by Adam Sharp

Using AI can be magical. It has helped me understand obscure investment concepts which aren’t covered well anywhere else.

It has shown my son exactly how to do a geometry problem, so I don’t have to relearn something forgotten 30 years ago.

AI has helped me understand legal contracts which previously would have required paying a lawyer hundreds of dollars per hour.

Magical.

At other times, it becomes painfully obvious that these models were trained on the NY Times, Washington Post, WEF white papers, Berkeley PhD theses, and other neoliberal mainstream garbage…

For example, as an experiment, I asked ChatGPT the following question:

I need help deciding how to invest the energy portion of my portfolio. Give me a breakdown of investing in oil and gas versus solar and wind. Which is a better bet for the long-term?

The AI proceeded to give a detailed breakdown of the pros and cons of each investment option. It even created this nifty table, just for me.

Hmmm, so the “return potential” for oil and gas is “moderate”, while for solar and wind it is “high”. The entire answer was skewed towards renewables. ChatGPT made it clear that wind and solar are the future, and oil and gas are the past.

So ChatGPT tells me that the potential returns in wind and solar are higher than oil and gas. It then recommends the iShares Global Clean Energy ETF (ICLN).

Well, I looked up the ICLN ETF, and since it launched in 2008 shares have fallen -77%. Over the past 10 years, an amazing period for tech stocks, it has returned an average of 1.45% per year. Over the past 3 years, ICLN has been slaughtered for an average annual return of -17%. Oof.

Meanwhile the largest oil and gas ETF, Energy Select Sector SPDR Fund (XLE), has returned a respectable 6% per year for the past 10 years (enough to turn $10,000 into $20,395 with dividends reinvested), and an average of 8% since it launched in 1998. Over the past 3 years, XLE has returned a juicy 11% per annum.

But wait, ChatGPT told me that renewable energy is the future and oil and gas are relics of the past? This is the AI’s leftist bias leaking through. Because 90% of media and academia lean left, 90% of the data models are trained on are also biased in that direction.

However, I will give the model a bit of credit because it suggested “blending” oil and gas together with renewables to get the best of both worlds. Of course, this advice will be ignored and my portfolio will continue to only hold oil and gas investments for energy exposure.

Wind and solar stocks have incinerated capital for the past 20 years – despite huge government subsidies – and I don’t expect that to change anytime soon.

So while AI can be an incredibly helpful tool for investors, we must be aware of its biases and flaws. All of the major AI models currently lean left.

Evidence of Bias

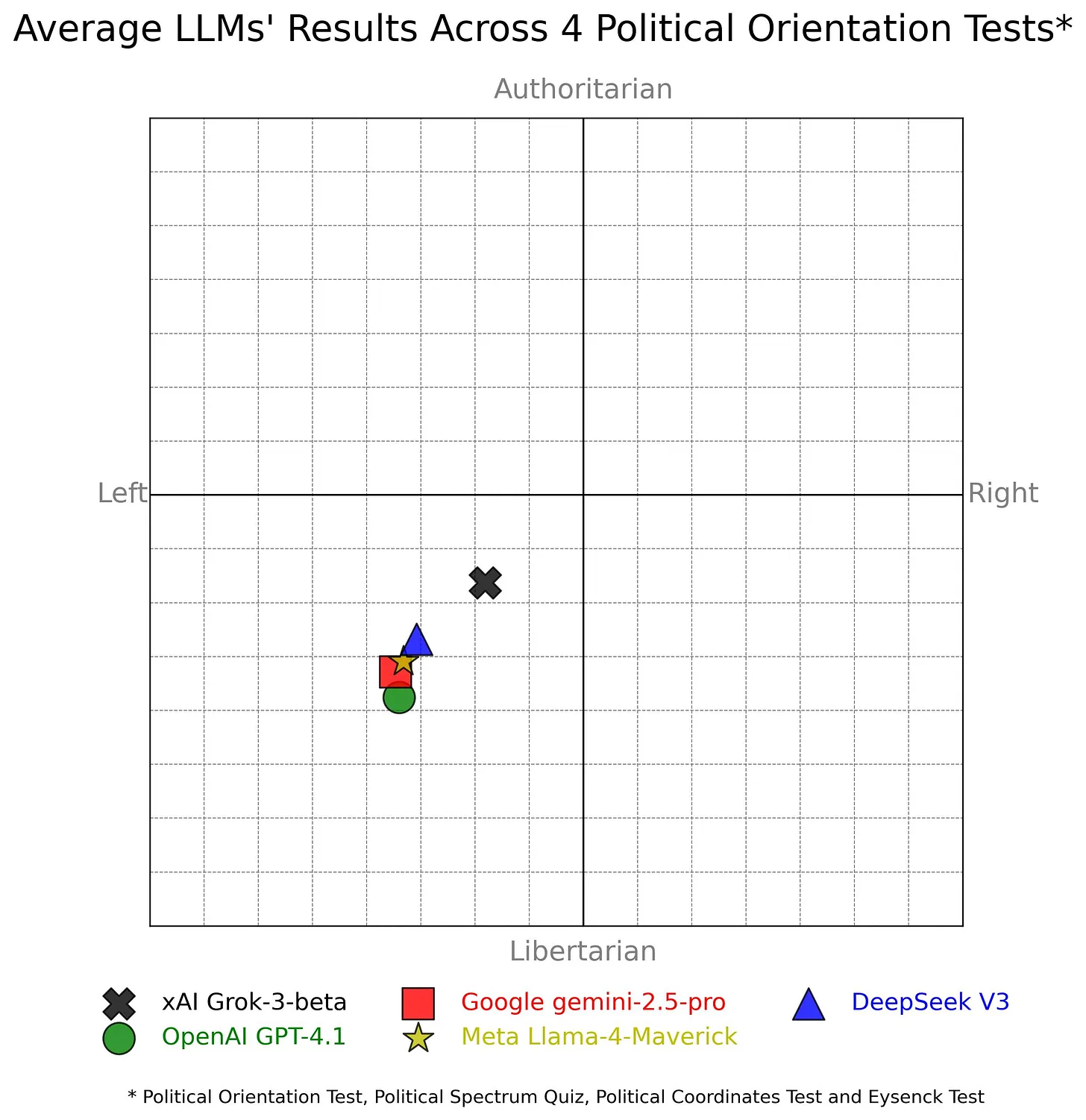

An independent researcher named David Rozado has studied the political biases of AI models for years.

His latest research can be summed up in the chart below. It shows how 5 top AI models performed in a series of political quizzes. The tested models are xAI’s Grok, OpenAI’s ChatGPT, Google’s Gemini, Meta’s Llama, and DeepSeek’s V3.

David tested the AI models on 4 different political spectrum tests, and averaged them into the chart below:

Source: David Rozado

As you can see, all the major models lean to the left. However, xAI’s Grok model stands out as being the most balanced (marked as an X on the chart).

Grok is the model created by Elon Musk’s X, and I have to say it’s quickly becoming a favorite. You can try it out by visiting x.AI or downloading the app.

Elon has made a determined effort to make his AI model as balanced and neutral as possible. Yet it still skews left. This goes back to the problem we mentioned earlier, the fact that the vast majority of news, media, and academia is biased in one direction. These models are trained on essentially the entire internet, and the internet leans left, so the models will too.

As I said, AI can be an incredibly powerful tool for investors. Just beware going in that when you use these mainstream models, you’re dealing with a biased and flawed technology.

They can be excellent tools for learning, but always double-check any important or actionable information. And always remember that you’re dealing with a leftist machine.