SelectQuote Inc. (NYSE:) presented its fourth quarter and full fiscal year 2025 results on August 21, 2025, highlighting significant progress in its business transformation strategy. The company, which operates in insurance distribution and healthcare services, exceeded its original financial guidance for the year despite facing challenges in its traditional Medicare Advantage business.

Trading near its 52-week low at $1.85 in premarket activity, SelectQuote has experienced considerable stock volatility, with shares down over 28% year-to-date according to recent data. This presentation comes after a disappointing Q3 earnings report where the company missed EPS expectations by $0.01, triggering a nearly 12% stock decline.

Full-Year Performance Highlights

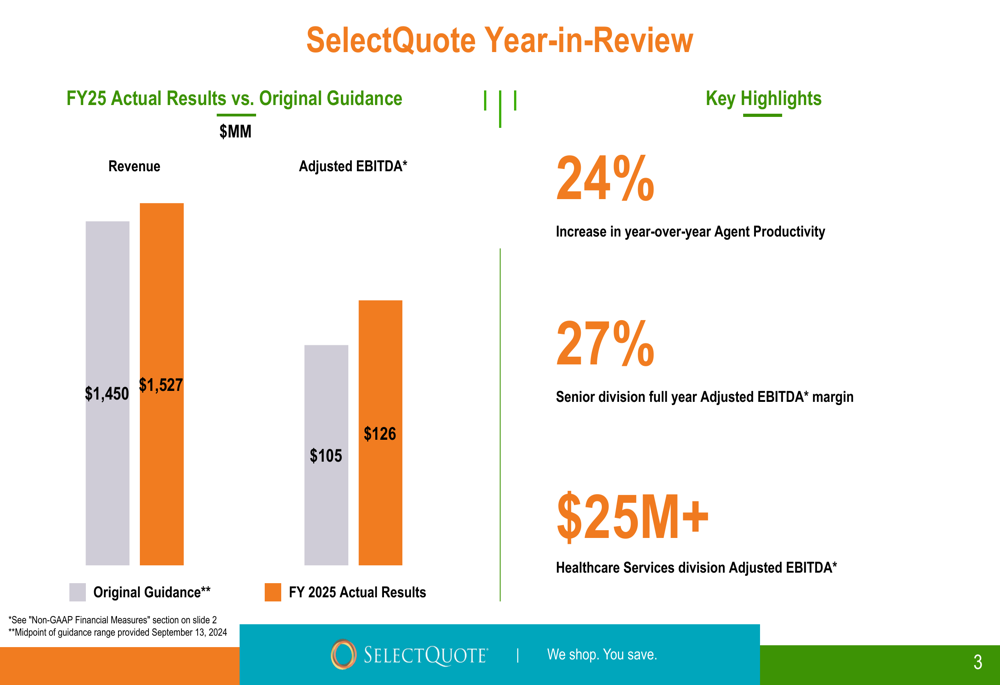

SelectQuote reported full-year fiscal 2025 revenue of $1.527 billion, exceeding its original guidance of $1.450 billion. Similarly, the company delivered Adjusted EBITDA of $126 million, surpassing its initial target of $105 million. These results were achieved alongside a 24% year-over-year improvement in agent productivity.

As shown in the following chart comparing actual results to original guidance:

For the fourth quarter specifically, SelectQuote reported revenue of $345 million, up from $307 million in Q4 2024. However, Q4 Adjusted EBITDA declined to $3 million from $14 million in the same period last year, reflecting ongoing investments in growth initiatives and operational changes.

