BioMarin Pharmaceutical Inc (NASDAQ:BMRN) delivered strong second-quarter results on August 4, 2025, reporting double-digit revenue growth and significant profitability expansion across its rare disease portfolio. The company’s stock, which closed up 3.8% in regular trading, gained an additional 1.29% in after-hours trading following the earnings release.

Quarterly Performance Highlights

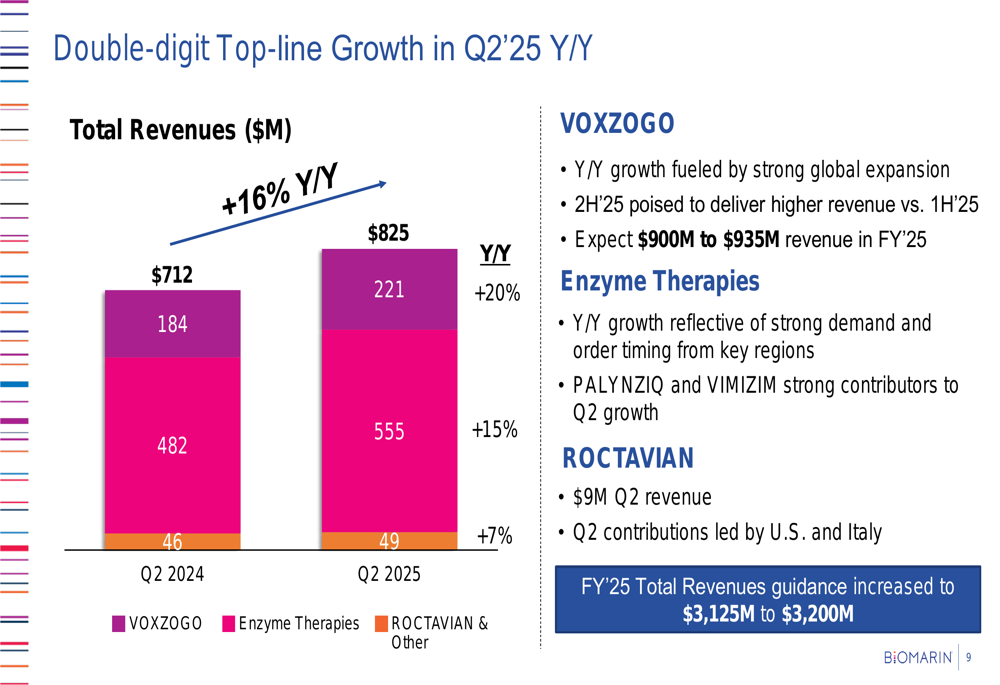

BioMarin reported total Q2 2025 revenues of $825 million, representing a 16% year-over-year increase from $712 million in Q2 2024. This growth was driven by strong performance across multiple products, particularly VOXZOGO, PALYNZIQ, and VIMIZIM.

As shown in the following chart of quarterly revenue growth:

