- Jyong Biotech develops botanical drugs for urinary disorders. Their lead asset is clearly MCS‑2, which is currently restarting Phase 3 trials after a previous FDA setback.

- Their pipeline targets large unmet BPH, prostate cancer prevention, and IC markets. However, their botanical approach could be a potential “first‑in‑class” as a safer alternative.

- MENS recent IPO raised roughly $20 million and gave them a healthy cash runway. Though note that additional trials could accelerate cash burn.

- Still, I think their valuation and low trading volume make shares highly speculative. MENS would require a substantial revenue jump in the near term to justify its price tag.

- Hence, I reckon there’s some risk‑adjusted upside left in the long term. But for now, clinical trials, dilution, and liquidity risks keep my stance at a 'hold.'

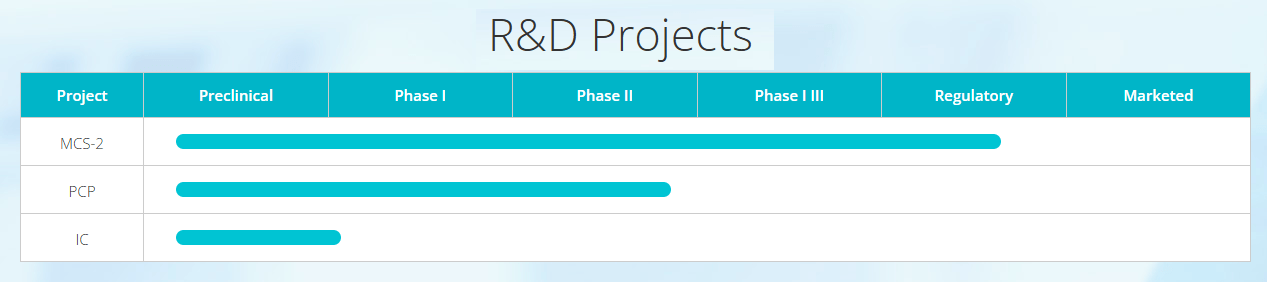

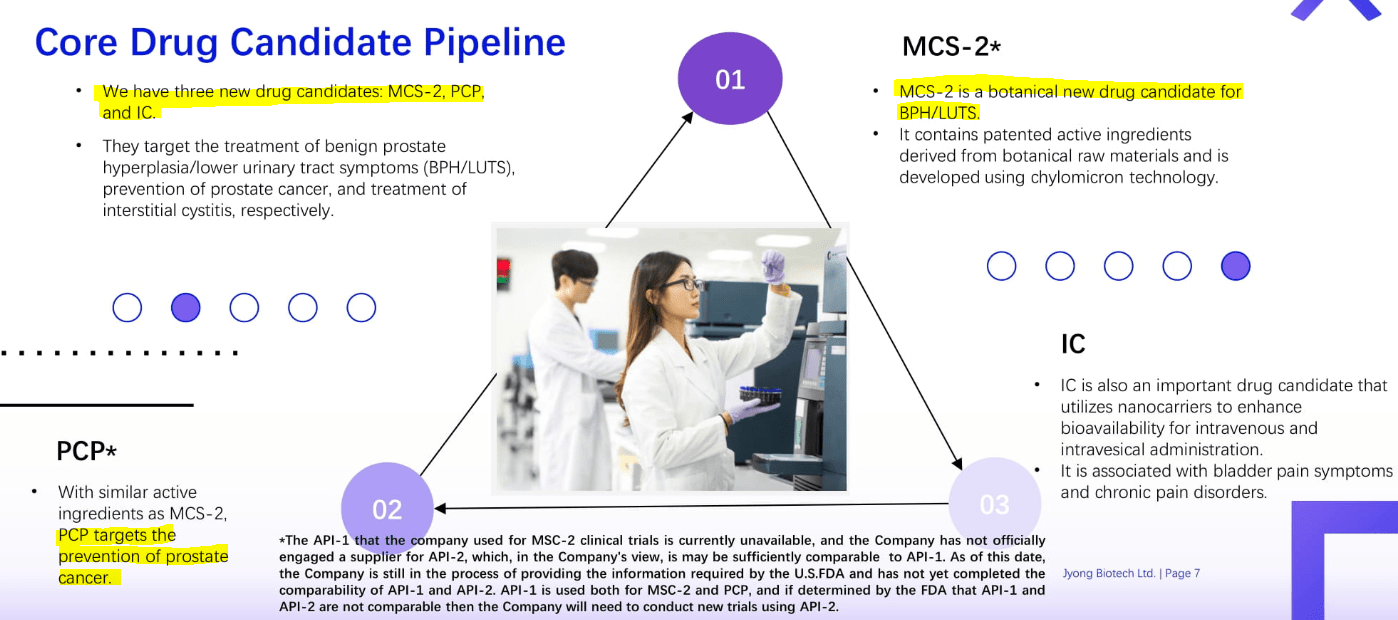

- Jyong Biotech Ltd. (MENS) is a clinical-stage biotechnology company developing botanical drugs for urinary system disorders. Their intention is to provide safer alternatives to conventional synthetic treatments. Currently, MENS’ pipeline includes MCS-2 for benign prostatic hyperplasia and lower urinary tract symptoms, PCP for prostate cancer prevention, and IC for interstitial cystitis. These candidates are in Phase 3, Phase 2, and preclinical stages, respectively. Similarly, MENS had an FDA setback, and it’s restarting its late-stage trials while pursuing licensing agreements. So, there are still substantial clinical trial risks embedded in MENS’ investment thesis. Likewise, I have some valuation concerns at these levels, and it’s also difficult to justify the stock’s low trading liquidity risks associated. Hence, I lean towards a “hold” rating for now, but worth adding to your watchlist.