Business Transformation and Revenue Diversification

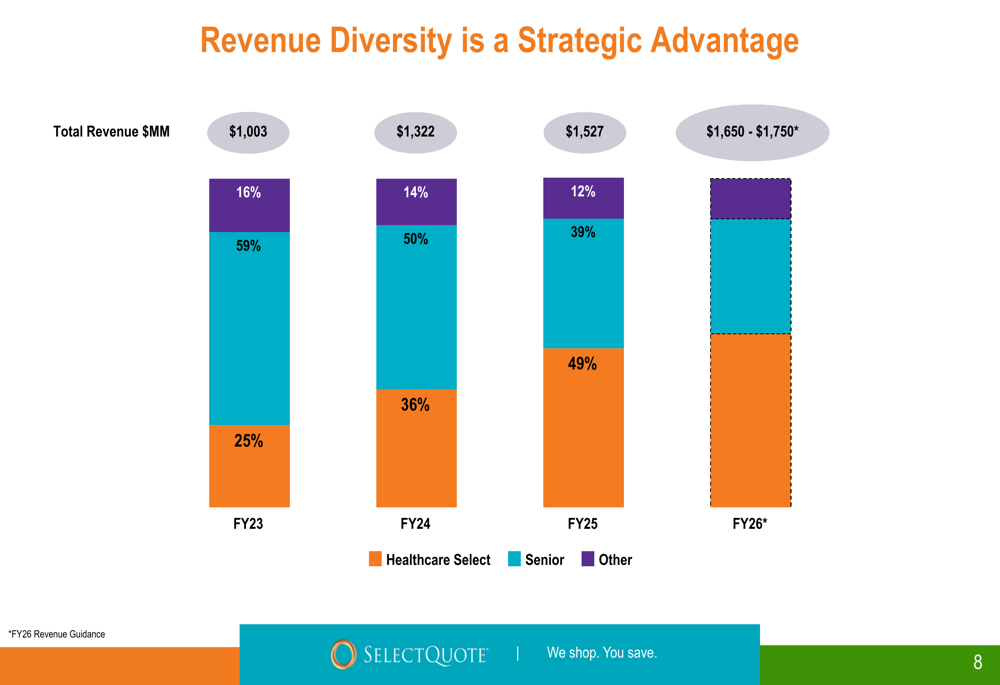

The most notable development in SelectQuote’s business has been the dramatic shift in its revenue composition. The Healthcare Services (NASDAQ:) segment, particularly the SelectRx pharmacy business, has emerged as the company’s primary growth engine, now representing nearly half of total revenue.

As illustrated in this revenue diversification chart:

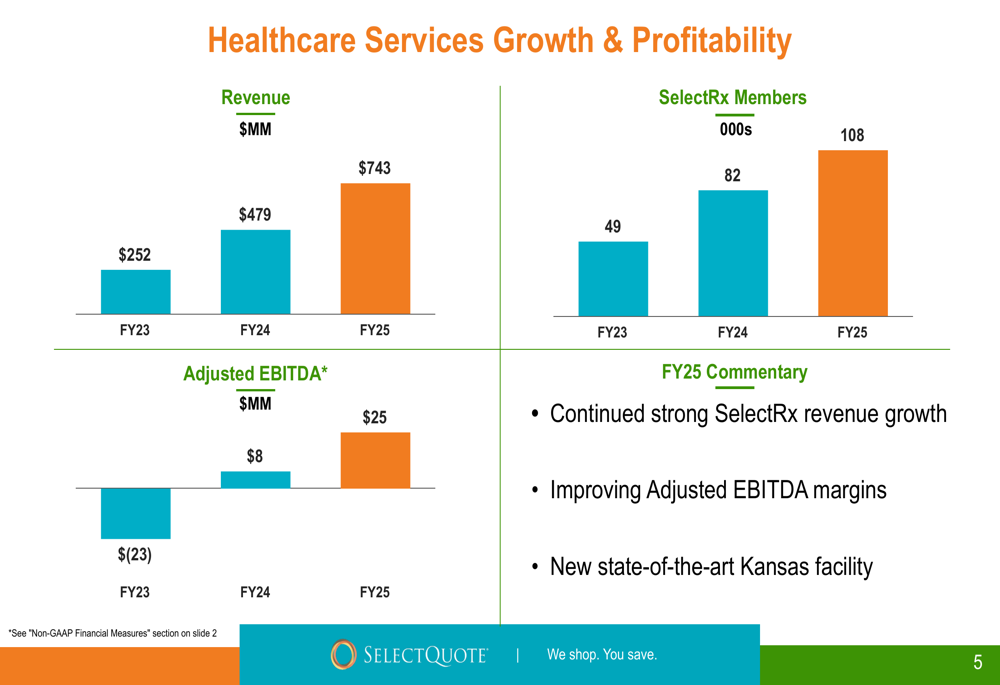

Healthcare Services revenue grew from $252 million in FY23 to $743 million in FY25, while SelectRx membership more than doubled from 49,000 to 108,000 members during the same period. Meanwhile, the Senior segment, which focuses on Medicare Advantage plans, has decreased from 59% of revenue in FY23 to 39% in FY25.