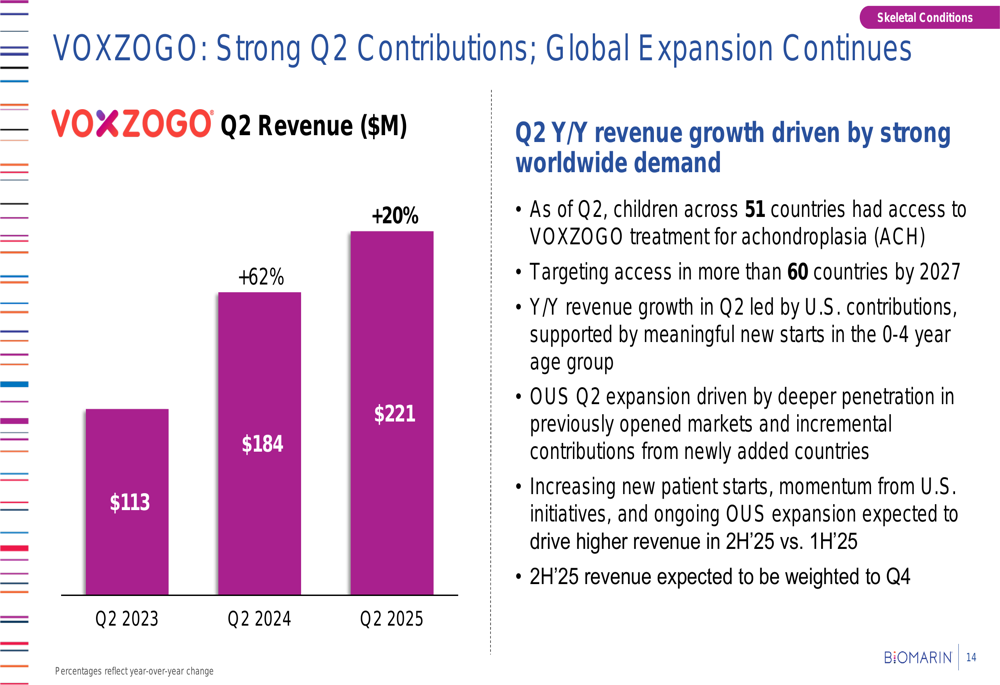

VOXZOGO, the company’s treatment for achondroplasia, continued its strong global expansion with Q2 revenue reaching $221 million, up 20% year-over-year. The company noted that children across 51 countries now have access to VOXZOGO treatment, with plans to expand to more than 60 countries by 2027.

The following chart illustrates VOXZOGO’s consistent growth trajectory:

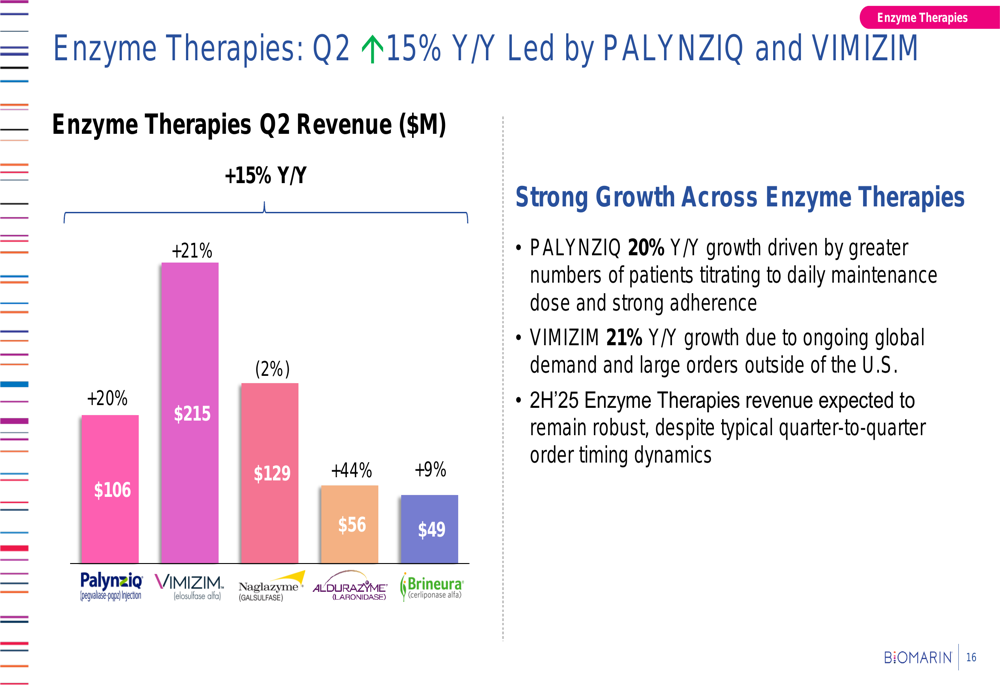

The Enzyme Therapies portfolio also performed well, with revenues increasing 15% year-over-year to $555 million. PALYNZIQ and VIMIZIM were particularly strong contributors, growing 20% and 21% respectively.

As shown in this breakdown of Enzyme Therapies revenue:

Detailed Financial Analysis

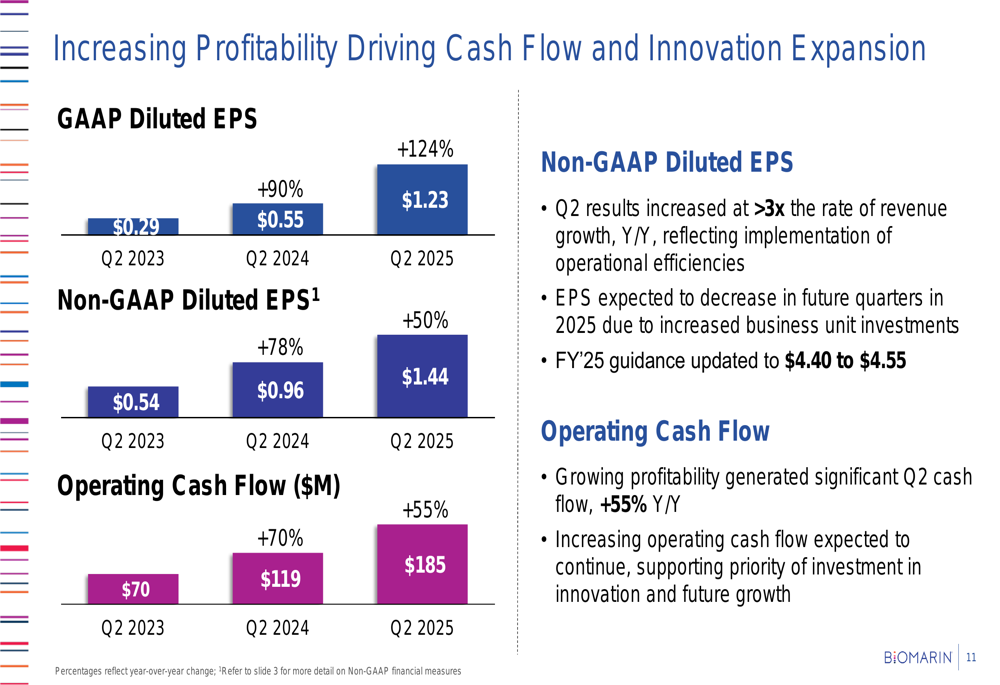

BioMarin’s profitability metrics showed substantial improvement in Q2 2025. GAAP operating margin expanded to 33.5%, an increase of 16.6 percentage points year-over-year, while non-GAAP operating margin reached 39.9%, up 8.7 percentage points.

GAAP diluted earnings per share more than doubled to $1.23, representing a 124% increase from $0.55 in Q2 2024. Non-GAAP diluted EPS grew 50% to $1.44. The company noted that EPS increased at more than three times the rate of revenue growth, reflecting successful implementation of operational efficiencies.

The following chart illustrates this dramatic profitability improvement:

Operating cash flow also showed robust growth, increasing 55% year-over-year to $185 million. This growing cash generation is expected to support the company’s investments in innovation and future growth.

Operating expenses showed disciplined management, with GAAP R&D and SG&A expenses both decreasing 12% year-over-year. The company attributed this to focused R&D investment following its 2024 strategic review. However, BioMarin expects operating expenses to increase in the second half of 2025 as clinical programs and commercial initiatives advance.

Pipeline and Strategic Initiatives

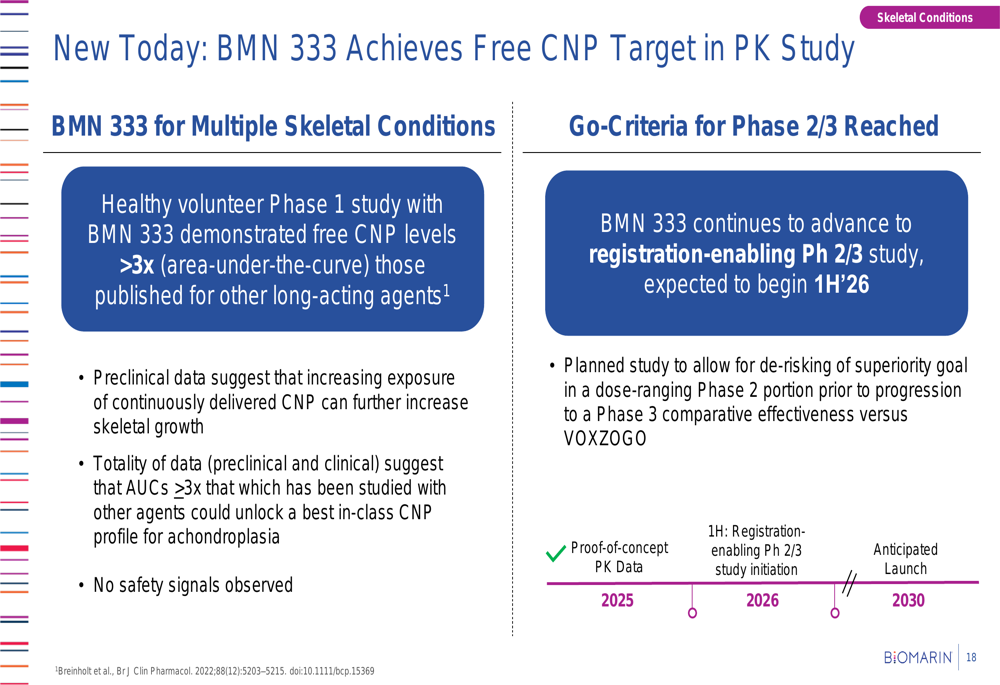

BioMarin highlighted several key pipeline developments during its presentation. The company announced that BMN 333, its treatment candidate for multiple skeletal conditions, achieved free CNP levels more than three times those published for other long-acting agents in a Phase 1 study, with no safety signals observed.