Asian Biotech Play

Jyong Biotech is a biotech that works on plant-derived drugs for urinary system conditions. It’s actually incorporated in the Cayman Islands, and its IPO was recently on June 18, 2025. Today, they’re headquartered in New Taipei City, Taiwan. However, their global strategy depends heavily on forming international partnerships, and that remains a wildcard until we see the final terms on each deal. Essentially, they offer a botanical therapeutic alternative to traditional synthetic drugs, while attempting to secure global licensing deals. The idea is to eventually cover other markets across the US, EU, and Asia through partnerships. Yet, in the near term, their main focus remains on Taiwan and mainland China.

Source: MENS’ Subsidiary, Health Ever Bio‑Tech. Company Website. Retrieved July 23, 2025

But more importantly, I believe they target large and underserved markets, which is probably the stock’s main positive factor as it implies substantial upside potential. Additionally, their in-house manufacturing capabilities show they can scale rapidly once their IP reaches regulatory approval. Having said that, MENS operates through its five wholly owned subsidiaries. This includes Health Ever Bio‑Tech Co., Ltd. in Taiwan. Also, MENS’ Yilan Letzer Pharmaceutical Factory is authorized by the Taiwan Food and Drug Administration [TFDA] to conduct in-house manufacturing. And as I previously noted, this is a great variable in their favor, as it shows MENS can quickly ramp up production whenever one of its candidates obtains approval.

