract wins totaling €1.3 million. Rocket Lab Corporation +18.3% : After reporting results last week, the company benefited from positive recommendations from Deutsche Bank and New Street. A recent insider share sale was not enough to derail the rally. Nebius Group +24.22% : A notable rebound. When it reported results, the U.S. group announced diluted earnings per share of $2.11, compared with a loss of $0.48 a year earlier. Lumen technologies +18.51% : Northline is the name the fiber specialist has given to its new low-latency optical route linking Seattle and Minneapolis. Another positive: Lumen and Qwest Corporation announced an extension of the early participation and withdrawal deadlines for their offers. Ford +8.77% : The U.S. automaker rallied after the official launch of Ford Energy, a subsidiary focused on battery storage systems for data centers and large industrial customers. The stock was also helped by a Morgan Stanley note valuing the new business at up to $10 billion, based on a target operating profit of about $588 million at full capacity, or 20 GWh a year. Philip Morris +10.89% : The U.S. tobacco company saw a clear rebound in investor interest after the FDA issued new guidance saying it would not prioritize enforcement action against nicotine pouches and vaping products whose premarket authorization applications have been accepted and are under review. The move removes much of the regulatory uncertainty that had weighed on ZYN Ultra and IQOS in the United States. Tate & Lyle +44.55% : The British food ingredients specialist surged after U.S.-based Ingredion made a cash takeover offer valuing the shares at 615 pence each, a 64% premium to the last closing price, against a backdrop of sustained weakness in the stock over the past year.Intertek +14.36% : The British testing, inspection and certification specialist jumped after its board said it was prepared to recommend EQT’s final offer of GBX 6,000 per share. This is the Swedish fund’s fourth sweetened bid, valuing the group at £9.4 billion. British American Tobacco +13.99% : The British tobacco giant benefited from a major regulatory reprieve in the United States. The FDA said it would deprioritize enforcement action against smoke-free products with accepted PMTA applications, significantly reducing the risk hanging over the Vuse and Velo brands. Morgan Stanley upgraded the stock to overweight, while Citi raised its price target to GBX 5,200. JBS -16.33% : The Brazilian meat processor listed in New York was hit by a double blow: weaker results and earnings per share that were more than halved. JP Morgan then downgraded the stock from buy to neutral. Morgan Stanley remains positive on the name but cut its price target to $19 from $20.50. Intel -12.93% : South Korea raised the prospect of a tax on AI-related stocks, sending the sector lower. After the Korean giants, Intel and SanDisk also came under pressure, with SanDisk further hurt by a $3.5 million insider share sale. Oklo -14.15% : A widening net loss is rarely a good sign. Oklo’s net loss again landed in negative territory, at $33.1 million, compared with analysts’ expectations for a $32.1 million loss. 3i Group -14.67% : The British private equity firm fell sharply after reporting annual results. The main concern is the trajectory of Action, its flagship holding, which represents 65.4% of a £31.8 billion portfolio, as growth slows and margins narrow. Burberry -12.27% : The British fashion house came under pressure after annual results showed revenue down 2%, despite an improvement in earnings driven by Joshua Schulman’s restructuring plan. The entire sector remains out of favor, with analysts at AlphaValue noting that “the highly uncertain geopolitical backdrop and persistently weak tourism-related demand continue to limit visibility.” Salvatore Ferragamo also fell sharply after lackluster figures. |