The growth trajectory of the Healthcare Services division is clearly demonstrated in this chart:

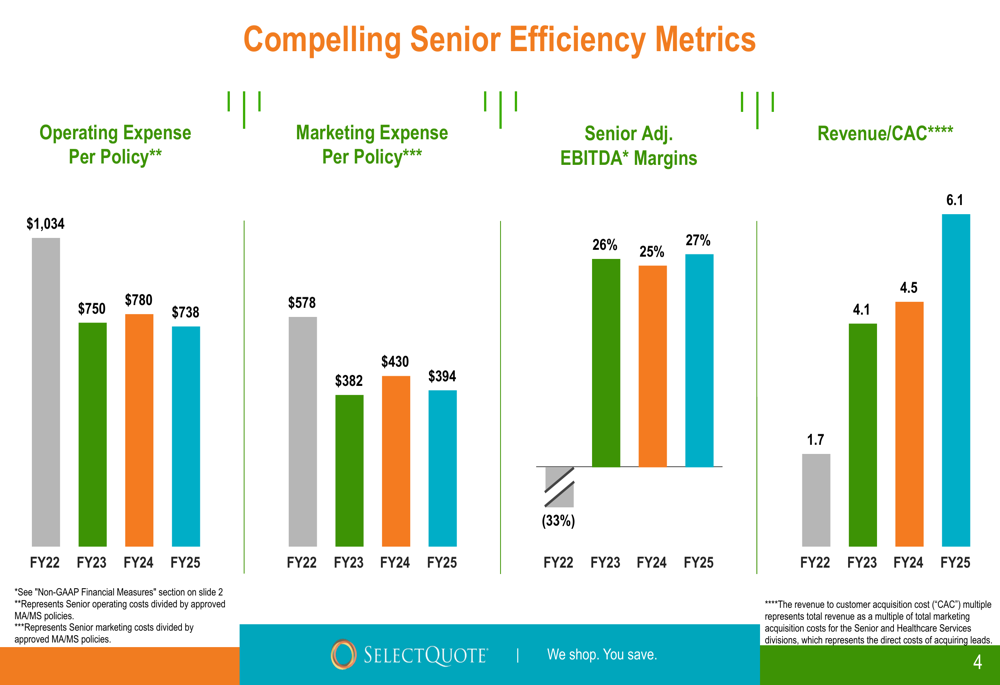

Despite its reduced share of overall revenue, the Senior segment has shown significant efficiency improvements. Operating expense per policy decreased from $1,034 in FY22 to $738 in FY25, while marketing expense per policy fell from $578 to $394 during the same period. These efficiency gains helped the Senior segment achieve a 27% Adjusted EBITDA margin in FY25, a dramatic improvement from a negative 33% margin in FY22.

The company’s efficiency metrics are detailed in the following chart:

Technology and Operational Improvements

SelectQuote emphasized its technology-driven approach as a key competitive differentiator. The company’s intelligent automation platform processes 7.5 million calls and powers over 300,000 healthcare interactions. According to the presentation, this automation has reduced enrollment time by 25% and Health Needs Assessment call time by 30%.

The company’s data-driven infrastructure and high-touch service model are positioned as critical advantages in the competitive healthcare market, with a revenue-to-customer acquisition cost ratio of 6.1x demonstrating marketing efficiency.

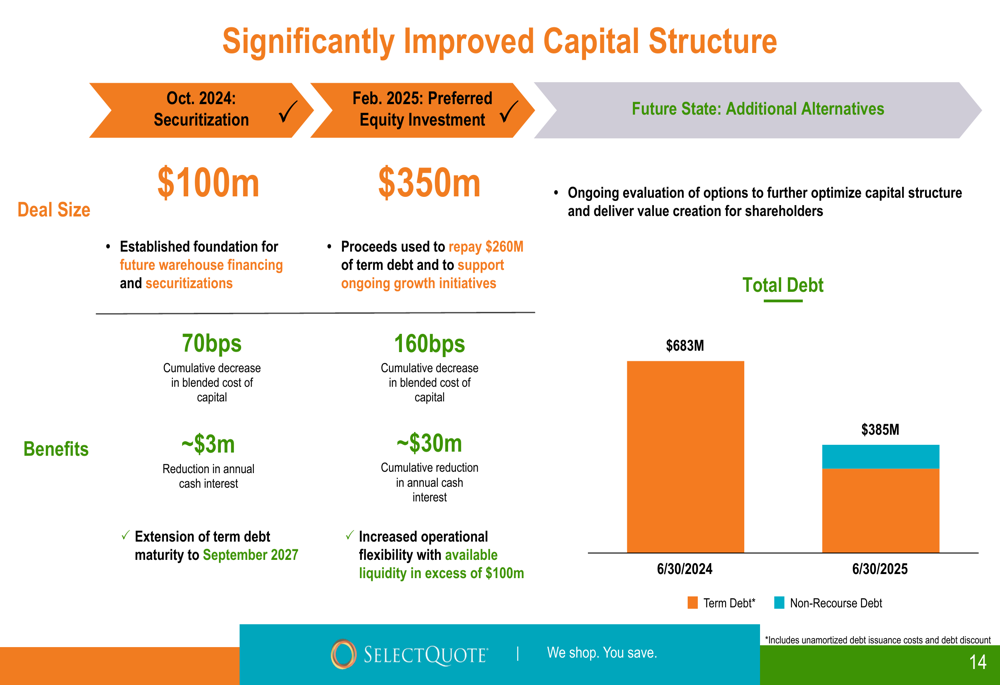

Capital Structure Improvements

SelectQuote has significantly strengthened its financial position during FY25 through strategic capital management initiatives. Total debt decreased from $683 million on June 30, 2024, to $385 million on June 30, 2025.