Pipeline Details And Regulatory Process

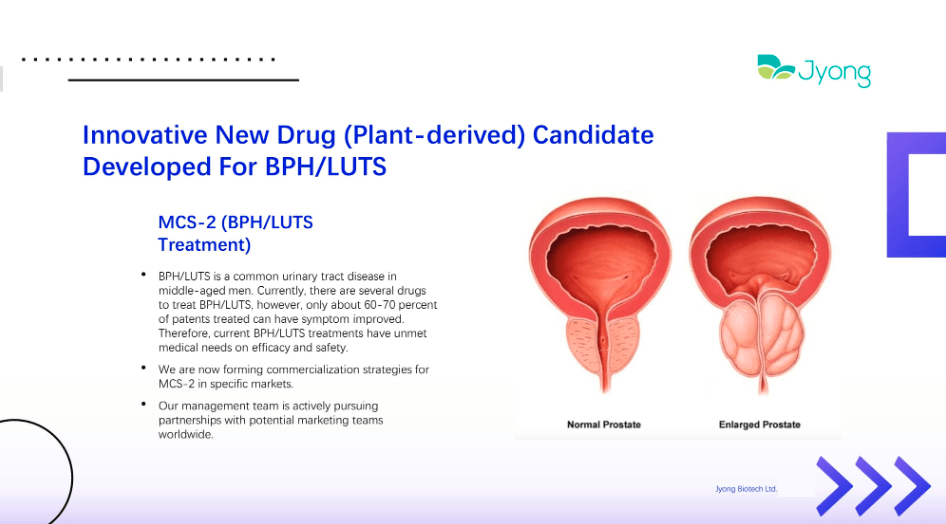

Furthermore, I believe MENS’ flagship drug candidate is MCS-2, a clinical-stage botanical medicine that targets benign prostatic hyperplasia [BPH] and lower urinary tract symptoms [LUTS]. MCS-2’s active ingredients are mainly fat-soluble compounds, which are absorbed and transported via chylomicrons. This is a particularly important feature since those are natural lipid particles formed in the human digestive system. In fact, chylomicrons transport MCS-2’s active ingredients from the intestines through the lymphatic system and into the bloodstream. And the main benefit from this approach is that it bypasses the hepatic first-pass metabolism.

Source: MENS’ Issuer Free Writing Prospectus. March 2025.

So far, we know that MCS-2 recently did an NDA resubmission to the FDA back in December 2021. However, that NDA was voluntarily withdrawn in 2022 after receiving FDA feedback on significant issues. That’s why MENS decided to restart its Phase 3 trials, but this time with a different active pharmaceutical ingredient [API]. And indeed, such a change of API requires new trials and results that corroborate its safety and efficiency.

This is where the recent IPO comes into play. You see, MENS plans to use those IPO proceeds to fund its additional Phase 3 trials. Naturally, it will also use part of the IPO’s proceeds to fund other earlier-stage trials. Management will test its candidates to compare its original API with the new one.