As shown in the following slide detailing the BMN 333 progress:

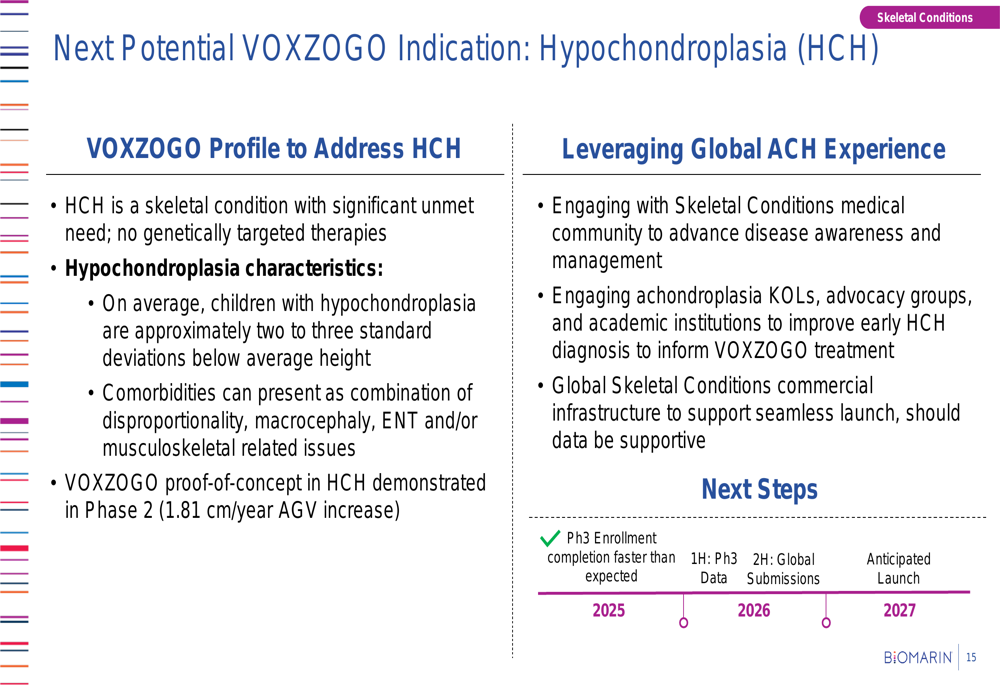

The company is also expanding VOXZOGO’s potential indications to include hypochondroplasia (HCH), a skeletal condition with significant unmet need. Phase 3 enrollment is expected to complete faster than anticipated in 2025, with global submissions planned for the second half of 2026 and potential launch in 2027.

The following timeline illustrates VOXZOGO’s development for HCH:

BioMarin completed the acquisition of Inozyme Pharma on July 1, 2025, adding BMN 401 (formerly INZ-701) to its Enzyme Therapies portfolio. BMN 401 is positioned as a potential first-in-disease treatment for ENPP1 Deficiency, with pivotal data expected in the first half of 2026 and potential launch in 2027.