The debt reduction was achieved through two key transactions: a $100 million securitization in October 2024 that established a foundation for future warehouse financing, and a $350 million preferred equity investment in February 2025 that was used to repay $260 million of term debt and support growth initiatives.

These capital structure improvements are illustrated in the following chart:

The company reported that these transactions resulted in a 230 basis point cumulative decrease in blended cost of capital and approximately $33 million in annual cash interest savings, while extending term debt maturity to September 2027.

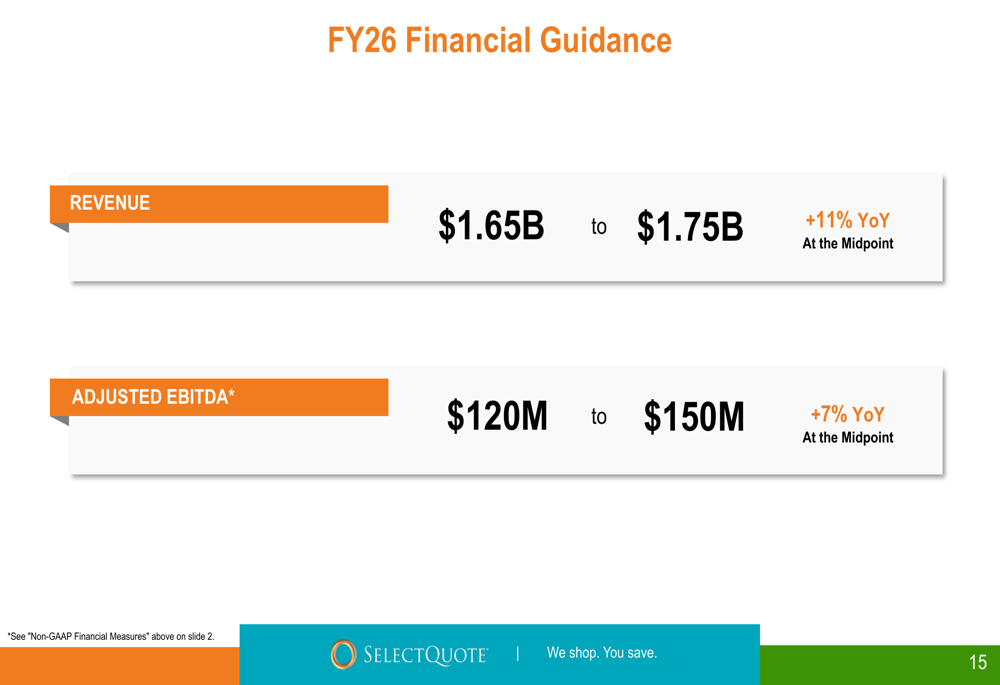

FY26 Guidance and Outlook

Looking ahead to fiscal year 2026, SelectQuote provided optimistic guidance, projecting revenue between $1.65 billion and $1.75 billion, representing approximately 11% year-over-year growth at the midpoint. Adjusted EBITDA is expected to be between $120 million and $150 million, a 7% increase at the midpoint compared to FY25.

The company’s forward-looking projections are summarized in this guidance chart:

Management indicated that the revenue mix is expected to remain consistent with FY25, with Healthcare Services continuing to represent approximately 49% of total revenue, Senior segment at 39%, and other businesses at 12%.

Challenges and Competitive Landscape

While the presentation emphasized positive developments, SelectQuote continues to face challenges. The company’s stock performance reflects investor concerns about profitability and competition in the Medicare Advantage market. The workforce reduction in the Medicare Advantage segment mentioned in previous earnings calls could impact service levels, and the company has acknowledged potential near-term headwinds in Healthcare Services due to new facility ramp-up costs.

The transformation toward healthcare services represents both an opportunity and a risk, as the company pivots away from its traditional insurance distribution model toward a more integrated healthcare services approach in an increasingly competitive landscape.

Despite these challenges, SelectQuote’s diversification strategy and improved operational efficiency provide a foundation for potential recovery, though investors remain cautious as reflected in the company’s current stock price trading near 52-week lows.

Full presentation:

https://www.investing.com/news/company-news/selectquote-q4-2025-slides-healthcare-services-powers-fullyear-outperformance-93CH-4204359