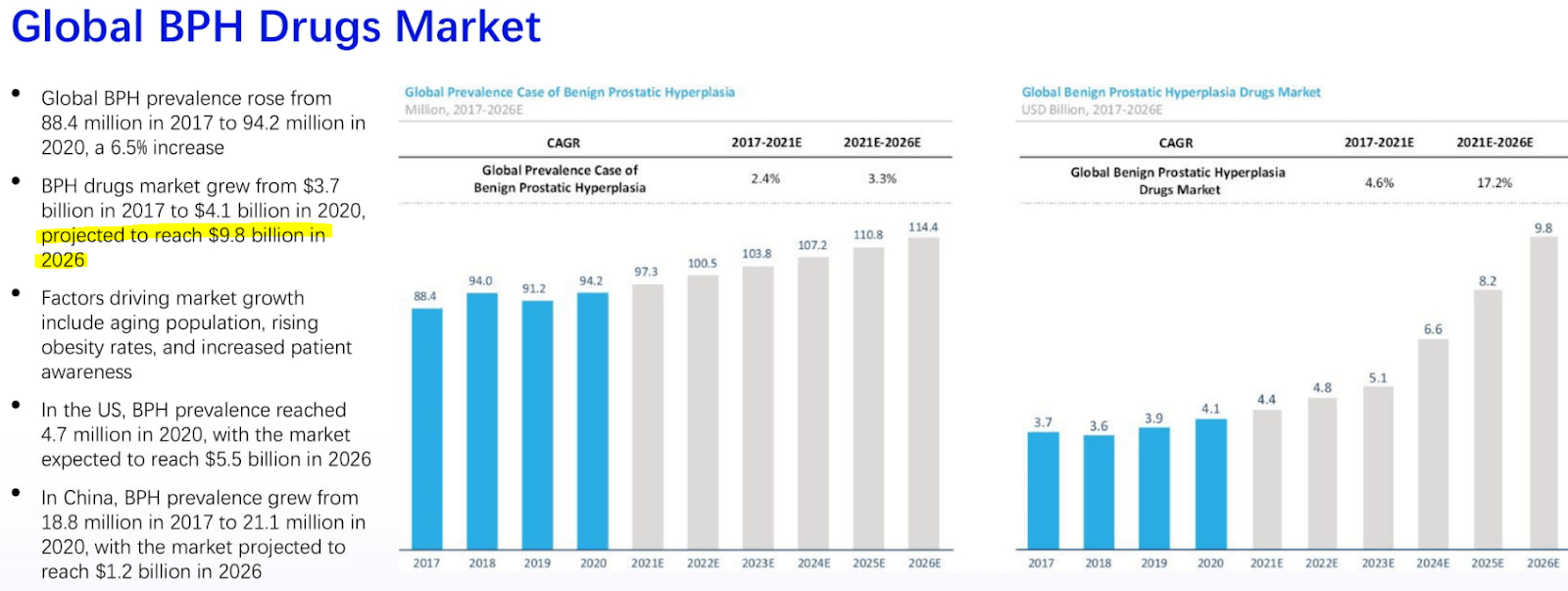

But in any event, MCS-2 targets a large unmet clinical need in BPH and LUTS. After all, this is a sizeable market as these conditions affect nearly one in two men over 50. Likewise, MENS has a nice strategic value within this niche because current therapies are synthetic and have many adverse effects. For example, alpha-blockers and 5-alpha reductase inhibitors sometimes cause dizziness, sexual dysfunction, and even hypotension. Thus, MENS’ opportunity in the BPH market is considerable, and this TAM is projected to grow to $9.8 billion by 2026.

Source: MENS’ Issuer Free Writing Prospectus. March 2025.

In my view, its second value driver is its other candidate, called PCP. This IP is currently in Phase 2 trials in Taiwan as a botanical medication indicated for prostate cancer prevention. This medication contains several patented APIs that reduce oxidative stress and cytokines, especially IL-6, which is a marker linked to inflammation and cancer. These biological effects are associated with reducing the risk of prostate cancer. So far, PCP’s Phase 2 studies have been ongoing since November 2014, involving 702 subjects across 20 medical centers. The company is looking for partnerships with international pharmaceutical firms to conduct multinational Phase 3 trials eventually as well.

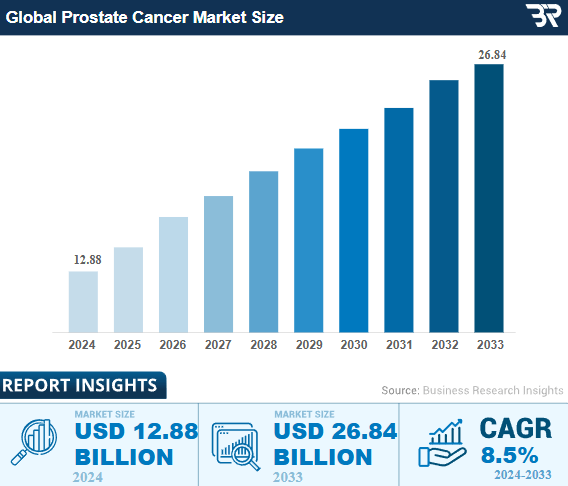

But the main opportunity here is that there are no FDA-approved drugs to prevent prostate cancer. Drugs like finasteride and dutasteride are used for prostate conditions like BPH. However, according to an FDA warning, these drugs may increase the risk of high-grade prostate cancer. In fact, those drugs can even cause side effects such as sexual dysfunction and skin reactions. In contrast, MENS’ botanical products may produce fewer negative effects than existing synthetic therapies. If successful, PCP could offer a first-in-class preventive solution and tap into a large market in oncology projected to reach $26.8 billion by 2033. Though, since PCP is in Phase 2, I imagine it should take longer to reach any regulatory approval than MENS’ leading candidate, MCS-2.

Source: Business Research Insights.

Lastly, MENS’ third drug candidate is IC. This is a medication in the preclinical stages that’s intended for interstitial cystitis and bladder pain syndrome [IC/BPS]. IC/BPS is a chronic and debilitating bladder condition. Thus, MENS’ IC uses nanocarriers for intravenous and intravesical administration. Nanocarriers are tiny particles designed to enhance drug delivery and absorption, aiming to improve efficacy and reduce side effects. The company is currently working on an initial Phase 1 trial planned in the near future in Taiwan. But overall, this still seems like a very early-stage R&D project, which is why I wouldn’t consider it a major value driver just yet.