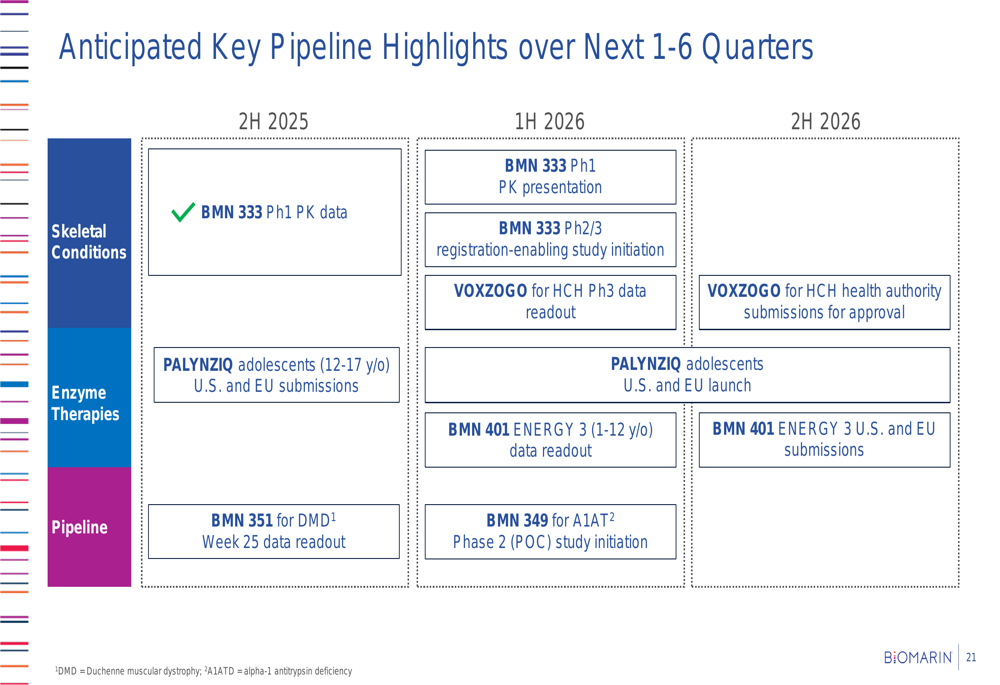

The company provided a comprehensive roadmap of anticipated pipeline milestones:

Updated Guidance and Outlook

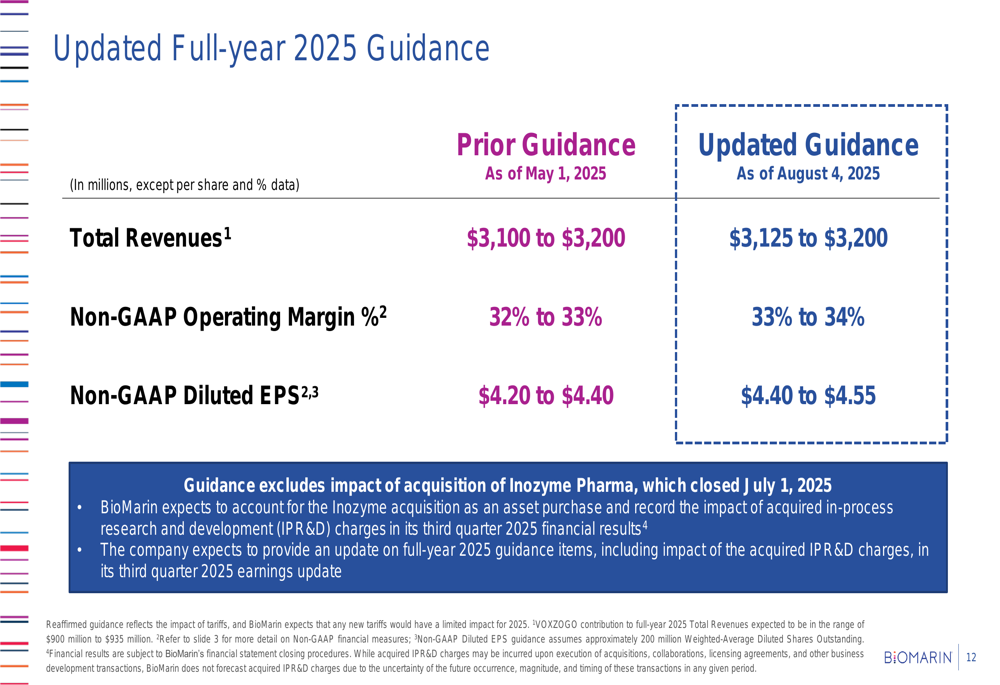

Based on its strong first-half performance, BioMarin updated its full-year 2025 guidance. The company narrowed its total revenue guidance to $3,125-$3,200 million, raised its non-GAAP operating margin guidance to 33-34% (from 32-33%), and increased its non-GAAP diluted EPS guidance to $4.40-$4.55 (from $4.20-$4.40).

The following slide details the updated guidance:

"We delivered strong Q2’25 revenue growth and significant profitability expansion driven by execution across the business," said Alexander Hardy, President and CEO of BioMarin. The company emphasized its focus on continued strong growth, progressing prioritized pipeline assets, and augmenting growth with business development opportunities in the second half of 2025.