|

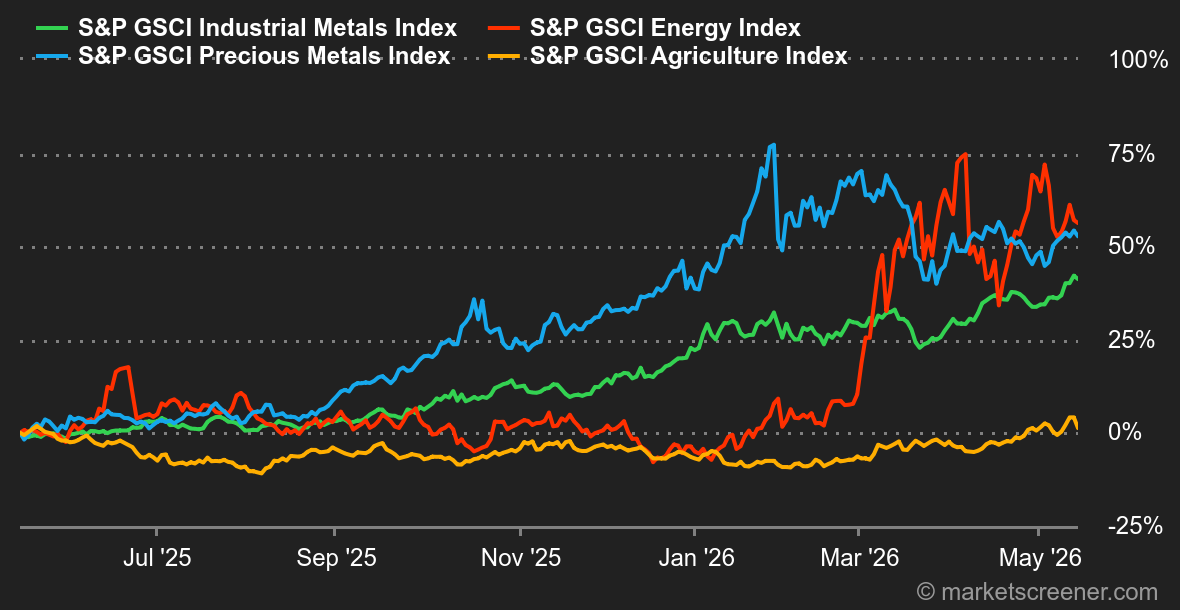

| Commodities |

Energy: Oil prices ended the week sharply higher. Brent rose nearly 4% to around $108 a barrel. U.S. WTI also advanced, moving above $100. The market reacted to ongoing disruptions in the Strait of Hormuz and a persistent global supply deficit. The meeting between Donald Trump and Xi Jinping in Beijing failed to break the deadlock over Iran. Both presidents agreed on the need to prevent Tehran from obtaining nuclear weapons and to reopen the Strait of Hormuz. The market hopes China will use its influence over Iran to help secure a peace deal, but no concrete progress emerged from the summit. On the ground, geopolitical risks remain high. Tight supply remains the main driver of higher prices. The International Energy Agency (IEA) estimates that global production fell by 1.8 million barrels per day (mb/d) in April. The latest OPEC report confirms the trend. The cartel’s production fell by 1.73 mb/d in April. The decline stems from export difficulties in the Persian Gulf and still includes volumes from the United Arab Emirates, which officially left OPEC on May 1. On 2026 demand, agencies are offering different scenarios. The IEA cut its forecast and now expects global demand to fall by 420,000 barrels per day, weighed down by aviation and petrochemicals. OPEC, by contrast, maintains a positive outlook and expects demand to grow by 1.17 mb/d. Metals: In London, copper topped $14,000 a metric ton this week before pulling back to around $13,938. As with oil, the rally was driven by supply-side concerns. Peru, the world’s third-largest producer, is facing production issues, raising the risk of a copper shortage given low global inventories. Demand, meanwhile, remains strong. The development of artificial intelligence requires the construction of many data centers, which use large amounts of copper. In precious metals, gold fell this week to $4,550. The U.S. economy continues to face persistent inflation. U.S. producer and consumer prices rose sharply in April, wiping out hopes for an interest-rate cut this year. High interest rates weigh on gold, as investors prefer assets that generate income. Agricultural products: Wheat posted the strongest weekly gain. The July 2026 contract rose 6% over the week to 650 cents a bushel. The increase was driven directly by the $A’s latest forecasts, which point to a weak wheat harvest. Soybeans reacted to U.S.-China trade talks and ended the week slightly lower, at 1,188 cents. Donald Trump expects China to make large soybean purchases, but price action suggests the market is tempering those expectations. |

|

| Macroeconomics |

Macro: The odds of a Fed rate hike appear to be rising by the day. According to the CME FedWatch tool, markets now see roughly a one-in-two chance that the Fed raises rates at least once by year-end. This week's inflation data, with both CPI and PPI above expectations, increased pressure on the Fed. The U.S. 10-year yield crossed 4.5% this week. The 2-year yield, generally seen as a proxy for expectations about the Fed's rate path, is at its highest level since last June. Back then, the Fed funds rate was 75 basis points higher. Finally, Jerome Powell's term as Fed chair ends this Friday. Kevin Warsh, confirmed by the Senate this week, will take over. Crypto: Bitcoin fell 2.2% this week and is once again flirting with $80,000. More broadly, alongside equity indexes, BTC has gained 17% since late March. But that still trails the Nasdaq 100, which is up 28% over the same period. The leading cryptocurrency had previously accustomed investors to magnifying moves in equity indexes, both up and down. This time, however, enthusiasm for the AI-semiconductor theme has largely overshadowed crypto. As a result, while investors once diversified by adding a bitcoin position to their portfolios, the trend now is to pile into anything that sounds like “semiconductor.” It is reminiscent of the period when simply adding the word “blockchain” to a press release was enough to send a stock soaring. This time, though, the use cases for AI are much more tangible than they were for blockchain. It may take tomorrow's AI agents adopting crypto use cases at scale before major inflows return to the cryptosphere. For now, other cryptocurrencies have followed bitcoin lower since Monday: ether (ETH) is down 4.8%, around $2,250; Solana (SOL) has fallen 5.5%, to $91; and XRP is flat at around $ 1.46. |

|

|

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.