Valuation And Risk Analysis

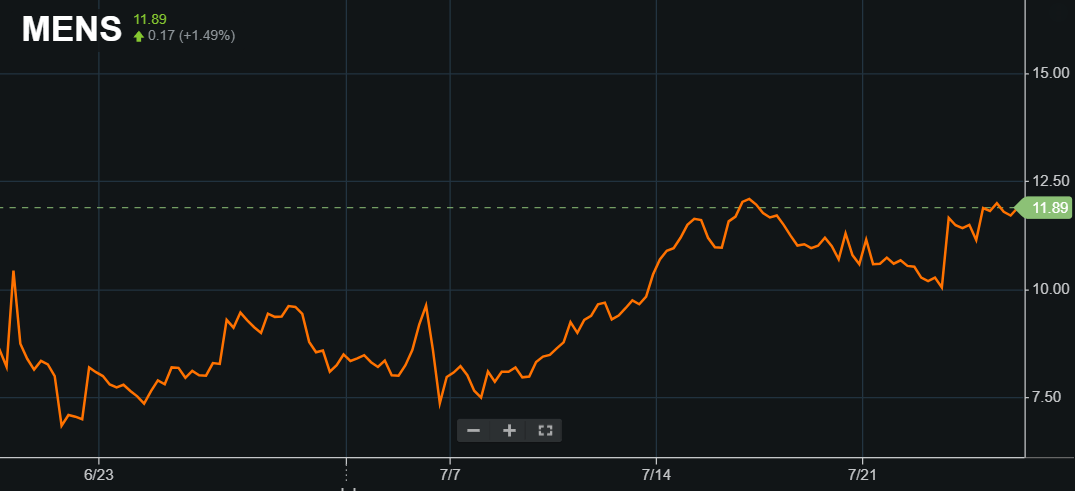

Now, from a valuation perspective, MENS’ IPO was priced at $7.50 per share and issued approximately 2.7 million shares. In total, the IPO’s gross proceeds were roughly $20.0 million. At first glance, it would seem the IPO was a success since the shares rapidly appreciated and have now settled around the $11.80 level per share. MENS’ market cap is now close to $827.7 million, which is also impressive given its underlying financials. After all, this is a pre-revenue biotech that still remains far away from having a commercially approved product.

Source: Seeking Alpha Charts.

In my opinion, even their leading candidate, MCS-2, is likely 1 or 2 years away from regulatory approval (at the earliest). Also, their latest financials are from December 2024, and their balance held only $98.0 thousand in cash, with a negative book value of $36.5 million. Naturally, that makes their 2025 IPO proceeds of $20.0 million the main source of liquidity. Similarly, I estimate their 2024 cash burn reached $3.6 million. Note that I got that figure by adding their cash flows from operations and CAPEX. That implies a cash runway of about 5.6 years.

Therefore, I do think this is a relatively healthy runway. Though I anticipate that if the FDA requires another Phase 3 trial on MCS-2, it would probably increase MENS’ burn rate even more, shortening this runway. But overall, I have to admit MENS’ valuation today seems a bit rich given its still highly speculative nature. They’re still relatively far away from commercializing any products, and even if they reach approval, any product launches will probably require even more capital. Thus, I think there’s a high likelihood of another capital raise in the future, even in the bull case scenario where MENS’ leading candidate, MCS-2, is approved within 1-2 years.

Also, remember that MENS’ peers trade at a forward P/S of 3.6. So, at MENS' current market cap of $827.7 million, they would require roughly $229.9 million in sales (within 1 or 2 years) to trade in line with the rest of its sector. And, in my view, that seems like a highly unlikely scenario, which probably hints at MENS being overvalued at these levels. However, I do concede they have a promising and potentially safer approach that could pay off in the long run.

Source: MENS’ Issuer Free Writing Prospectus. March 2025.

And on top of that, the stock itself has a razor-thin volume of about 60.0 thousand shares. At the current PPS of $11.80, that’s only $708.0 thousand in trading liquidity, which suggests even smaller buy/sell orders will push the price and create volatility. Hence, on balance, I lean towards a neutral rating for now, mostly because MCS-2 could potentially tap into a huge market in BPH eventually.

Conclusion: Pass For Now

Overall, I think MENS has an interesting and more natural approach to urinary system conditions. This could definitely find a favorable product-market fit if they reach FDA approval. However, even their leading candidate seems 1-2 years away from regulatory approval. Also, their stock appears quite expensive at these levels. So, while their cash runway derisks MENS’ investment thesis, I still think it’s not enough to warrant a bullish rating. Conversely, their underlying IP portfolio is indeed in late stages, which offsets my concerns to some extent. That’s why, on balance, I lean towards a neutral “Hold” rating for MENS at these levels.

This article was written by

Analyst’s Disclosure:I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.